Anda mungkin juga menyukai

- Earnings Statement: Non-NegotiableDokumen1 halamanEarnings Statement: Non-Negotiablesivajyothi1973Belum ada peringkat

- Cook County Executive Budget Recommendation FY 2018Dokumen432 halamanCook County Executive Budget Recommendation FY 2018CrainsChicagoBusiness100% (1)

- T08 - Government Accounting PDFDokumen9 halamanT08 - Government Accounting PDFAken Lieram Ats AnaBelum ada peringkat

- A Handbook For Tax SimplificationDokumen258 halamanA Handbook For Tax SimplificationROWLAND PASARIBU100% (1)

- Community College Finance: A Guide for Institutional LeadersDari EverandCommunity College Finance: A Guide for Institutional LeadersBelum ada peringkat

- Budget MessageDokumen2 halamanBudget MessageGina Gobaton Arquillo100% (4)

- Accounting for Budgetary AccountsDokumen11 halamanAccounting for Budgetary AccountsFred Michael L. Go100% (1)

- Tax GoshwaraDokumen2 halamanTax GoshwaraasfandjanBelum ada peringkat

- Inherent Limitations of TaxationDokumen1 halamanInherent Limitations of TaxationVicson Mabanglo100% (2)

- Briefing Note: "2011 - 2014 Budget and Taxpayer Savings"Dokumen6 halamanBriefing Note: "2011 - 2014 Budget and Taxpayer Savings"Jonathan Goldsbie100% (1)

- Metro General Survey Results PresentationDokumen29 halamanMetro General Survey Results PresentationMetro Los AngelesBelum ada peringkat

- D25News 07 AugSept2010Dokumen4 halamanD25News 07 AugSept2010Della Au BelattiBelum ada peringkat

- 2010 Charleston BLVD Rod Run Doo Wop - Event AnalysisDokumen16 halaman2010 Charleston BLVD Rod Run Doo Wop - Event AnalysisDuane B ThomasBelum ada peringkat

- Blade 02-06-14 01Dokumen1 halamanBlade 02-06-14 01bladepublishingBelum ada peringkat

- Metro Public Poll ResultsDokumen46 halamanMetro Public Poll ResultsMetro Los AngelesBelum ada peringkat

- Report On Poverty SurveyDokumen17 halamanReport On Poverty SurveyGuneet SinghBelum ada peringkat

- 2014 Retail Rates and Market Demographic Summary: AddressDokumen20 halaman2014 Retail Rates and Market Demographic Summary: AddressMichael DanielsBelum ada peringkat

- 2016 Finance Survey Report FINALDokumen24 halaman2016 Finance Survey Report FINALrkarlinBelum ada peringkat

- The Star News January 15 2015Dokumen31 halamanThe Star News January 15 2015The Star NewsBelum ada peringkat

- District 5 Summer Newsletter Supervisor Keith Carson: Release Date: August 3, 2010Dokumen6 halamanDistrict 5 Summer Newsletter Supervisor Keith Carson: Release Date: August 3, 2010localonBelum ada peringkat

- Using Geospatial Mapping To Build City Success: Creating Support, Setting Priorities, Marking ProgressDokumen93 halamanUsing Geospatial Mapping To Build City Success: Creating Support, Setting Priorities, Marking Progressceosforcities_docsBelum ada peringkat

- MN 2013 ScorecardDokumen15 halamanMN 2013 ScorecardAfp HqBelum ada peringkat

- Fargo Refugee PollDokumen5 halamanFargo Refugee PollRob PortBelum ada peringkat

- 1 News Kantar Public Poll - MayDokumen9 halaman1 News Kantar Public Poll - May1NewsBelum ada peringkat

- 1news Kantar Public Poll Report March 2023Dokumen12 halaman1news Kantar Public Poll Report March 20231NewsBelum ada peringkat

- December 9, 2015 Tribune Record GleanerDokumen24 halamanDecember 9, 2015 Tribune Record GleanercwmediaBelum ada peringkat

- 17 2 BondPresentation012516 0Dokumen8 halaman17 2 BondPresentation012516 0Burlingame_DataBelum ada peringkat

- Telephone Survey ReportDokumen58 halamanTelephone Survey ReportJeff RobinsonBelum ada peringkat

