Anda mungkin juga menyukai

- Trust AccountingDokumen13 halamanTrust AccountingPriyalaxmi Uma100% (4)

- Offshore Trust Lecture 3Dokumen14 halamanOffshore Trust Lecture 3Raveesh HurhangeeBelum ada peringkat

- Basics of Trusts - Beneficiaries, Vesting, TaxationDokumen18 halamanBasics of Trusts - Beneficiaries, Vesting, TaxationBhuvan100% (1)

- Estates and TrustsDokumen56 halamanEstates and TrustsRa El100% (4)

- Beat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012Dari EverandBeat Estate Tax Forever: The Unprecedented $5 Million Opportunity in 2012Belum ada peringkat

- Raising Money – Legally: A Practical Guide to Raising CapitalDari EverandRaising Money – Legally: A Practical Guide to Raising CapitalPenilaian: 4 dari 5 bintang4/5 (1)

- Under The Radar How To Protect And Maintain Your Own Financial Fortress By Flying Under The RadarDari EverandUnder The Radar How To Protect And Maintain Your Own Financial Fortress By Flying Under The RadarBelum ada peringkat

- Securitized Real Estate and 1031 ExchangesDari EverandSecuritized Real Estate and 1031 ExchangesBelum ada peringkat

- Asset ProtectionDokumen2 halamanAsset Protection05C1LL473Belum ada peringkat

- Insider Investment GuideDokumen273 halamanInsider Investment GuideFhélixAbel LoyaBelum ada peringkat

- Bus Org TrustDokumen11 halamanBus Org TrustFarizah Joy Pedroso BagundangBelum ada peringkat

- Private Placement Memorandum Blackcommerce, LLC: Page 1 of 111Dokumen112 halamanPrivate Placement Memorandum Blackcommerce, LLC: Page 1 of 111Viper 6058100% (1)

- The Massachusetts Business Trust and Registered Investment Companies PDFDokumen38 halamanThe Massachusetts Business Trust and Registered Investment Companies PDFed_nyc100% (2)

- 1 Requirements of An Express Private TrustDokumen14 halaman1 Requirements of An Express Private TrustDhabitah AdrianaBelum ada peringkat

- Free Business Trust ManualDokumen101 halamanFree Business Trust ManualHarry100% (5)

- Guide To Family TrustsDokumen20 halamanGuide To Family TruststestnationBelum ada peringkat

- Debt InstrumentsDokumen5 halamanDebt InstrumentsŚáńtőśh MőkáśhíBelum ada peringkat

- 1895 Trust Business PlanDokumen8 halaman1895 Trust Business Planthe1895trustBelum ada peringkat

- How Corporations Issue SecuritiesDokumen22 halamanHow Corporations Issue Securitieskaylakshmi8314Belum ada peringkat

- The Uncorporation Unleashing The Power of The Business Trust ForDokumen94 halamanThe Uncorporation Unleashing The Power of The Business Trust ForT Austin100% (10)

- Wyoming Dynasty Trust Seminar OutlineDokumen19 halamanWyoming Dynasty Trust Seminar Outlineplasma411nyBelum ada peringkat

- Business TrustDokumen6 halamanBusiness TrustsentinelionBelum ada peringkat

- TrustDokumen91 halamanTrustmohiuddinduo593% (14)

- How The Rich Stay Rich - Using A Family Trust Company To Secure ADokumen51 halamanHow The Rich Stay Rich - Using A Family Trust Company To Secure Aspcbanking100% (4)

- Holding Co.Dokumen78 halamanHolding Co.Anonymous ckTjn7RCq8100% (1)

- Express Trusts Under Common LawDokumen52 halamanExpress Trusts Under Common LawPawPaul Mccoy100% (9)

- A Trust Can Either Be A Private Trust or A Public Charitable TrustDokumen2 halamanA Trust Can Either Be A Private Trust or A Public Charitable TrustShwetaHarlalkaBelum ada peringkat

- Choice Is YoursDokumen23 halamanChoice Is Yoursffmaer100% (2)

- Unincorporated Business TrustDokumen9 halamanUnincorporated Business TrustSpencerRyanOneal98% (41)

- Business TrustDokumen5 halamanBusiness Trustempoweredwendy758867% (3)

- Designing An Income Only Irrevocable TrustDokumen15 halamanDesigning An Income Only Irrevocable Trusttaurusho100% (2)

- Chapter 11 Trustee HandbookDokumen84 halamanChapter 11 Trustee HandbookCj CrowellBelum ada peringkat

