Anda mungkin juga menyukai

- DTL Sec 10Dokumen14 halamanDTL Sec 10Nikhil KasatBelum ada peringkat

- Sale DeedDokumen5 halamanSale DeedNitin GoyalBelum ada peringkat

- Types of Stamps and Some Concepts of Stamp DutyDokumen5 halamanTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

- Derivatives Markets in Interest Rate & Foreign Exchange RateDokumen20 halamanDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfBelum ada peringkat

- Income Declaration Scheme Rules, 2016: Form 1Dokumen9 halamanIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatBelum ada peringkat

- Hedging With Financial DerivativesDokumen30 halamanHedging With Financial DerivativesNikhil KasatBelum ada peringkat

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Dokumen21 halamanSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatBelum ada peringkat

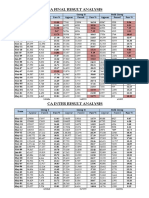

- CA Result AnalysisDokumen1 halamanCA Result AnalysisNikhil KasatBelum ada peringkat

- BLack Money RulesDokumen23 halamanBLack Money RulesLive LawBelum ada peringkat

- Banca SuranceDokumen32 halamanBanca SuranceNikhil KasatBelum ada peringkat

- August Month CompliancesDokumen1 halamanAugust Month CompliancesNikhil KasatBelum ada peringkat

- Black Money BillDokumen30 halamanBlack Money BillNikhil KasatBelum ada peringkat

- Delhi Dvat Registration InformationDokumen4 halamanDelhi Dvat Registration InformationNikhil KasatBelum ada peringkat

- Valuation of InventoriesDokumen4 halamanValuation of InventoriesNikhil KasatBelum ada peringkat

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDokumen10 halamanFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatBelum ada peringkat

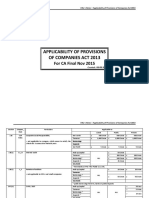

- ApplicabiliTY of ProvisionsDokumen3 halamanApplicabiliTY of ProvisionsNikhil KasatBelum ada peringkat

- Directors Report As Per StatusDokumen5 halamanDirectors Report As Per StatusNikhil KasatBelum ada peringkat

- List of Indian As Convergence With IfrsDokumen1 halamanList of Indian As Convergence With IfrsNikhil KasatBelum ada peringkat

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDokumen9 halamanAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatBelum ada peringkat

- Anf 4dDokumen3 halamanAnf 4dNikhil KasatBelum ada peringkat

- Tds On SalariesDokumen55 halamanTds On SalariespunitBelum ada peringkat

- Curriculum VitaeDokumen13 halamanCurriculum VitaeNikhil KasatBelum ada peringkat

- CA Final Writing Professional Ethics AnswersDokumen2 halamanCA Final Writing Professional Ethics AnswersNikhil KasatBelum ada peringkat

- Web Base Timesheet ApplicationDokumen4 halamanWeb Base Timesheet ApplicationNikhil KasatBelum ada peringkat

- Importance of ArticleshipDokumen6 halamanImportance of ArticleshipNikhil KasatBelum ada peringkat

- Privileges To Small CompaniesDokumen2 halamanPrivileges To Small CompaniesNikhil KasatBelum ada peringkat

- C01Dokumen23 halamanC01Silvery DoeBelum ada peringkat

- Ind As 2015Dokumen2 halamanInd As 2015Nikhil KasatBelum ada peringkat

- Cusoms Valuation MaterialDokumen8 halamanCusoms Valuation MaterialNikhil KasatBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (120)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- ch4 PDFDokumen43 halamanch4 PDFAliaa HosamBelum ada peringkat

- UNIT:10 Accounts For Incomplete RecordsDokumen7 halamanUNIT:10 Accounts For Incomplete RecordsPramod VasudevBelum ada peringkat

- Transaksi Jurnal PT AlfamartDokumen1 halamanTransaksi Jurnal PT AlfamartSefriati MagdaBelum ada peringkat

- Origin and Evolution of AuditingDokumen3 halamanOrigin and Evolution of AuditingAntony SanthiyaBelum ada peringkat

