Anda mungkin juga menyukai

- Microeconomics: The Costs of ProductionDokumen8 halamanMicroeconomics: The Costs of ProductiondewiBelum ada peringkat

- Types of Market StructureDokumen16 halamanTypes of Market StructureCatarina CoelhoBelum ada peringkat

- Debunking Economics - SupplementDokumen46 halamanDebunking Economics - SupplementApostolos FsnsBelum ada peringkat

- Lecture 7 Competitive Market (Lec)Dokumen17 halamanLecture 7 Competitive Market (Lec)Fathimath ShaheeraBelum ada peringkat

- Pr. of Eco - Prod & CostDokumen38 halamanPr. of Eco - Prod & CostmukulBelum ada peringkat

- Introductory MicroeconomiDokumen7 halamanIntroductory Microeconomivivian umangBelum ada peringkat

- Business and The Cost of ProductionDokumen46 halamanBusiness and The Cost of ProductionBhoxs Joey CelesparaBelum ada peringkat

- LESSON 16 - Cost, Revenue and ProfitDokumen5 halamanLESSON 16 - Cost, Revenue and ProfitfarahBelum ada peringkat

- Perfect Competition Revision NotesDokumen10 halamanPerfect Competition Revision NotesJyot NarangBelum ada peringkat

- Unit 8 - Perfect CompetitionDokumen20 halamanUnit 8 - Perfect CompetitionRax-Nguajandja KapuireBelum ada peringkat

- Principles of Microeconomics - Costs of ProductionDokumen45 halamanPrinciples of Microeconomics - Costs of ProductionKatherine SauerBelum ada peringkat

- Game theory insights for oligopoliesDokumen3 halamanGame theory insights for oligopoliesAsfawosen DingamaBelum ada peringkat

- 03 NotesDokumen5 halaman03 NotesMahendra JarwalBelum ada peringkat

- Perfect Competition MarketDokumen17 halamanPerfect Competition MarketMaide HamasesBelum ada peringkat

- MONOPOLY Market Spring 2022Dokumen50 halamanMONOPOLY Market Spring 2022Abid SunnyBelum ada peringkat

- Perfect Competition: Ch. 20, Economics 9 Ed, R.A. ArnoldDokumen11 halamanPerfect Competition: Ch. 20, Economics 9 Ed, R.A. ArnoldMd Abil KhanBelum ada peringkat

- FinalDokumen20 halamanFinalMaryamBelum ada peringkat

- Practice: + 10Q and FC ($) 200, Where Q Is inDokumen2 halamanPractice: + 10Q and FC ($) 200, Where Q Is insơn trầnBelum ada peringkat

- Chapter 5 - Production and CostDokumen29 halamanChapter 5 - Production and CostYusuf OmarBelum ada peringkat

- ch#8 & 9Dokumen12 halamanch#8 & 9Rao Talha Rao NasirBelum ada peringkat

- Chapter 13 - The Costs of Production: Profit MaximizationDokumen28 halamanChapter 13 - The Costs of Production: Profit MaximizationTường HuyBelum ada peringkat

- Model Answer of Assignment 2 DR ShantalDokumen5 halamanModel Answer of Assignment 2 DR ShantalBishoy EmileBelum ada peringkat

- Market PerfectDokumen35 halamanMarket PerfectLoretta D'SouzaBelum ada peringkat

- Ent300 - Calculation MSDokumen1 halamanEnt300 - Calculation MSWAN NUR AYUNI ISNINBelum ada peringkat

- Chapter 05 Inputs & CostsDokumen67 halamanChapter 05 Inputs & CostsMark EbrahimBelum ada peringkat

- Ps5 Solution AdjDokumen5 halamanPs5 Solution AdjJonathanFengBelum ada peringkat

- Econ 2010 Final Essay QuestionsDokumen6 halamanEcon 2010 Final Essay QuestionsBrandon Lehr0% (1)

- DocumentDokumen5 halamanDocumentworkinehamanuBelum ada peringkat

- S2 CMA c02 Cost-Volume-Profit AnalysisDokumen25 halamanS2 CMA c02 Cost-Volume-Profit Analysisdiasjoy67Belum ada peringkat

- Market_power__1_ (1)Dokumen19 halamanMarket_power__1_ (1)taraffoiBelum ada peringkat

- Assignment 2 DR ShantalDokumen4 halamanAssignment 2 DR ShantalBishoy EmileBelum ada peringkat

- 3 - BREAK EVEN ANALYSIS - UploadDokumen5 halaman3 - BREAK EVEN ANALYSIS - Uploadniaz kilamBelum ada peringkat

