Anda mungkin juga menyukai

- rp5301fs Prop Tax Facts PDFDokumen2 halamanrp5301fs Prop Tax Facts PDFjspectorBelum ada peringkat

- Tax Freeze Guidance DocumentDokumen20 halamanTax Freeze Guidance DocumentjspectorBelum ada peringkat

- 2012 Tax Rate ReportDokumen88 halaman2012 Tax Rate ReportZoe GallandBelum ada peringkat

- 16 Don'T-Miss Tax DeductionsDokumen4 halaman16 Don'T-Miss Tax DeductionsGon FloBelum ada peringkat

- Cut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesDari EverandCut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesBelum ada peringkat

- NY COVID Rent ReliefDokumen2 halamanNY COVID Rent ReliefJoe SpectorBelum ada peringkat

- Intrim Union Budget 2019-20Dokumen12 halamanIntrim Union Budget 2019-20Rukmani GuptaBelum ada peringkat

- Pro Mortgage Interest Tax Deduction: Ashley Sadighpour, Charlene Shi, Jeremy Sauvage, Nick Segal, & Matt WagonhurstDokumen8 halamanPro Mortgage Interest Tax Deduction: Ashley Sadighpour, Charlene Shi, Jeremy Sauvage, Nick Segal, & Matt WagonhurstJiayu JinBelum ada peringkat

- County Administrator 2017 Budget MemoDokumen20 halamanCounty Administrator 2017 Budget MemoFauquier NowBelum ada peringkat

- Quick Notes on “The Trump Tax Cut: Your Personal Guide to the New Tax Law by Eva Rosenberg”Dari EverandQuick Notes on “The Trump Tax Cut: Your Personal Guide to the New Tax Law by Eva Rosenberg”Belum ada peringkat

- Forbes 2018 Tax GuideDokumen16 halamanForbes 2018 Tax GuideJerry WhittonBelum ada peringkat

- Tax Update 2009Dokumen2 halamanTax Update 2009calebwoodsBelum ada peringkat

- 2011 Tax Reference GuideDokumen11 halaman2011 Tax Reference GuideSaver PlusBelum ada peringkat

- Session 23-25 Permissible Deduction From Gross Total IncomeDokumen14 halamanSession 23-25 Permissible Deduction From Gross Total Incomeomar zohorianBelum ada peringkat

- Revenue Sharing ReportDokumen12 halamanRevenue Sharing ReportMaine Policy InstituteBelum ada peringkat

- House PropertyDokumen19 halamanHouse PropertyChandraBelum ada peringkat

- Income Tax ReturnDokumen57 halamanIncome Tax ReturnMalik WasimBelum ada peringkat

- Taxes and InsuranceDokumen14 halamanTaxes and InsuranceAbdullah RamzanBelum ada peringkat

- 2023 Proposed Fauquier Budget SummaryDokumen24 halaman2023 Proposed Fauquier Budget SummaryFauquier NowBelum ada peringkat

- Atlantic City Recovery Plan in Brief 10.24.2016 - FINALDokumen23 halamanAtlantic City Recovery Plan in Brief 10.24.2016 - FINALPress of Atlantic CityBelum ada peringkat

- A. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductionDokumen67 halamanA. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductioncjleopBelum ada peringkat

- Real Estate Recapture TaxDokumen5 halamanReal Estate Recapture TaxmpboxeBelum ada peringkat

- Investment Submission Guidelines For F.Y. 2022-23Dokumen13 halamanInvestment Submission Guidelines For F.Y. 2022-23harikrushnaBelum ada peringkat

- Joint Tax Hearing-Ron DeutschDokumen18 halamanJoint Tax Hearing-Ron DeutschZacharyEJWilliamsBelum ada peringkat

- Evaluating School Funding ProposalsDokumen8 halamanEvaluating School Funding ProposalspublicschoolnotebookBelum ada peringkat

- CCH Federal Taxation Comprehensive Topics 2013 1st Edition Harmelink Test Bank DownloadDokumen27 halamanCCH Federal Taxation Comprehensive Topics 2013 1st Edition Harmelink Test Bank DownloadCecelia Taylor100% (23)

- BTC Reports - Final Tax Plan2013Dokumen10 halamanBTC Reports - Final Tax Plan2013CarolinaMercuryBelum ada peringkat

- Surviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesDari EverandSurviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesBelum ada peringkat

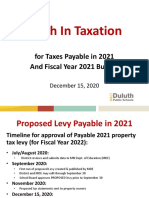

- Truth in Taxation: For Taxes Payable in 2021 and Fiscal Year 2021 BudgetDokumen12 halamanTruth in Taxation: For Taxes Payable in 2021 and Fiscal Year 2021 BudgetDuluth News TribuneBelum ada peringkat

