Anda mungkin juga menyukai

- Elegant Education Pack For Students by SlidesgoDokumen9 halamanElegant Education Pack For Students by SlidesgoAngie GarciaBelum ada peringkat

- BankingDokumen32 halamanBankingapi-173610472Belum ada peringkat

- Opening and Types of Bank Account: by Rushil Pandey 11hDokumen11 halamanOpening and Types of Bank Account: by Rushil Pandey 11hRushil PandeyBelum ada peringkat

- General InfoDokumen15 halamanGeneral Infodhuni143Belum ada peringkat

- 2011 BankingBasic Class enDokumen55 halaman2011 BankingBasic Class enJeevan DeeshaBelum ada peringkat

- Banking: What You Should Know About..Dokumen16 halamanBanking: What You Should Know About..Muhammad Fahad AkhterBelum ada peringkat

- Chapter 4: Money and Banking: Why Use A Bank?Dokumen23 halamanChapter 4: Money and Banking: Why Use A Bank?Jojilyn DabloBelum ada peringkat

- FM 202 Finals3Dokumen34 halamanFM 202 Finals3sudariodaisyre19Belum ada peringkat

- Consumer CreditDokumen45 halamanConsumer CreditJan Francine AbanteBelum ada peringkat

- Banking: Eastbourne Citizens Advice Bureau Financial LiteracyDokumen42 halamanBanking: Eastbourne Citizens Advice Bureau Financial LiteracyGIRIDHARI RANBIDABelum ada peringkat

- Kokan BankDokumen20 halamanKokan BankramshaBelum ada peringkat

- Professional EnglishDokumen10 halamanProfessional EnglishFrancesca Rutti AlvaradoBelum ada peringkat

- Deposist AccountDokumen6 halamanDeposist AccountwaheedarifBelum ada peringkat

- KasusDokumen2 halamanKasusJoe Erian Dinda PratiwiBelum ada peringkat

- 04 Social Security Get Your Payments Electronically En-05-10073Dokumen8 halaman04 Social Security Get Your Payments Electronically En-05-10073api-309082881Belum ada peringkat

- Unit 4 Credit - For WEBSITEDokumen46 halamanUnit 4 Credit - For WEBSITEASHISH KUMARBelum ada peringkat

- Saving AccountDokumen9 halamanSaving AccountpalkhinBelum ada peringkat

- Guide To Payment Types, With Pros and Cons For EachDokumen14 halamanGuide To Payment Types, With Pros and Cons For EachJeffreyBelum ada peringkat

- 2010 BB Brochure EngDokumen2 halaman2010 BB Brochure EngjoswaroopBelum ada peringkat

- Jargon Buster Fact SheetDokumen9 halamanJargon Buster Fact Sheettedi wediBelum ada peringkat

- Get Your Payments Electronically: Socialsecurity - GovDokumen8 halamanGet Your Payments Electronically: Socialsecurity - GovJacqueline VillaltaBelum ada peringkat

- Bank ProductsDokumen14 halamanBank ProductsJuhi AgrawalBelum ada peringkat

- Bank AccountsDokumen47 halamanBank AccountsGSOCION LOUSELLE LALAINE D.Belum ada peringkat

- Banking: Eastbourne Citizens Advice Bureau Financial LiteracyDokumen39 halamanBanking: Eastbourne Citizens Advice Bureau Financial LiteracyPriya JainBelum ada peringkat

- Document 6Dokumen6 halamanDocument 6Yasiru PandigamaBelum ada peringkat

- A, B, C - Specialised Accounting - 1Dokumen12 halamanA, B, C - Specialised Accounting - 1محمود احمدBelum ada peringkat

- Banking Solutions For Ageing PopulationDokumen2 halamanBanking Solutions For Ageing PopulationpallavimahagavkarBelum ada peringkat

- The Essentials. Our Guide To CreditDokumen16 halamanThe Essentials. Our Guide To CreditHands OffBelum ada peringkat

- Opening A Bank Account Can Seem IntimidatingDokumen9 halamanOpening A Bank Account Can Seem IntimidatingtriratnacomBelum ada peringkat