- Irrevocable TrustDokumen4 halamanIrrevocable TrustNelson Harris100% (1)

- Articles of AssociationDokumen2 halamanArticles of AssociationMadan MathodBelum ada peringkat

- The Law of Trusts PDFDokumen396 halamanThe Law of Trusts PDFlee sands100% (2)

- Private Money Presentation 2019Dokumen21 halamanPrivate Money Presentation 2019asegurado100% (2)

- Southpac Trust - Offshore Trustee ServicesDokumen5 halamanSouthpac Trust - Offshore Trustee Servicesomninetltd100% (1)

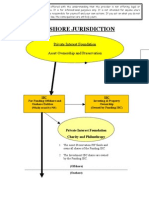

- TRUSTDokumen19 halamanTRUSTOffshore Company FormationBelum ada peringkat

- 0 Asset Protection BasicsDokumen43 halaman0 Asset Protection Basicspwilkers36100% (1)

- TrustDokumen30 halamanTrustWho moved my Cheese?100% (2)

- Wyoming Dynasty TrustsDokumen4 halamanWyoming Dynasty TrustsGonnellaAdamsonBelum ada peringkat

- Trust Law 1Dokumen49 halamanTrust Law 1QuYnii ShaFieBelum ada peringkat

- Family Trusts and Other TrustsDokumen5 halamanFamily Trusts and Other TrustsGreg Suefong100% (1)

- Corporate Trust SampleDokumen43 halamanCorporate Trust SampleCaesar Wilson100% (1)

- Family Trust Agreement SummaryDokumen13 halamanFamily Trust Agreement SummaryThileep100% (3)

- Private Purpose TrustsDokumen12 halamanPrivate Purpose Trustsxristianismos100% (1)

- Trust Law in Wealth Management and Estate PlanningDokumen986 halamanTrust Law in Wealth Management and Estate PlanningdbircS4264100% (2)

- Ucc 1Dokumen26 halamanUcc 1Carlton D WatsonBelum ada peringkat

- Trust Establishment SetupDokumen4 halamanTrust Establishment SetupAdv. Govind S. TehareBelum ada peringkat

- Ubot Pages From Book PDFDokumen9 halamanUbot Pages From Book PDFNaamir Wahiyd-BeyBelum ada peringkat

- Common Law Trust Unincorporated Business Trust Asset Protection Remedy (Protect Assets)Dokumen8 halamanCommon Law Trust Unincorporated Business Trust Asset Protection Remedy (Protect Assets)in1or86% (7)

- Unincorporated AssociationsDokumen8 halamanUnincorporated AssociationsxristianismosBelum ada peringkat

- Carlton A Weiss Na Crs 2006Dokumen49 halamanCarlton A Weiss Na Crs 2006MarkMatrix100% (8)

- Trust Accounting HandbookDokumen95 halamanTrust Accounting HandbookLuis RiquelmeBelum ada peringkat

- Private Trust CreationDokumen32 halamanPrivate Trust CreationArunaML100% (9)

- Living Estate Trust Proclamation - Nahveyah Analyse Israel BeyDokumen3 halamanLiving Estate Trust Proclamation - Nahveyah Analyse Israel Beydejure moorishe american justices100% (1)

- Lichtenstein Family TrustDokumen38 halamanLichtenstein Family TrustTerry Lichtenstein100% (1)

- The Natural Law Trust EbookDokumen90 halamanThe Natural Law Trust EbookSwank80% (5)

- LAVECO Newsletter 2018/1. - The Next Step: Total Financial Dictatorship!? Or, The Experiences From A Latvian Bank's BankruptcyDokumen10 halamanLAVECO Newsletter 2018/1. - The Next Step: Total Financial Dictatorship!? Or, The Experiences From A Latvian Bank's BankruptcyOffshore Company FormationBelum ada peringkat

- Offshore Goes To Paradise?! - LAVECO Newsletter 2017/4.Dokumen8 halamanOffshore Goes To Paradise?! - LAVECO Newsletter 2017/4.Offshore Company FormationBelum ada peringkat

- Company Formation in The United Arab Emirates (Ajman)Dokumen12 halamanCompany Formation in The United Arab Emirates (Ajman)Offshore Company FormationBelum ada peringkat

- 2017: The Year of PurgesDokumen12 halaman2017: The Year of PurgesOffshore Company FormationBelum ada peringkat

- Company Formation and Bank Account Opening in BulgariaDokumen22 halamanCompany Formation and Bank Account Opening in BulgariaOffshore Company FormationBelum ada peringkat