- Affordable Housing FAQs 7-28-2014Dokumen1 halamanAffordable Housing FAQs 7-28-2014Josh YamatBelum ada peringkat

- Severance and Lump Sum Withholding Tax RatesDokumen1 halamanSeverance and Lump Sum Withholding Tax RatesAnonymous HbOTj4Belum ada peringkat

- Home Loan Update 002842 PDFDokumen1 halamanHome Loan Update 002842 PDFShannon SmithBelum ada peringkat

- Deductions Under Section 80C For Investments in The Indian It Act 1961Dokumen20 halamanDeductions Under Section 80C For Investments in The Indian It Act 1961saurav-maitra-3114Belum ada peringkat

- Rebates For First Time BuyersDokumen5 halamanRebates For First Time BuyersjohnBelum ada peringkat

- Budget 2010-11: by Karan Singh, MBA (General) Section - ADokumen32 halamanBudget 2010-11: by Karan Singh, MBA (General) Section - AscherrercuteBelum ada peringkat

- Comparison Between I.T. and DTCDokumen23 halamanComparison Between I.T. and DTCsharma.shalinee1626Belum ada peringkat

- BudgetDokumen21 halamanBudgetshweta_narkhede01Belum ada peringkat

- Executive Summary:: Tax Restructuring Policy ProposalDokumen6 halamanExecutive Summary:: Tax Restructuring Policy ProposalThe Salt Lake TribuneBelum ada peringkat

- County Manager's Presentation To Rockingham County Board of Commissioners For 2018/19 Budget.Dokumen22 halamanCounty Manager's Presentation To Rockingham County Board of Commissioners For 2018/19 Budget.jeffreyhsykesBelum ada peringkat

- Tax Insight February 2016Dokumen1 halamanTax Insight February 2016banks305Belum ada peringkat

- GOP Tax Bill HighlightsDokumen2 halamanGOP Tax Bill HighlightsWashington Examiner100% (1)

- Taxes: Tax StructureDokumen14 halamanTaxes: Tax StructurePradeep NairBelum ada peringkat

- Homeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransDari EverandHomeowner's Simple Guide to Property Tax Protest: Whats key: Exemptions & Deductions Blind. Disabled. Over 65. Property Rehabilitation. VeteransBelum ada peringkat

- 2012 Kentucky Individual Income Tax Forms: WWW - Revenue.ky - GovDokumen76 halaman2012 Kentucky Individual Income Tax Forms: WWW - Revenue.ky - GovJason GrohBelum ada peringkat

- Tax Changes in India and Morocco Taxation CiaDokumen20 halamanTax Changes in India and Morocco Taxation CiaMEERA JOSHY 1927436Belum ada peringkat

- Livingston County Adopted Budget (2023)Dokumen401 halamanLivingston County Adopted Budget (2023)Watertown Daily TimesBelum ada peringkat

- Tax FinalDokumen21 halamanTax Finalshweta_narkhede01Belum ada peringkat

- Bank of North Dakota Buydown ProgramDokumen3 halamanBank of North Dakota Buydown ProgramJeremy TurleyBelum ada peringkat

- Tax and SuperDokumen3 halamanTax and SuperEmmaBelum ada peringkat

- VFN Tax and Tax Saving Session 2015Dokumen27 halamanVFN Tax and Tax Saving Session 2015Sumit BawejaBelum ada peringkat

- SUPPORT ActDokumen5 halamanSUPPORT ActMary Claire PattonBelum ada peringkat

- Deductions 3Dokumen35 halamanDeductions 3sanjeev kumar vsBelum ada peringkat

- FY 16 Analysis of Introduced Budget 102115Dokumen65 halamanFY 16 Analysis of Introduced Budget 102115The Daily LineBelum ada peringkat

- Maryland Mortgage Program - Recapture TaxDokumen12 halamanMaryland Mortgage Program - Recapture TaxNishika JGBelum ada peringkat

- Form 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsDokumen9 halamanForm 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsBrokerABelum ada peringkat

- Income TaxationDokumen12 halamanIncome TaxationMonica Jarabelo RamintasBelum ada peringkat

- Midterm - Theory ReviewDokumen18 halamanMidterm - Theory ReviewCameron BelangerBelum ada peringkat

- Week 3-Local TaxationDokumen23 halamanWeek 3-Local TaxationShanique WilliamsBelum ada peringkat

- Understanding Income TaxDokumen31 halamanUnderstanding Income TaxRajesh RoatBelum ada peringkat

- Clarksburg Sewer Extension Groundbreaking InvitationDokumen1 halamanClarksburg Sewer Extension Groundbreaking InvitationPublic Information OfficeBelum ada peringkat

- Christmas Tree UO 11192021Dokumen1 halamanChristmas Tree UO 11192021Public Information OfficeBelum ada peringkat