- What Is A BankDokumen5 halamanWhat Is A BankmanojdunnhumbyBelum ada peringkat

- File 1641790871 0004738 BLPDokumen118 halamanFile 1641790871 0004738 BLPwww.ishusingh4420Belum ada peringkat

- Types of Electronic Banking: Debit CardsDokumen2 halamanTypes of Electronic Banking: Debit CardsSk nabilaBelum ada peringkat

- Credit Management CounselingDokumen47 halamanCredit Management CounselingKaren LaccayBelum ada peringkat

- Unit 5Dokumen16 halamanUnit 5rishavBelum ada peringkat

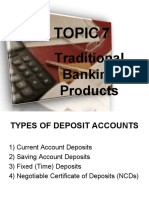

- Topic 7: Traditional Banking ProductsDokumen26 halamanTopic 7: Traditional Banking ProductsPremah BalasundramBelum ada peringkat

- DOMINGO, Celine Elaiza B. Bas Fin - Sec 2 Types of Deposits in The BankDokumen2 halamanDOMINGO, Celine Elaiza B. Bas Fin - Sec 2 Types of Deposits in The BankCeline DomingoBelum ada peringkat

- Payment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsDari EverandPayment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsBelum ada peringkat

- CitibankDokumen9 halamanCitibankSiva BalajiBelum ada peringkat

- An Introduction To Banking - PowerPointDokumen25 halamanAn Introduction To Banking - PowerPointRuchira PereraBelum ada peringkat

- Personal Finance - Chapter 6Dokumen10 halamanPersonal Finance - Chapter 6a.wilson7980Belum ada peringkat

- English For Banking and FinanceDokumen28 halamanEnglish For Banking and FinancefathiyarizkiBelum ada peringkat

- Understanding CCDokumen5 halamanUnderstanding CCJoseph IsekBelum ada peringkat

- Basic Documents and Transactions Related To Bank DepositsDokumen18 halamanBasic Documents and Transactions Related To Bank DepositsSophia NicoleBelum ada peringkat

- Credit MGMTDokumen7 halamanCredit MGMTaden Budi wBelum ada peringkat

- Credit Report and BorrowingDokumen32 halamanCredit Report and Borrowingparkerroach21Belum ada peringkat

- Credit CardDokumen51 halamanCredit CardSmita JainBelum ada peringkat

- Accounting Prefinals ReviewerDokumen9 halamanAccounting Prefinals ReviewerMaxine RodriguezBelum ada peringkat

- Fabm2 Q1 - W7 M10Dokumen17 halamanFabm2 Q1 - W7 M10Ashianna Kim FernandezBelum ada peringkat

- Level Up Lesson Plans Banking 101 DDokumen15 halamanLevel Up Lesson Plans Banking 101 DPriyanka artsBelum ada peringkat

- Assignment On Payment Methods: Submitted byDokumen6 halamanAssignment On Payment Methods: Submitted bySanam ChouhanBelum ada peringkat

- 5 6226516373657356654Dokumen230 halaman5 6226516373657356654Sangeeta HatwalBelum ada peringkat

- Accounts and Financial Services 2Dokumen25 halamanAccounts and Financial Services 2Sweetie PíeBelum ada peringkat

- Moneymaxims 28pDokumen28 halamanMoneymaxims 28pparaggnBelum ada peringkat

- How Do We Pay For ThingsDokumen17 halamanHow Do We Pay For ThingsRidhima MathurBelum ada peringkat

- Banking Organizer & Note TakingDokumen8 halamanBanking Organizer & Note TakingRashid DannettBelum ada peringkat

- Chase Bank Account Rules and Regulations 12-31-08Dokumen34 halamanChase Bank Account Rules and Regulations 12-31-08wps013100% (1)

- Credit Score Lecture NotesDokumen5 halamanCredit Score Lecture NotesGeri Leine0% (1)

- ANZ Cashback Visa GuideDokumen16 halamanANZ Cashback Visa GuideDewaldBelum ada peringkat

