Anda mungkin juga menyukai

- Fuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryDari EverandFuel Pumps & Fuel Tanks (C.V. OE & Aftermarket) World Summary: Market Values & Financials by CountryBelum ada peringkat

- Year Ended 53Dokumen24 halamanYear Ended 53ashokdb2kBelum ada peringkat

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryDari EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryBelum ada peringkat

- Rio Tinto Delivers First Half Underlying Earnings of 2.9 BillionDokumen58 halamanRio Tinto Delivers First Half Underlying Earnings of 2.9 BillionBisto MasiloBelum ada peringkat

- Fuel Pumps & Fuel Tanks (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryDari EverandFuel Pumps & Fuel Tanks (Car OE & Aftermarket) World Summary: Market Values & Financials by CountryBelum ada peringkat

- 1H15 PPT - VFDokumen29 halaman1H15 PPT - VFClaudio Andrés De LucaBelum ada peringkat

- Maruti India Limited: SuzukiDokumen13 halamanMaruti India Limited: SuzukiHemant Raj DixitBelum ada peringkat

- Interim Report Interim ReportDokumen34 halamanInterim Report Interim ReportMohammed AbdoBelum ada peringkat

- Results Conference CallDokumen14 halamanResults Conference CallLightRIBelum ada peringkat

- Earnings ReleaseDokumen8 halamanEarnings ReleaseBVMF_RIBelum ada peringkat

- Rio Tinto Alcan: Financial Community Site VisitDokumen22 halamanRio Tinto Alcan: Financial Community Site Visitmythos1976Belum ada peringkat

- Presentation (Company Update)Dokumen25 halamanPresentation (Company Update)Shyam SunderBelum ada peringkat

- 4Q15 PresentationDokumen21 halaman4Q15 PresentationMultiplan RIBelum ada peringkat

- 3Q15 PresentationDokumen16 halaman3Q15 PresentationMultiplan RIBelum ada peringkat

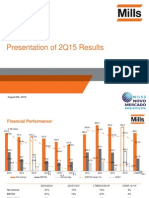

- 2Q15 Presentation of ResultsDokumen30 halaman2Q15 Presentation of ResultsMillsRIBelum ada peringkat

- QCOM Alignment PlanDokumen17 halamanQCOM Alignment Planmtan88Belum ada peringkat

- 4Q15 Earnings PresentationDokumen14 halaman4Q15 Earnings PresentationFibriaRIBelum ada peringkat

- Earnings ReleaseDokumen9 halamanEarnings ReleaseBVMF_RIBelum ada peringkat

- Earnings ReleaseDokumen15 halamanEarnings ReleaseMultiplan RIBelum ada peringkat

- Third Quarter Report March 31 2014Dokumen36 halamanThird Quarter Report March 31 2014Salman MohiuddinBelum ada peringkat

- 2015 04 Investor PresentationDokumen37 halaman2015 04 Investor PresentationsidBelum ada peringkat

- Presentation 1Q15Dokumen14 halamanPresentation 1Q15Multiplan RIBelum ada peringkat

- 2Q15 PresentationDokumen16 halaman2Q15 PresentationMultiplan RIBelum ada peringkat

- Quarterly Report 1Q08: EBITDA of 1Q08 Reaches R$ 205 Million, With 28% MarginDokumen17 halamanQuarterly Report 1Q08: EBITDA of 1Q08 Reaches R$ 205 Million, With 28% MarginKlabin_RIBelum ada peringkat

- Results Conference Call: 2009 Third QuarterDokumen17 halamanResults Conference Call: 2009 Third QuarterLightRIBelum ada peringkat

- Fiscal Management Report 2016Dokumen123 halamanFiscal Management Report 2016Ada DeranaBelum ada peringkat

- Caterpillar Inc.: 3Q 2009 Earnings ReleaseDokumen34 halamanCaterpillar Inc.: 3Q 2009 Earnings ReleaseqtipxBelum ada peringkat

- Talgo 1H2015 Results PresentationDokumen18 halamanTalgo 1H2015 Results PresentationTail RiskBelum ada peringkat

- 2015 Interim Results PresentationDokumen30 halaman2015 Interim Results PresentationAnonymous 6tuR1hzBelum ada peringkat

- Quarterly GDP Publication - Q2 2015Dokumen4 halamanQuarterly GDP Publication - Q2 2015Anonymous UpWci5Belum ada peringkat

- FullYear2014 ResultsPresentationDokumen31 halamanFullYear2014 ResultsPresentationkaze_no_taniBelum ada peringkat

- Sun Microsystems Q107 Quarterly Results Release: Investor RelationsDokumen39 halamanSun Microsystems Q107 Quarterly Results Release: Investor RelationsjohnachanBelum ada peringkat

- FXCM Q1 2014 Earnings PresentationDokumen21 halamanFXCM Q1 2014 Earnings PresentationRon FinbergBelum ada peringkat