- 9th Annual Senior Safety Forum World Elder Abuse Awareness DayDokumen1 halaman9th Annual Senior Safety Forum World Elder Abuse Awareness DayPublic Information OfficeBelum ada peringkat

- Cyber Threat Actors Are Impersonating Maryland Government Agencies in Phishing SchemesDokumen2 halamanCyber Threat Actors Are Impersonating Maryland Government Agencies in Phishing SchemesPublic Information OfficeBelum ada peringkat

- Caregiver Flyer 8.5x11-2019Dokumen1 halamanCaregiver Flyer 8.5x11-2019Public Information OfficeBelum ada peringkat

- Letter To TPB Rep. RaskinDokumen1 halamanLetter To TPB Rep. RaskinPublic Information OfficeBelum ada peringkat

- Bike To Work Day - SponsorsDokumen1 halamanBike To Work Day - SponsorsPublic Information OfficeBelum ada peringkat

- Beacon Celebration of The ArtsDokumen1 halamanBeacon Celebration of The ArtsPublic Information OfficeBelum ada peringkat

- Vital Living NetworkerDokumen34 halamanVital Living NetworkerPublic Information OfficeBelum ada peringkat

- Bethesda Bikeway Popup BTWRoute 05182018 V 4Dokumen1 halamanBethesda Bikeway Popup BTWRoute 05182018 V 4Public Information OfficeBelum ada peringkat

- Veto of Line Item in CIP Budget For Montgomery County's Clean Water and Permit Compliance ProgramDokumen2 halamanVeto of Line Item in CIP Budget For Montgomery County's Clean Water and Permit Compliance ProgramPublic Information OfficeBelum ada peringkat

- 7th Annual World Elder Abuse Awareness DayDokumen2 halaman7th Annual World Elder Abuse Awareness DayPublic Information OfficeBelum ada peringkat

- Minimum Wage Transition TableDokumen1 halamanMinimum Wage Transition TablePublic Information OfficeBelum ada peringkat

- Bike To Work Day - Spanish - SponsorsDokumen1 halamanBike To Work Day - Spanish - SponsorsPublic Information OfficeBelum ada peringkat

- The Time To Build: County Executive Ike Leggett Capital Improvement Projects 2007 - 2018Dokumen1 halamanThe Time To Build: County Executive Ike Leggett Capital Improvement Projects 2007 - 2018Public Information OfficeBelum ada peringkat

- D3 Lane Closures - 042718Dokumen8 halamanD3 Lane Closures - 042718Public Information OfficeBelum ada peringkat

- Bike To Work DayDokumen1 halamanBike To Work DayPublic Information OfficeBelum ada peringkat

- Age Friendly Advisory Presentation-010918Dokumen22 halamanAge Friendly Advisory Presentation-010918Public Information OfficeBelum ada peringkat

- Protecting Your Consumer Rights: What You Need To KnowDokumen1 halamanProtecting Your Consumer Rights: What You Need To KnowPublic Information OfficeBelum ada peringkat

- Leggett Announces County Suit Against 14 Opioid CompaniesDokumen163 halamanLeggett Announces County Suit Against 14 Opioid CompaniesPublic Information OfficeBelum ada peringkat

- County Executive Ike Leggett Developing A Recommended Saving Plan To Address FY18 Revenue ShortfallDokumen2 halamanCounty Executive Ike Leggett Developing A Recommended Saving Plan To Address FY18 Revenue ShortfallPublic Information OfficeBelum ada peringkat

- PSTA Open House - Flyer - 8.5x11 For WebsiteDokumen1 halamanPSTA Open House - Flyer - 8.5x11 For WebsitePublic Information OfficeBelum ada peringkat

- Transportation Options For Older Adults and People With DisabilitiesDokumen2 halamanTransportation Options For Older Adults and People With DisabilitiesPublic Information OfficeBelum ada peringkat

- BRT Open HouseDokumen2 halamanBRT Open HousePublic Information OfficeBelum ada peringkat

- Montgomery County, MD FY19 Operating Budget Forum BriefingDokumen26 halamanMontgomery County, MD FY19 Operating Budget Forum BriefingPublic Information OfficeBelum ada peringkat

- White Oak Science Gateway NewsletterDokumen6 halamanWhite Oak Science Gateway NewsletterPublic Information OfficeBelum ada peringkat

- May 17, 2017 Invitation To Maintenance Facilities Ribbon CuttingDokumen1 halamanMay 17, 2017 Invitation To Maintenance Facilities Ribbon CuttingPublic Information OfficeBelum ada peringkat

- 9-2016 Beacon Villages Age FriendlyDokumen2 halaman9-2016 Beacon Villages Age FriendlyPublic Information OfficeBelum ada peringkat