- Collections and Repayments PDFDokumen54 halamanCollections and Repayments PDFJimuel FaigaoBelum ada peringkat

- World Issues Yearlong Project 2018Dokumen13 halamanWorld Issues Yearlong Project 2018api-238711136Belum ada peringkat

- Subsaharaafricapowerpoint MinDokumen72 halamanSubsaharaafricapowerpoint Minapi-238711136Belum ada peringkat

- Subsaharaafricapowerpoint MinDokumen72 halamanSubsaharaafricapowerpoint Minapi-238711136Belum ada peringkat

- Latinamericai MinDokumen31 halamanLatinamericai Minapi-238711136Belum ada peringkat

- LatinamericaDokumen56 halamanLatinamericaapi-2387111360% (1)

- GlobalstudiessyllabusDokumen3 halamanGlobalstudiessyllabusapi-238711136Belum ada peringkat

- Honors Global Studies: Liberty High School Course Syllabus: 2016 - 2017 Mr. Christian ConradDokumen3 halamanHonors Global Studies: Liberty High School Course Syllabus: 2016 - 2017 Mr. Christian Conradapi-238711136Belum ada peringkat

- Asia Thepacificpowerpoint-MinDokumen61 halamanAsia Thepacificpowerpoint-Minapi-238711136Belum ada peringkat

- Population Culture Powerpoint-MinDokumen64 halamanPopulation Culture Powerpoint-Minapi-238711136Belum ada peringkat

- Population Culture Powerpoint-MinDokumen64 halamanPopulation Culture Powerpoint-Minapi-238711136Belum ada peringkat

- Asia Thepacificpowerpoint-MinDokumen61 halamanAsia Thepacificpowerpoint-Minapi-238711136Belum ada peringkat

- OceaniaDokumen20 halamanOceaniaapi-238711136Belum ada peringkat

- Political Economic World Powerpoint-MinDokumen67 halamanPolitical Economic World Powerpoint-Minapi-2387111360% (1)

- OceaniaDokumen20 halamanOceaniaapi-238711136Belum ada peringkat

- AfricatestDokumen4 halamanAfricatestapi-238711136Belum ada peringkat

- InvestingDokumen74 halamanInvestingapi-238711136Belum ada peringkat

- Political EconomicworldtestDokumen5 halamanPolitical Economicworldtestapi-238711136Belum ada peringkat

- Semi RGDokumen5 halamanSemi RGapi-238711136Belum ada peringkat

- Europe RussiatestDokumen5 halamanEurope Russiatestapi-238711136100% (1)

- Northamerica OceaniatestDokumen3 halamanNorthamerica Oceaniatestapi-238711136Belum ada peringkat

- M e TestDokumen5 halamanM e Testapi-238711136Belum ada peringkat

- Chris Conrad - Planboard Week - Aug 16 2015Dokumen1 halamanChris Conrad - Planboard Week - Aug 16 2015api-238711136Belum ada peringkat

- Chris Conrad - Planboard Week - Aug 30 2015Dokumen2 halamanChris Conrad - Planboard Week - Aug 30 2015api-238711136Belum ada peringkat

- Chris Conrad - Planboard Week - Sep 6 2015 1Dokumen2 halamanChris Conrad - Planboard Week - Sep 6 2015 1api-238711136Belum ada peringkat

- Chris Conrad - Planboard Week - Aug 23 2015Dokumen2 halamanChris Conrad - Planboard Week - Aug 23 2015api-238711136Belum ada peringkat

- Economics & Personal Finance: Course DescriptionDokumen4 halamanEconomics & Personal Finance: Course Descriptionapi-238711136Belum ada peringkat

- Economicsunit 1Dokumen39 halamanEconomicsunit 1api-238711136Belum ada peringkat

- Oceangoing Ships 2007 PDFDokumen102 halamanOceangoing Ships 2007 PDFaleventBelum ada peringkat

- Entry Mode StrategyDokumen12 halamanEntry Mode StrategyMetiya RatimartBelum ada peringkat