- 1Q14 Presentation of ResultsDokumen16 halaman1Q14 Presentation of ResultsMillsRIBelum ada peringkat

- Financial Results With Results Press Release & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Dokumen5 halamanFinancial Results With Results Press Release & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderBelum ada peringkat

- Next PLC - Press ReleaseDokumen20 halamanNext PLC - Press Releasecasefortrils0% (1)

- Saipem - Sem15IngDokumen116 halamanSaipem - Sem15IngJohn KentBelum ada peringkat

- Tata Power (TATPOW) : Lower Coal Price Dents Margin of Coal SPVDokumen13 halamanTata Power (TATPOW) : Lower Coal Price Dents Margin of Coal SPVGauriGanBelum ada peringkat

- Can Q3 FY09 FinancialResultsDokumen42 halamanCan Q3 FY09 FinancialResultsAppu Moments MatterBelum ada peringkat

- Puma Energy - Results Report - Q1 2016Dokumen10 halamanPuma Energy - Results Report - Q1 2016KA-11 Єфіменко ІванBelum ada peringkat

- 2Q 2010 Release Eng FinalDokumen9 halaman2Q 2010 Release Eng FinalAlexander ChesnkovBelum ada peringkat

- 1Q15 Presentation of ResultsDokumen20 halaman1Q15 Presentation of ResultsMillsRIBelum ada peringkat

- BM&FBOVESPA S.A. Announces Earnings For The Second Quarter of 2010Dokumen15 halamanBM&FBOVESPA S.A. Announces Earnings For The Second Quarter of 2010BVMF_RIBelum ada peringkat

- English Ratio Analysis For Real-Estate CompanyDokumen14 halamanEnglish Ratio Analysis For Real-Estate CompanyMohamad RizwanBelum ada peringkat

- KPIT Technologies: IT Services Sector Outlook - NeutralDokumen9 halamanKPIT Technologies: IT Services Sector Outlook - NeutralgirishrajsBelum ada peringkat

- Quarterly Report 3Q08: Klabin Concludes MA 1100 Expansion Project With A Solid Cash PositionDokumen15 halamanQuarterly Report 3Q08: Klabin Concludes MA 1100 Expansion Project With A Solid Cash PositionKlabin_RIBelum ada peringkat

- Communication To Investors - June 2015 (Company Update)Dokumen11 halamanCommunication To Investors - June 2015 (Company Update)Shyam SunderBelum ada peringkat

- GOME 2012Q3 Results en Final 1700Dokumen30 halamanGOME 2012Q3 Results en Final 1700Deniz TuracBelum ada peringkat

- Conference CallDokumen15 halamanConference CallLightRIBelum ada peringkat

- Call 4T09 ENG FinalDokumen10 halamanCall 4T09 ENG FinalFibriaRIBelum ada peringkat

- 1Q15 Earnings PresentationDokumen12 halaman1Q15 Earnings PresentationFibriaRIBelum ada peringkat

- BHP Billiton Results For The Half Year Ended 31 December 2013Dokumen40 halamanBHP Billiton Results For The Half Year Ended 31 December 2013digifi100% (1)

- CSX Q1 2014 EarningsDokumen14 halamanCSX Q1 2014 EarningsFelipe TojaBelum ada peringkat

- Results Conference Call: 2009 Second QuarterDokumen18 halamanResults Conference Call: 2009 Second QuarterLightRIBelum ada peringkat

- Alok - Performance Report - q4 2010-11Dokumen24 halamanAlok - Performance Report - q4 2010-11Krishna VaniaBelum ada peringkat

- Klabin Webcast 20101 Q10Dokumen10 halamanKlabin Webcast 20101 Q10Klabin_RIBelum ada peringkat

- Financial Results & Limited Review Report For Sept 30, 2015 (Result)Dokumen11 halamanFinancial Results & Limited Review Report For Sept 30, 2015 (Result)Shyam SunderBelum ada peringkat

- 2014 Full-Year Results Briefing PresentationDokumen75 halaman2014 Full-Year Results Briefing PresentationRachelLooBelum ada peringkat

- Siemens 2020 VisionDokumen46 halamanSiemens 2020 VisionSudeep KeshriBelum ada peringkat

- Schlumberger Announces Third-Quarter 2018 ResultsDokumen12 halamanSchlumberger Announces Third-Quarter 2018 ResultsYves-donald MakoumbouBelum ada peringkat

- September 2015Dokumen14 halamanSeptember 2015api-307565920Belum ada peringkat

- Condensed Combined Interim Financial Statements Cpsa and Related Cos September 30 2015Dokumen42 halamanCondensed Combined Interim Financial Statements Cpsa and Related Cos September 30 2015api-307565920Belum ada peringkat

- Ws Refe 20151016033538 Tsl2prod 109616Dokumen285 halamanWs Refe 20151016033538 Tsl2prod 109616api-30756592050% (2)