- 2017 Western States Survey: Interview ScheduleDokumen26 halaman2017 Western States Survey: Interview ScheduleBenjamin SpillmanBelum ada peringkat

- May 2014 Rev-E NewsDokumen4 halamanMay 2014 Rev-E NewsRob PortBelum ada peringkat

- AALA: Unequal PainDokumen8 halamanAALA: Unequal Painsmf 4LAKidsBelum ada peringkat

- MEC-Mason Dixon Poll On MS Taxes and RoadsDokumen4 halamanMEC-Mason Dixon Poll On MS Taxes and RoadsSam HallBelum ada peringkat

- Daugaard Preprimary ReportDokumen13 halamanDaugaard Preprimary ReportPat PowersBelum ada peringkat

- John HamercheckDokumen2 halamanJohn HamercheckThe News-HeraldBelum ada peringkat

- Nicholas A. Micozzie: State RepresentativeDokumen4 halamanNicholas A. Micozzie: State RepresentativePAHouseGOPBelum ada peringkat

- K-12 Referenda Passage Rates FallDokumen4 halamanK-12 Referenda Passage Rates FallAly ProutyBelum ada peringkat

- April Revenue ReportDokumen3 halamanApril Revenue ReportRob PortBelum ada peringkat

- The Macroeconomics of FundraisingDokumen13 halamanThe Macroeconomics of FundraisingxornophobeBelum ada peringkat

- Budget Vote Delayed: Browsing BackDokumen16 halamanBudget Vote Delayed: Browsing BackelauwitBelum ada peringkat

- Every Child, by Name and Face, To Graduation: Popular Annual Financial ReportDokumen17 halamanEvery Child, by Name and Face, To Graduation: Popular Annual Financial ReportKaleb RoedelBelum ada peringkat

- Dear Constituents,: Save The Date!Dokumen6 halamanDear Constituents,: Save The Date!Representative Debbie PhillipsBelum ada peringkat

- Relationship Between Public Opinion and Public Policy On Public SchoolsDokumen9 halamanRelationship Between Public Opinion and Public Policy On Public Schoolscmarin92Belum ada peringkat

- WSCUHSD Unification StudyDokumen56 halamanWSCUHSD Unification StudyKaylee100% (1)

- Four Year SchoolsDokumen8 halamanFour Year SchoolsJustine AshleyBelum ada peringkat

- May 2013 Project Connect Report-FinalDokumen17 halamanMay 2013 Project Connect Report-Finalapi-218293468Belum ada peringkat

- Brendan Walsh - Financial Benchmark Report - 2013Dokumen12 halamanBrendan Walsh - Financial Benchmark Report - 2013Brendan WalshBelum ada peringkat

- A Discussion About Alaska's FutureDokumen32 halamanA Discussion About Alaska's FutureJeffrey RivetBelum ada peringkat

- Riverside County Legislative PlatformDokumen57 halamanRiverside County Legislative PlatformThe Press-Enterprise / pressenterprise.comBelum ada peringkat

- Ramos July ENL 2017Dokumen1 halamanRamos July ENL 2017HouseDemCommBelum ada peringkat

- VB 10 Year PlanDokumen96 halamanVB 10 Year PlansmcaagencyBelum ada peringkat

- United Way 2-1-1 Annual Report FY 2012Dokumen4 halamanUnited Way 2-1-1 Annual Report FY 2012United Way of East Central IowaBelum ada peringkat

- Americans For Prosperity FY 2017 Taxpayers' BudgetDokumen112 halamanAmericans For Prosperity FY 2017 Taxpayers' BudgetAFPHQ_NewJerseyBelum ada peringkat

- Annual Financial Report Sequatchie County, TennesseeDokumen158 halamanAnnual Financial Report Sequatchie County, TennesseeNewsDunlapBelum ada peringkat

- EKOS Poll, June 17Dokumen5 halamanEKOS Poll, June 17TheGlobeandMailBelum ada peringkat

- Fy 2014 Mayors Budget WebsiteDokumen437 halamanFy 2014 Mayors Budget WebsiteHelen BennettBelum ada peringkat

- Bill Could Change School Elections: Classroom LectureDokumen16 halamanBill Could Change School Elections: Classroom LectureelauwitBelum ada peringkat

- Year Three Survey 050212Dokumen28 halamanYear Three Survey 050212smf 4LAKidsBelum ada peringkat