- Company Formation in The United Arab Emirates (Umm Al Quwain)Dokumen14 halamanCompany Formation in The United Arab Emirates (Umm Al Quwain)Offshore Company FormationBelum ada peringkat

- Company Formation in The United Arab Emirates (Sharjah)Dokumen14 halamanCompany Formation in The United Arab Emirates (Sharjah)Offshore Company FormationBelum ada peringkat

- LAVECO Newsletter 2017/2. - Business Is Moving To The NetDokumen10 halamanLAVECO Newsletter 2017/2. - Business Is Moving To The NetOffshore Company FormationBelum ada peringkat

- Is It Worth Hiding Money Abroad? - Newsletter 2017/3Dokumen9 halamanIs It Worth Hiding Money Abroad? - Newsletter 2017/3Offshore Company FormationBelum ada peringkat

- Company Formation in The SeychellesDokumen12 halamanCompany Formation in The SeychellesOffshore Company FormationBelum ada peringkat

- LAVECO Newsletter June, 2016 - Panama Papers, Bahamas Papers, UK Papers, Germany Papers, USA Papers, ..... ?Dokumen8 halamanLAVECO Newsletter June, 2016 - Panama Papers, Bahamas Papers, UK Papers, Germany Papers, USA Papers, ..... ?Offshore Company FormationBelum ada peringkat

- LAVECO Newsletter 2016/2. - Is There Another 25 Years in LAVECO LTD.?Dokumen10 halamanLAVECO Newsletter 2016/2. - Is There Another 25 Years in LAVECO LTD.?Offshore Company FormationBelum ada peringkat

- So What Will Offshore Companies Be Good For, If All Money Will Be "White"? - LAVECO Newsletter 2014/2.Dokumen8 halamanSo What Will Offshore Companies Be Good For, If All Money Will Be "White"? - LAVECO Newsletter 2014/2.Offshore Company FormationBelum ada peringkat

- Nude Banking - LAVECO Newsletter 2015/3.Dokumen7 halamanNude Banking - LAVECO Newsletter 2015/3.Offshore Company FormationBelum ada peringkat

- 5 Minutes Offshore - Cyprus: Resident, But Not Domiciled"Dokumen4 halaman5 Minutes Offshore - Cyprus: Resident, But Not Domiciled"Offshore Company FormationBelum ada peringkat

- The Cyprus CompanyDokumen54 halamanThe Cyprus CompanyOffshore Company FormationBelum ada peringkat

- Why Will It Still Be Worth Operating Offshore Companies in The Future?Dokumen15 halamanWhy Will It Still Be Worth Operating Offshore Companies in The Future?Offshore Company FormationBelum ada peringkat

- Offshore 2.0 - LAVECO Newsletter 2015/2.Dokumen8 halamanOffshore 2.0 - LAVECO Newsletter 2015/2.Offshore Company FormationBelum ada peringkat

- The Secrets of Offshore Banking - Part OneDokumen5 halamanThe Secrets of Offshore Banking - Part OneOffshore Company FormationBelum ada peringkat

- LAVECO Newsletter 2014/4. - Won't It Be Any Easier Next Year Either?Dokumen9 halamanLAVECO Newsletter 2014/4. - Won't It Be Any Easier Next Year Either?Offshore Company FormationBelum ada peringkat

- Company Formation and Bank Account Opening in Hong KongDokumen26 halamanCompany Formation and Bank Account Opening in Hong KongOffshore Company FormationBelum ada peringkat

- Will The World Be Different Without Offshore Structures? - LAVECO Newsletter 2015/1.Dokumen10 halamanWill The World Be Different Without Offshore Structures? - LAVECO Newsletter 2015/1.Offshore Company FormationBelum ada peringkat

- The End of Offshore: Repeated Ad Nauseam - LAVECO Newsletter 2014/1.Dokumen8 halamanThe End of Offshore: Repeated Ad Nauseam - LAVECO Newsletter 2014/1.Offshore Company FormationBelum ada peringkat

- Company Formation in HungaryDokumen28 halamanCompany Formation in HungaryOffshore Company FormationBelum ada peringkat

- Fiduciary ServicesDokumen9 halamanFiduciary ServicesOffshore Company FormationBelum ada peringkat

- Offshore Company Formation For More Than 40 Offshore Jurisdictions.Dokumen31 halamanOffshore Company Formation For More Than 40 Offshore Jurisdictions.Offshore Company Formation100% (1)