- Tigo Ws Refe 20150511220956 Tsl1prod 41089Dokumen266 halamanTigo Ws Refe 20150511220956 Tsl1prod 41089api-307565920Belum ada peringkat

- Mda q3-2015 FinalDokumen14 halamanMda q3-2015 Finalapi-307565920Belum ada peringkat

- 1986 Elektric M InfoDokumen1 halaman1986 Elektric M InfoDanielDiasBelum ada peringkat

- " Thou Hast Made Me, and Shall Thy Work Decay?Dokumen2 halaman" Thou Hast Made Me, and Shall Thy Work Decay?Sbgacc SojitraBelum ada peringkat

- Entrep Bazaar Rating SheetDokumen7 halamanEntrep Bazaar Rating SheetJupiter WhitesideBelum ada peringkat

- Conductivity MeterDokumen59 halamanConductivity MeterMuhammad AzeemBelum ada peringkat

- FPSCDokumen15 halamanFPSCBABER SULTANBelum ada peringkat

- Ollie Nathan Harris v. United States, 402 F.2d 464, 10th Cir. (1968)Dokumen2 halamanOllie Nathan Harris v. United States, 402 F.2d 464, 10th Cir. (1968)Scribd Government DocsBelum ada peringkat

- 60617-7 1996Dokumen64 halaman60617-7 1996SuperhypoBelum ada peringkat

- TestDokumen56 halamanTestFajri Love PeaceBelum ada peringkat

- Theo Hermans (Cáp. 3)Dokumen3 halamanTheo Hermans (Cáp. 3)cookinglike100% (1)

- Outline - Criminal Law - RamirezDokumen28 halamanOutline - Criminal Law - RamirezgiannaBelum ada peringkat

- Economies of Scale in European Manufacturing Revisited: July 2001Dokumen31 halamanEconomies of Scale in European Manufacturing Revisited: July 2001vladut_stan_5Belum ada peringkat

- Alcatraz Analysis (With Explanations)Dokumen16 halamanAlcatraz Analysis (With Explanations)Raul Dolo Quinones100% (1)

- CGP Module 1 FinalDokumen19 halamanCGP Module 1 Finaljohn lexter emberadorBelum ada peringkat

- Logic of English - Spelling Rules PDFDokumen3 halamanLogic of English - Spelling Rules PDFRavinder Kumar80% (15)

- Wetlands Denote Perennial Water Bodies That Originate From Underground Sources of Water or RainsDokumen3 halamanWetlands Denote Perennial Water Bodies That Originate From Underground Sources of Water or RainsManish thapaBelum ada peringkat

- Applied Thermodynamics - DraughtDokumen22 halamanApplied Thermodynamics - Draughtpiyush palBelum ada peringkat

- Nandurbar District S.E. (CGPA) Nov 2013Dokumen336 halamanNandurbar District S.E. (CGPA) Nov 2013Digitaladda IndiaBelum ada peringkat

- Hypnosis ScriptDokumen3 halamanHypnosis ScriptLuca BaroniBelum ada peringkat

- TN Vision 2023 PDFDokumen68 halamanTN Vision 2023 PDFRajanbabu100% (1)

- Medicidefamilie 2011Dokumen6 halamanMedicidefamilie 2011Mesaros AlexandruBelum ada peringkat

- Syllabus Biomekanika Kerja 2012 1Dokumen2 halamanSyllabus Biomekanika Kerja 2012 1Lukman HakimBelum ada peringkat

- Cambridge IGCSE Business Studies 4th Edition © Hodder & Stoughton LTD 2013Dokumen1 halamanCambridge IGCSE Business Studies 4th Edition © Hodder & Stoughton LTD 2013RedrioxBelum ada peringkat

- Grossman 1972 Health CapitalDokumen33 halamanGrossman 1972 Health CapitalLeonardo SimonciniBelum ada peringkat

- Physiology PharmacologyDokumen126 halamanPhysiology PharmacologyuneedlesBelum ada peringkat

- Tangazo La Kazi October 29, 2013 PDFDokumen32 halamanTangazo La Kazi October 29, 2013 PDFRashid BumarwaBelum ada peringkat

- DMSCO Log Book Vol.25 1947Dokumen49 halamanDMSCO Log Book Vol.25 1947Des Moines University Archives and Rare Book RoomBelum ada peringkat

- Language Analysis - GRAMMAR/FUNCTIONS Context Anticipated ProblemsDokumen2 halamanLanguage Analysis - GRAMMAR/FUNCTIONS Context Anticipated Problemsshru_edgyBelum ada peringkat

- Undertaking:-: Prime Membership Application Form (Fill With All Capital Letters)Dokumen3 halamanUndertaking:-: Prime Membership Application Form (Fill With All Capital Letters)Anuj ManglaBelum ada peringkat

- Debarchana TrainingDokumen45 halamanDebarchana TrainingNitin TibrewalBelum ada peringkat

- What Is A Designer Norman PotterDokumen27 halamanWhat Is A Designer Norman PotterJoana Sebastião0% (1)