- Access ControllerDokumen16 halamanAccess Controllerjstocks747Belum ada peringkat

- Solution 1Dokumen7 halamanSolution 1api-253385147Belum ada peringkat

- Glad Win Ballot Proofs 91912Dokumen48 halamanGlad Win Ballot Proofs 91912tfaber2933Belum ada peringkat

- The Few Decide - ReportDokumen12 halamanThe Few Decide - ReportRobert GarciaBelum ada peringkat

- Highlights of The North Carolina Public School Budget 2013Dokumen41 halamanHighlights of The North Carolina Public School Budget 2013Nathaniel MaconBelum ada peringkat

- 20120524133045612Dokumen119 halaman20120524133045612WisconsinOpenRecordsBelum ada peringkat

- Country Courier - 09/06/2013 - Page 01Dokumen1 halamanCountry Courier - 09/06/2013 - Page 01bladepublishingBelum ada peringkat

- EKOS Poll - April 15, 2010Dokumen5 halamanEKOS Poll - April 15, 2010The Globe and MailBelum ada peringkat

- $56B Budget Heads To Kasich's Desk: Elphos EraldDokumen10 halaman$56B Budget Heads To Kasich's Desk: Elphos EraldThe Delphos HeraldBelum ada peringkat

- More Economic Growth Region 5 Labor Market InformationDokumen6 halamanMore Economic Growth Region 5 Labor Market InformationHilary TerryBelum ada peringkat

- The Financial Death Spiral of the United States Postal Service ...Unless?Dari EverandThe Financial Death Spiral of the United States Postal Service ...Unless?Belum ada peringkat

- 2017 08 18 Constitution OrderDokumen27 halaman2017 08 18 Constitution OrderjspectorBelum ada peringkat

- Joseph Ruggiero Employment AgreementDokumen6 halamanJoseph Ruggiero Employment AgreementjspectorBelum ada peringkat

- IG LetterDokumen3 halamanIG Letterjspector100% (1)

- Cornell ComplaintDokumen41 halamanCornell Complaintjspector100% (1)

- Pennies For Charity 2018Dokumen12 halamanPennies For Charity 2018ZacharyEJWilliamsBelum ada peringkat

- NYSCrimeReport2016 PrelimDokumen14 halamanNYSCrimeReport2016 PrelimjspectorBelum ada peringkat

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDokumen8 halamanFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorBelum ada peringkat

- Federal Budget Fiscal Year 2017 Web VersionDokumen36 halamanFederal Budget Fiscal Year 2017 Web VersionjspectorBelum ada peringkat

- State Health CoverageDokumen26 halamanState Health CoveragejspectorBelum ada peringkat

- Hiffa Settlement Agreement ExecutedDokumen5 halamanHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Inflation AllowablegrowthfactorsDokumen1 halamanInflation AllowablegrowthfactorsjspectorBelum ada peringkat

- Abo 2017 Annual ReportDokumen65 halamanAbo 2017 Annual ReportrkarlinBelum ada peringkat

- SNY0517 Crosstabs 052417Dokumen4 halamanSNY0517 Crosstabs 052417Nick ReismanBelum ada peringkat

- Teacher Shortage Report 05232017 PDFDokumen16 halamanTeacher Shortage Report 05232017 PDFjspectorBelum ada peringkat

- Class of 2022Dokumen1 halamanClass of 2022jspectorBelum ada peringkat

- Opiods 2017-04-20-By Numbers Brief No8Dokumen17 halamanOpiods 2017-04-20-By Numbers Brief No8rkarlinBelum ada peringkat

- Siena Poll March 27, 2017Dokumen7 halamanSiena Poll March 27, 2017jspectorBelum ada peringkat

- p12 Budget Testimony 2-14-17Dokumen31 halamanp12 Budget Testimony 2-14-17jspectorBelum ada peringkat

- Youth Cigarette and E-Cigs UseDokumen1 halamanYouth Cigarette and E-Cigs UsejspectorBelum ada peringkat

- Oag Sed Letter Ice 2-27-17Dokumen3 halamanOag Sed Letter Ice 2-27-17BethanyBelum ada peringkat

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDokumen55 halaman16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorBelum ada peringkat

- 2017 School Bfast Report Online Version 3-7-17 0Dokumen29 halaman2017 School Bfast Report Online Version 3-7-17 0jspectorBelum ada peringkat