- Executive Initiatives - SMT BriefingDokumen6 halamanExecutive Initiatives - SMT BriefingPublic Information OfficeBelum ada peringkat

- 9-2016 Beacon Villages Age FriendlyDokumen2 halaman9-2016 Beacon Villages Age FriendlyPublic Information OfficeBelum ada peringkat

- Sales Tax PerformaDokumen2 halamanSales Tax PerformaShamas Ur Rehman100% (2)

- Form 16ADokumen4 halamanForm 16AniranjansankaBelum ada peringkat

- SolutionsDokumen22 halamanSolutionsapi-381707267% (3)

- RMC 2020 No. 16 Availability of Oflline eBIR Forms Version 7.6Dokumen2 halamanRMC 2020 No. 16 Availability of Oflline eBIR Forms Version 7.6Bien Bowie A. CortezBelum ada peringkat

- Cir v. Phoenix DigestDokumen3 halamanCir v. Phoenix DigestkathrynmaydevezaBelum ada peringkat

- SPIT. Abella SamplexDokumen5 halamanSPIT. Abella SamplexEins BalagtasBelum ada peringkat

- Commissioner of Internal Revenue V Solidbank CorporationDokumen2 halamanCommissioner of Internal Revenue V Solidbank CorporationMarj CenBelum ada peringkat

- 01TaskPerformance1 BussinessTaxDokumen3 halaman01TaskPerformance1 BussinessTaxSnapShop by AJBelum ada peringkat

- Estates & Trust, Fringe BenefitDokumen3 halamanEstates & Trust, Fringe BenefitYamateBelum ada peringkat

- Sabeel Ahamed SANAM20120007Dokumen1 halamanSabeel Ahamed SANAM20120007Srei noyaBelum ada peringkat

- DR Rohit JainDokumen1 halamanDR Rohit JainlxshBelum ada peringkat

- TRACES TDS July-2019 PDFDokumen1 halamanTRACES TDS July-2019 PDFPrameet ChakrabortyBelum ada peringkat

- GTS Calculation PDFDokumen1 halamanGTS Calculation PDFpablo zarateBelum ada peringkat

- Earnings Deductions: Eicher Motors LimitedDokumen1 halamanEarnings Deductions: Eicher Motors LimitedR SEETHARAMANBelum ada peringkat

- Indigo Denim Work Order SiemensDokumen1 halamanIndigo Denim Work Order SiemensAadya In StyleBelum ada peringkat

- GIRO Instalment Plan For Income Tax: Month Month Amount ($) Amount ($)Dokumen2 halamanGIRO Instalment Plan For Income Tax: Month Month Amount ($) Amount ($)Nelly HBelum ada peringkat

- Gstin: 08cympg9536p1z9 BG01189: Amichand Saini (11885729)Dokumen2 halamanGstin: 08cympg9536p1z9 BG01189: Amichand Saini (11885729)Subhash SainiBelum ada peringkat

- 2316 (1) 2Dokumen2 halaman2316 (1) 2jonbelzaBelum ada peringkat

- Getting Paid MathDokumen3 halamanGetting Paid Mathapi-26818659543% (7)

- Tax Invoice: Gohtldand3W6Z8U7Dokumen2 halamanTax Invoice: Gohtldand3W6Z8U7Arup ChakrabortyBelum ada peringkat

- Inv Ap B1 78160637 104375634240 August 2022Dokumen2 halamanInv Ap B1 78160637 104375634240 August 2022Narasimha RaoBelum ada peringkat

- Epayslip 2023-07-27 31173270Dokumen1 halamanEpayslip 2023-07-27 31173270ryan robert mercadoBelum ada peringkat

- MBB InvoiceDokumen1 halamanMBB InvoiceYuvraj ElangoBelum ada peringkat

- IRS Abatement Letter TemplateDokumen1 halamanIRS Abatement Letter Templategregtalbott100% (1)

- INVOICE: INV44692504 Customer #52693642Dokumen1 halamanINVOICE: INV44692504 Customer #52693642Sandy TessierBelum ada peringkat

- Percentage Tax Return: BIR Form NoDokumen1 halamanPercentage Tax Return: BIR Form NoLorraine Steffany BanguisBelum ada peringkat

- How Does The BIR Conduct Its Audit: By: Ms. Jorhiza Ortelano EstebanDokumen13 halamanHow Does The BIR Conduct Its Audit: By: Ms. Jorhiza Ortelano EstebanRheneir MoraBelum ada peringkat

- Sample ComputationDokumen16 halamanSample ComputationMarkwin QuadxBelum ada peringkat

- CA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Dokumen4 halamanCA Final Vsi Jaipur IDT ABC Analysis For Nov 2023Dharani SsBelum ada peringkat

- Chandra Enterprises-059Dokumen4 halamanChandra Enterprises-059Aarvee FoodBelum ada peringkat