- 02-IAS 12 Income TaxesDokumen42 halaman02-IAS 12 Income TaxesHaseeb Ullah KhanBelum ada peringkat

- What Is An Extended TrialDokumen19 halamanWhat Is An Extended TrialocalmaviliBelum ada peringkat

- Internal Audit Manual NewDokumen26 halamanInternal Audit Manual NewhtakrouriBelum ada peringkat

- P3 - Performance StrategyDokumen17 halamanP3 - Performance StrategyWaqas BadshahBelum ada peringkat

- English For The Financial Sector Intermediate Teachers Book FrontmatterDokumen10 halamanEnglish For The Financial Sector Intermediate Teachers Book FrontmatterPS Lee0% (3)

- Long Test BFDokumen2 halamanLong Test BFApril De HittaBelum ada peringkat

- Accounting Theory Conceptual Issues in A Political and Economic Environment 8th Edition Wolk Solutions ManualDokumen36 halamanAccounting Theory Conceptual Issues in A Political and Economic Environment 8th Edition Wolk Solutions Manualgauntreprovalaxdjx100% (25)

- Accounting ChangesDokumen5 halamanAccounting ChangesShielle AzonBelum ada peringkat

- Riyadh Final PB Far 2019Dokumen17 halamanRiyadh Final PB Far 2019jhaizonBelum ada peringkat

- Solutions To Exercises - Chap 3Dokumen27 halamanSolutions To Exercises - Chap 3InciaBelum ada peringkat

- SOP For Fixed Assets Management PPTX JN9OBYJQ PDF Corporations Accounting 18Dokumen1 halamanSOP For Fixed Assets Management PPTX JN9OBYJQ PDF Corporations Accounting 18Mohammad ZamanBelum ada peringkat

- Books of Accounts & Accounting RecordsDokumen34 halamanBooks of Accounts & Accounting RecordsCA Deepak Ehn67% (3)

- Wk14 Summary Quizzer 2 - Set BDokumen5 halamanWk14 Summary Quizzer 2 - Set Bmariesteinsher0Belum ada peringkat

- RMK Akl Kelompok 5Dokumen25 halamanRMK Akl Kelompok 5rico zachariBelum ada peringkat

- Hira Arshad: ObjectiveDokumen2 halamanHira Arshad: ObjectiveNabeel MaqsoodBelum ada peringkat

- Accounting 141 2020Dokumen7 halamanAccounting 141 2020alexcharles433Belum ada peringkat

- Module 4 Completion The Accounting CycleDokumen27 halamanModule 4 Completion The Accounting CycleJane Russel SolatorioBelum ada peringkat

- Cost Accounting Class XI PDFDokumen173 halamanCost Accounting Class XI PDFKaushal guptaBelum ada peringkat

- PARTNERSHIP2Dokumen13 halamanPARTNERSHIP2Anne Marielle UyBelum ada peringkat

- Solution Manual For College Accounting 14th Edition Price, Haddock, FarinaDokumen18 halamanSolution Manual For College Accounting 14th Edition Price, Haddock, Farinaa289899847Belum ada peringkat

- PSA 100 Phil Framework For Assurance EngagementsDokumen4 halamanPSA 100 Phil Framework For Assurance EngagementsSkye LeeBelum ada peringkat

- Introduction To Adjusting EntriesDokumen1 halamanIntroduction To Adjusting EntriesAnj HwanBelum ada peringkat

- Job Order Costing Syste1 PDFDokumen19 halamanJob Order Costing Syste1 PDFgosaye desalegn100% (2)

- Earning Quality ICDokumen6 halamanEarning Quality ICnovitaanggrainiBelum ada peringkat

- Ichapter 6-The Expenditure Cycle Part Ii: Payroll Processing and Fixed Asset ProceduresDokumen14 halamanIchapter 6-The Expenditure Cycle Part Ii: Payroll Processing and Fixed Asset ProceduresJessalyn DaneBelum ada peringkat

- Glimpse of Accounting Standards Group 1Dokumen52 halamanGlimpse of Accounting Standards Group 1Rajesh Mahesh BohraBelum ada peringkat