Anda mungkin juga menyukai

- ItfDokumen3 halamanItfDeepak Shori100% (1)

- PDF 1Dokumen45 halamanPDF 1Deepak ShoriBelum ada peringkat

- Safety Data Sheet: Product Name: MOBILGARD 540Dokumen11 halamanSafety Data Sheet: Product Name: MOBILGARD 540Deepak ShoriBelum ada peringkat

- Alfalaval UVvsECDokumen13 halamanAlfalaval UVvsECDeepak ShoriBelum ada peringkat

- IMO News - Autumn Issue - 2017Dokumen36 halamanIMO News - Autumn Issue - 2017Deepak ShoriBelum ada peringkat

- EthicsDokumen8 halamanEthicsDeepak ShoriBelum ada peringkat

- FocDokumen7 halamanFocDeepak ShoriBelum ada peringkat

- Autocar Spare Parts Price SurveyDokumen10 halamanAutocar Spare Parts Price SurveyDeepak ShoriBelum ada peringkat

- SofDokumen2 halamanSofDeepak ShoriBelum ada peringkat

- Law of TortsDokumen41 halamanLaw of TortsDeepak ShoriBelum ada peringkat

- ItfDokumen3 halamanItfDeepak Shori100% (1)

- Ethics in ShipbrokingDokumen4 halamanEthics in ShipbrokingDeepak ShoriBelum ada peringkat

- IccDokumen3 halamanIccDeepak ShoriBelum ada peringkat

- Ship-owners' decisions to outsource vessel managementDokumen24 halamanShip-owners' decisions to outsource vessel managementDeepak ShoriBelum ada peringkat

- Riska of LOCDokumen11 halamanRiska of LOCDeepak ShoriBelum ada peringkat

- IntroductionDokumen2 halamanIntroductionDeepak ShoriBelum ada peringkat

- Public and Private CompanyDokumen22 halamanPublic and Private CompanyDeepak ShoriBelum ada peringkat

- Ics Exams 2013 Questions SLDokumen1 halamanIcs Exams 2013 Questions SLDeepak ShoriBelum ada peringkat

- Special Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDokumen3 halamanSpecial Circular: Revised Himalaya Clause For Bills of Lading and Other ContractsDeepak ShoriBelum ada peringkat

- UC40+ User GuideDokumen2 halamanUC40+ User GuideDeepak ShoriBelum ada peringkat

- Updated Glossary in Co TermsDokumen13 halamanUpdated Glossary in Co TermsDeepak ShoriBelum ada peringkat

- Public and Private CompanyDokumen22 halamanPublic and Private CompanyDeepak ShoriBelum ada peringkat

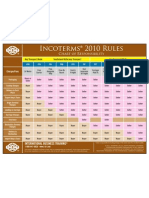

- Incoterms 2010 at A GlanceDokumen1 halamanIncoterms 2010 at A GlanceAftab UddinBelum ada peringkat

- Adler V Dickson The HimalayaDokumen18 halamanAdler V Dickson The HimalayaDeepak ShoriBelum ada peringkat

- Ics Exams 2013 Questions SBDokumen1 halamanIcs Exams 2013 Questions SBDeepak ShoriBelum ada peringkat

- 01 IntroductiontoTransportationDokumen23 halaman01 IntroductiontoTransportationDeepak ShoriBelum ada peringkat

- Shipping Finance Securitization Structure SPV IssuesDokumen2 halamanShipping Finance Securitization Structure SPV IssuesDeepak Shori100% (1)

- Port Agency 2014Dokumen3 halamanPort Agency 2014Deepak Shori100% (1)

- Ics Exams 2013 Questions SSPDokumen2 halamanIcs Exams 2013 Questions SSPDeepak ShoriBelum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)