- EcoTourism Unit 8Dokumen20 halamanEcoTourism Unit 8Mark Angelo PanisBelum ada peringkat

- CET Analysis of SamsungDokumen9 halamanCET Analysis of SamsungMj PayalBelum ada peringkat

- TCSDokumen4 halamanTCSjayasree_reddyBelum ada peringkat

- Yong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDDokumen9 halamanYong Le: Beijing Huaxia Yongleadhesive Tape Co., LTDColors Little ParkBelum ada peringkat

- Unit 7: Account Current: Learning OutcomesDokumen14 halamanUnit 7: Account Current: Learning OutcomesamirBelum ada peringkat

- B5M ElDokumen3 halamanB5M ElBALAKRISHNANBelum ada peringkat

- Eco-Fashion, Sustainability, and Social Responsibility: Survey ReportDokumen16 halamanEco-Fashion, Sustainability, and Social Responsibility: Survey ReportNovemberlady09Belum ada peringkat

- List of Turkish CompaniesDokumen5 halamanList of Turkish CompaniesMary GarciaBelum ada peringkat

- Steeple AnalysisDokumen2 halamanSteeple AnalysisSamrahBelum ada peringkat

- Effects of Labor Standard Law in Regularization of EmployeesDokumen4 halamanEffects of Labor Standard Law in Regularization of EmployeesNicole Ann MagistradoBelum ada peringkat

- List of TSD Facilities July 31 2019Dokumen15 halamanList of TSD Facilities July 31 2019Emrick SantiagoBelum ada peringkat

- Actions Required For Building A Strong Startup Ecosystem in ManipurDokumen3 halamanActions Required For Building A Strong Startup Ecosystem in ManipuryibungoBelum ada peringkat

- Herbert HooverDokumen4 halamanHerbert HooverZuñiga Salazar Hamlet EnocBelum ada peringkat

- Data Mahal (List Sponsorship 2019)Dokumen11 halamanData Mahal (List Sponsorship 2019)namira lutfiaBelum ada peringkat

- WEG India Staff Contact Numbers PDFDokumen10 halamanWEG India Staff Contact Numbers PDFM.DINESH KUMARBelum ada peringkat

- Grade 11 Daily Lesson Log: ObjectivesDokumen2 halamanGrade 11 Daily Lesson Log: ObjectivesKarla BangFerBelum ada peringkat

- Joint Stock CompanyDokumen2 halamanJoint Stock CompanybijuBelum ada peringkat

- Indian Real Estate SectorDokumen8 halamanIndian Real Estate SectorSumit VrmaBelum ada peringkat

- I. Convertible Currencies With Bangko Sentral:: Run Date/timeDokumen1 halamanI. Convertible Currencies With Bangko Sentral:: Run Date/timeLucito FalloriaBelum ada peringkat

- Chapter 6 MoodleDokumen36 halamanChapter 6 MoodleMichael TheodricBelum ada peringkat

- Employee Stock Ownership PlansDokumen3 halamanEmployee Stock Ownership PlansmanoramanBelum ada peringkat

- Bata FactsDokumen3 halamanBata FactsPrashant SantBelum ada peringkat

- AMT4SAP - Junio26 - Red - v3 PDFDokumen30 halamanAMT4SAP - Junio26 - Red - v3 PDFCarlos Eugenio Lovera VelasquezBelum ada peringkat

- Assessment of The Kosovo Innovation SystemDokumen113 halamanAssessment of The Kosovo Innovation SystemOECD Global RelationsBelum ada peringkat

- ASEAN Association of Southeast Asian NationsDokumen3 halamanASEAN Association of Southeast Asian NationsnicolepekkBelum ada peringkat

- The Seven Elements of CultureDokumen2 halamanThe Seven Elements of CultureДарья СухоборченкоBelum ada peringkat

- Tax Reviewer For MidtermDokumen4 halamanTax Reviewer For Midtermjury jasonBelum ada peringkat

- Pune MetroDokumen11 halamanPune MetroGanesh NichalBelum ada peringkat