- CHAPTER 9: Firm Behavior and Costs of ProductionDokumen9 halamanCHAPTER 9: Firm Behavior and Costs of ProductionMuhamamd Asfand YarBelum ada peringkat

- Break-Even Analysis 8.1 & 8.2Dokumen21 halamanBreak-Even Analysis 8.1 & 8.2Jelian E. TangaroBelum ada peringkat

- Cost-Volume Profit Analysis Break-Even PointDokumen18 halamanCost-Volume Profit Analysis Break-Even PointkishorechakravarthyBelum ada peringkat

- Merrion ProductsDokumen11 halamanMerrion ProductsVivek NarayananBelum ada peringkat

- Costing and PricingDokumen20 halamanCosting and PricingRahim JAbbarBelum ada peringkat

- Maximizing Profits in Different Market StructuresDokumen28 halamanMaximizing Profits in Different Market StructuresAngela WaganBelum ada peringkat

- Managerial Economics Assignment Biruk TesfaDokumen13 halamanManagerial Economics Assignment Biruk TesfaBirukee ManBelum ada peringkat

- 2 National Accounting - Lecture 2.Ppt (Autosaved)Dokumen32 halaman2 National Accounting - Lecture 2.Ppt (Autosaved)Darren MgayaBelum ada peringkat

- Cost Concepts: Gross Margin and Contribution MarginDokumen9 halamanCost Concepts: Gross Margin and Contribution MarginMahediBelum ada peringkat

- VMCSCHDokumen8 halamanVMCSCH2402nguyenlinhBelum ada peringkat

- Economics Final ExamDokumen17 halamanEconomics Final ExamAngelica Joy ManaoisBelum ada peringkat

- Production Analysis Group 6Dokumen36 halamanProduction Analysis Group 6Swapnil LilkeBelum ada peringkat

- CVP AnalysisDokumen18 halamanCVP AnalysisChristian TanBelum ada peringkat

- Competitive Firms and MarketsDokumen21 halamanCompetitive Firms and MarketsSarthakBelum ada peringkat

- Economics ExamDokumen15 halamanEconomics ExamИСЛАМБЕК СЕРІКҰЛЫBelum ada peringkat

- Unit7 D (A2)Dokumen10 halamanUnit7 D (A2)punte77Belum ada peringkat

- Cost Volume & ProfitDokumen40 halamanCost Volume & ProfitNitin Sharma100% (2)

- Niea NotesDokumen5 halamanNiea Notesogonnaakuneme830Belum ada peringkat

- Class Note - Chpt12 Decision MakingDokumen19 halamanClass Note - Chpt12 Decision MakingNicole LinBelum ada peringkat

- CVP analysis for cost-volume-profit relationshipsDokumen20 halamanCVP analysis for cost-volume-profit relationshipsDen Potxsz100% (1)

- Marginal CostingDokumen2 halamanMarginal Costingrupeshdahake8586Belum ada peringkat

- Cost-Volume-Profit AnalysisDokumen5 halamanCost-Volume-Profit AnalysisRaiza BarbasBelum ada peringkat

- Pasar Persaingan SempurnaDokumen38 halamanPasar Persaingan SempurnaCandri Rahma MaharaniBelum ada peringkat

- Assignment No 2Dokumen8 halamanAssignment No 2Fizza ImranBelum ada peringkat

- Bed 1101 Cat 1 MicroeconomicsDokumen10 halamanBed 1101 Cat 1 MicroeconomicsMuya KihumbaBelum ada peringkat

- Basic Microeconomics Handouts Week 1Dokumen13 halamanBasic Microeconomics Handouts Week 1ELMSSBelum ada peringkat

- Production TheoryDokumen72 halamanProduction TheoryAnirudh Dutta100% (1)

- Industrial Organization & Perfect CompetitionDokumen71 halamanIndustrial Organization & Perfect CompetitionRoni SuhandaniBelum ada peringkat

- Lecture 1 Ec3322 Sem I 2008 2009Dokumen46 halamanLecture 1 Ec3322 Sem I 2008 2009Roni SuhandaniBelum ada peringkat

- Outline: Industrial Organization: From The Fundamentals of Microeconomic PrinciplesDokumen12 halamanOutline: Industrial Organization: From The Fundamentals of Microeconomic PrinciplesRoni SuhandaniBelum ada peringkat

- Outline: Industrial Organization: From The Fundamentals of Microeconomic PrinciplesDokumen12 halamanOutline: Industrial Organization: From The Fundamentals of Microeconomic PrinciplesRoni SuhandaniBelum ada peringkat

- Lambang PMRDokumen3 halamanLambang PMRRoni SuhandaniBelum ada peringkat

- Textile Business PlanDokumen3 halamanTextile Business PlanJoshua Anim100% (2)