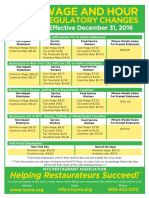

- Wage and Hour Regulatory Changes 2016Dokumen2 halamanWage and Hour Regulatory Changes 2016jspectorBelum ada peringkat

- Schneiderman Voter Fraud Letter 022217Dokumen2 halamanSchneiderman Voter Fraud Letter 022217Matthew HamiltonBelum ada peringkat

- Darweesh Cities AmicusDokumen32 halamanDarweesh Cities AmicusjspectorBelum ada peringkat

- Review of Executive Budget 2017Dokumen102 halamanReview of Executive Budget 2017Nick ReismanBelum ada peringkat

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Dokumen4 halamanActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorBelum ada peringkat

- 2016 Local Sales Tax CollectionsDokumen4 halaman2016 Local Sales Tax CollectionsjspectorBelum ada peringkat

- Pub Auth Num 2017Dokumen54 halamanPub Auth Num 2017jspectorBelum ada peringkat

- Voting Report CardDokumen1 halamanVoting Report CardjspectorBelum ada peringkat

- Sri Lanka State of The Economy 2015: Economic PerformanceDokumen3 halamanSri Lanka State of The Economy 2015: Economic PerformanceIPS Sri LankaBelum ada peringkat

- Expansionary & Contractionary Fiscal PolicyDokumen4 halamanExpansionary & Contractionary Fiscal PolicyShwetabh SrivastavaBelum ada peringkat

- Pateros Municipal Ordinances 1988-1990Dokumen59 halamanPateros Municipal Ordinances 1988-1990Suzette FloranzaBelum ada peringkat

- Viewing On Burma Wiki LeaksDokumen9 halamanViewing On Burma Wiki LeaksBurma Democratic Concern (BDC)Belum ada peringkat

- Economic Causes of The French Revolution: DebtDokumen3 halamanEconomic Causes of The French Revolution: Debtboorishyesterda21100% (1)

- Budgeting and Budgetary Control As Tools For Accountability in Government ParastatalsDokumen5 halamanBudgeting and Budgetary Control As Tools For Accountability in Government ParastatalsDineshBelum ada peringkat

- It 000037777275 2014 00Dokumen2 halamanIt 000037777275 2014 00Muneer AfridiBelum ada peringkat

- Icb0047: Public FinanceDokumen3 halamanIcb0047: Public FinancetitimaBelum ada peringkat

- Randall Wray's MMT Presentation For Modern Money and Public PurposeDokumen28 halamanRandall Wray's MMT Presentation For Modern Money and Public Purposedevindsmith80% (5)

- US Internal Revenue Service: f1041t - 1994Dokumen2 halamanUS Internal Revenue Service: f1041t - 1994IRSBelum ada peringkat

- Fiscal PolicyDokumen21 halamanFiscal PolicyAdityaBelum ada peringkat

- CMS ReportDokumen9 halamanCMS ReportRecordTrac - City of OaklandBelum ada peringkat

- Bla18632 ch09Dokumen34 halamanBla18632 ch09jackBelum ada peringkat

- 2011 EUA Crise Teto Da DívidaDokumen12 halaman2011 EUA Crise Teto Da DívidaGabriel LaguerraBelum ada peringkat

- Chuck Hillier Candidate QuestionnaireDokumen3 halamanChuck Hillier Candidate QuestionnaireDevon UrchinBelum ada peringkat

- Ejlr 2009-4 511-530Dokumen20 halamanEjlr 2009-4 511-530E Drejta BEBelum ada peringkat

- 2013 ABFM Conference Agenda BookDokumen48 halaman2013 ABFM Conference Agenda BookKenneth HunterBelum ada peringkat

- Government Accounting Written ReportDokumen14 halamanGovernment Accounting Written ReportMary Joy DomantayBelum ada peringkat

- The First State Finance Commission Report, (1996), KeralaDokumen288 halamanThe First State Finance Commission Report, (1996), KeralaK Rajasekharan100% (3)

- Peggy M. Venable Testimony Texas Public Education EfficiencyDokumen20 halamanPeggy M. Venable Testimony Texas Public Education EfficiencyeduefficiencyBelum ada peringkat