- TRUSTDokumen19 halamanTRUSTOffshore Company FormationBelum ada peringkat

- Fiduciary ServicesDokumen9 halamanFiduciary ServicesOffshore Company FormationBelum ada peringkat

- Real Estate Joint Venture DealDokumen5 halamanReal Estate Joint Venture DealRheneir Mora100% (3)

- Seville Sept13Dokumen25 halamanSeville Sept13Robin SpencerBelum ada peringkat

- Piercing Corporate Veil Doctrine Explained in Dispute over Machinery OwnershipDokumen4 halamanPiercing Corporate Veil Doctrine Explained in Dispute over Machinery OwnershipArnel ManalastasBelum ada peringkat

- MC QuestionsDokumen23 halamanMC QuestionsBob Sagett0% (5)

- G.R. No. 156956Dokumen17 halamanG.R. No. 156956Ayvee BlanchBelum ada peringkat

- Guide to Setting Up Benevolence FundsDokumen2 halamanGuide to Setting Up Benevolence Fundswajidkhan_imsBelum ada peringkat

- (1922) 1 Ch. 75Dokumen11 halaman(1922) 1 Ch. 75PeterBelum ada peringkat

- Collection Information Statement For Wage Earners and Self-Employed IndividualsDokumen7 halamanCollection Information Statement For Wage Earners and Self-Employed IndividualsAnonymous dfLfinUrp60% (5)

- Executor of The Irs Decedent Estate EntityDokumen81 halamanExecutor of The Irs Decedent Estate Entitylivingdaughter98% (47)

- Tax1 Final Landmark Case DigestDokumen29 halamanTax1 Final Landmark Case DigestasterBelum ada peringkat

- Serrano v. Central BankDokumen4 halamanSerrano v. Central BankWilfredo MolinaBelum ada peringkat

- Marital Settlement AgreementDokumen24 halamanMarital Settlement AgreementDaniela Herrero100% (1)

- Bankruptcy Expert ReportDokumen14 halamanBankruptcy Expert ReportDarren ChakerBelum ada peringkat

- Alito 2022 Financial DisclosureDokumen13 halamanAlito 2022 Financial DisclosureJimmy HooverBelum ada peringkat

- Sotto vs. TevesDokumen10 halamanSotto vs. TevesFranzMordenoBelum ada peringkat

- Tax-2Dokumen118 halamanTax-2ethel hyugaBelum ada peringkat

- EH405 ATP WWW - Midterm ExamDokumen3 halamanEH405 ATP WWW - Midterm ExamJandi Yang100% (1)

- Original PDF Introduction To Law 6th by Joanne B Hames PDFDokumen42 halamanOriginal PDF Introduction To Law 6th by Joanne B Hames PDFpearl.zinn592100% (32)

- Difference Between Trust & WakfDokumen1 halamanDifference Between Trust & WakfMRINMAY KUSHALBelum ada peringkat

- Court Rules in Favor of Respondents in Land Dispute CaseDokumen130 halamanCourt Rules in Favor of Respondents in Land Dispute CaseDianahAlcazarBelum ada peringkat

- Salas v. AboitizDokumen1 halamanSalas v. AboitizRuss TuazonBelum ada peringkat

- Spouses Armando and Lorna TRINIDAD, Petitioners, vs. DONA Glenn IMSON, RespondentDokumen9 halamanSpouses Armando and Lorna TRINIDAD, Petitioners, vs. DONA Glenn IMSON, RespondentMazaya VillameBelum ada peringkat

- Deposit SchemesDokumen57 halamanDeposit Schemesnarendar.1Belum ada peringkat

- One Person CorporationDokumen7 halamanOne Person CorporationBenedict IloseoBelum ada peringkat

- Arlegui Vs CA-ReadDokumen12 halamanArlegui Vs CA-ReadPatrick TanBelum ada peringkat

- Concept of Updating The Civil Code of UkraineDokumen111 halamanConcept of Updating The Civil Code of UkraineIlinca TurcanuBelum ada peringkat

- 099-Nidc vs. Aquino 163 Scra 153Dokumen12 halaman099-Nidc vs. Aquino 163 Scra 153wewBelum ada peringkat

- Third Verified Motion To Disqualify Circuit Judge Ann Melinda CraggsDokumen102 halamanThird Verified Motion To Disqualify Circuit Judge Ann Melinda CraggsNeil GillespieBelum ada peringkat

- Charitable & Religious Trusts Act 1920 PDFDokumen6 halamanCharitable & Religious Trusts Act 1920 PDFJay KothariBelum ada peringkat