- 1708587720_FMCG-December-2023Dokumen32 halaman1708587720_FMCG-December-2023pimewip969Belum ada peringkat

- Porter Five Forces Analysis - Wikipedia, The Free EncyclopediaDokumen6 halamanPorter Five Forces Analysis - Wikipedia, The Free Encyclopediagkj2004Belum ada peringkat

- Comparative Study of SBI and Bank of BarodaDokumen39 halamanComparative Study of SBI and Bank of BarodaDaman Deep Singh ArnejaBelum ada peringkat

- Intermediate+Financial+Accounting+I+-+Chapter+3+ SDokumen26 halamanIntermediate+Financial+Accounting+I+-+Chapter+3+ SNeil StechschulteBelum ada peringkat

- Performance Evaluation of Equity and Mutual FundsDokumen33 halamanPerformance Evaluation of Equity and Mutual FundsDev ChoudharyBelum ada peringkat

- "Big Ben" Strategy by Kristian KerrDokumen4 halaman"Big Ben" Strategy by Kristian Kerrapi-26247058100% (1)

- Perfect Competition Describes Markets Such That No Participants Are Large Enough To HauctDokumen17 halamanPerfect Competition Describes Markets Such That No Participants Are Large Enough To HauctRrisingg MishraaBelum ada peringkat

- COBIT 4 To 5 MappingDokumen20 halamanCOBIT 4 To 5 MappingHASANULBelum ada peringkat

- BBA 6th Sem Syllabus IPUDokumen6 halamanBBA 6th Sem Syllabus IPUmayank0143Belum ada peringkat

- Calamos Market Neutral Income Fund: CmnixDokumen2 halamanCalamos Market Neutral Income Fund: CmnixAl BruceBelum ada peringkat

- RWE Annual Report 2011Dokumen240 halamanRWE Annual Report 2011eboskovskiBelum ada peringkat

- Entry Barrierin The Music IndustryDokumen8 halamanEntry Barrierin The Music IndustryuniquedeepakBelum ada peringkat

- SheDokumen2 halamanSheRhozeiah LeiahBelum ada peringkat

- LBC Express Holdings' Financial AnalysisDokumen9 halamanLBC Express Holdings' Financial AnalysisJerry ManatadBelum ada peringkat

- Bond PricingDokumen70 halamanBond PricingSharika EpBelum ada peringkat

- Q .6 Security Market LineDokumen3 halamanQ .6 Security Market LineMAHENDRA SHIVAJI DHENAK100% (1)

- Assets FormDokumen4 halamanAssets FormAnonymous k5CcMyU6100% (1)

- NCMR Brochure Intl Edition - Pdf.coredownloadDokumen47 halamanNCMR Brochure Intl Edition - Pdf.coredownload王晓斌Belum ada peringkat

- Herbalife Company Analysis-1Dokumen19 halamanHerbalife Company Analysis-1Maureen AtienoBelum ada peringkat

- Unit - I: Introduction To AccountingDokumen24 halamanUnit - I: Introduction To AccountingbuviaroBelum ada peringkat

- Chapte R: Dividend TheoryDokumen19 halamanChapte R: Dividend TheoryArunim MehrotraBelum ada peringkat

- 24941-Article Text-29253-1-10-20180730Dokumen11 halaman24941-Article Text-29253-1-10-20180730Dhea Ratih KusumaningtyasBelum ada peringkat

- Simple and Compound InterestDokumen26 halamanSimple and Compound InterestCarlos Cary Colon100% (7)

- Fauji Fertilizer Bin Qasim Ltd. - Valuation Report: Industry OverviewDokumen7 halamanFauji Fertilizer Bin Qasim Ltd. - Valuation Report: Industry OverviewValeed ChBelum ada peringkat

- MGT 215 Fundamentals of Financial ManagementDokumen4 halamanMGT 215 Fundamentals of Financial ManagementRajkishor PanditBelum ada peringkat

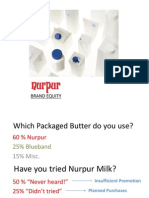

- Nurpur Brand EquityDokumen19 halamanNurpur Brand EquityBilal100% (2)

- Taxation and DepreciationDokumen62 halamanTaxation and Depreciationrobel popBelum ada peringkat

- Accounting ManualDokumen86 halamanAccounting ManualSaeed Rasool100% (1)

- Wm. Wrigley Jr. Co. Capital Structure AnalysisDokumen12 halamanWm. Wrigley Jr. Co. Capital Structure Analysis陳曄萱Belum ada peringkat