Anda mungkin juga menyukai

- Task 1 AnswerDokumen9 halamanTask 1 AnswerSiddhant Aggarwal0% (4)

- NBA Happy Hour Co - DCF Model v2Dokumen10 halamanNBA Happy Hour Co - DCF Model v2Siddhant Aggarwal50% (2)

- Task 3 - DCF ModelDokumen10 halamanTask 3 - DCF Modeldavin nathanBelum ada peringkat

- Engineering and Commercial Functions in BusinessDari EverandEngineering and Commercial Functions in BusinessPenilaian: 5 dari 5 bintang5/5 (1)

- Fundamentals of Fund Administration: A GuideDari EverandFundamentals of Fund Administration: A GuidePenilaian: 5 dari 5 bintang5/5 (1)

- MT103 Zheshang 100BDokumen3 halamanMT103 Zheshang 100Brasool mehrjooBelum ada peringkat

- X82 - Threads LTD v01Dokumen4 halamanX82 - Threads LTD v01Udaya Makineni33% (3)

- Case Study No. 3 PDFDokumen6 halamanCase Study No. 3 PDFMuhammadZahirGulBelum ada peringkat

- Black Book Project of Kotak Mahindra Bank PDFDokumen14 halamanBlack Book Project of Kotak Mahindra Bank PDFShinu Jain0% (2)

- AccDokumen4 halamanAccrenoBelum ada peringkat

- Problems: Set B: InstructionsDokumen4 halamanProblems: Set B: InstructionsflrnciairnBelum ada peringkat

- Marriott Corp BDokumen15 halamanMarriott Corp BEshesh GuptaBelum ada peringkat

- Case 1 MarriottDokumen14 halamanCase 1 Marriotthimanshu sagar100% (1)

- Working Capital Analysis Of: Supraneet AryaDokumen21 halamanWorking Capital Analysis Of: Supraneet Aryadeepak_chamaylBelum ada peringkat

- Working Capital Analysis Of: Supraneet AryaDokumen20 halamanWorking Capital Analysis Of: Supraneet AryaSupraneet AryaBelum ada peringkat

- Glaxosmithkline Consumer Healthcare: Group MembersDokumen19 halamanGlaxosmithkline Consumer Healthcare: Group MembersBilal AfzalBelum ada peringkat

- NBA Happy Hour Co - DCF Model - Task 4 - Revised TemplateDokumen10 halamanNBA Happy Hour Co - DCF Model - Task 4 - Revised Templateww weBelum ada peringkat

- Mini Case Chapter 3 Final VersionDokumen14 halamanMini Case Chapter 3 Final VersionAlberto MariñoBelum ada peringkat

- Nba Advanced - Happy Hour Co - DCF Model v2Dokumen10 halamanNba Advanced - Happy Hour Co - DCF Model v221BAM045 Sandhiya SBelum ada peringkat

- Genting Malaysia Berhad 110220Dokumen51 halamanGenting Malaysia Berhad 110220BT GOHBelum ada peringkat

- Financial Ratio Analysis of PSO and SPL (Shell) ........ TAHIR SAMIDokumen35 halamanFinancial Ratio Analysis of PSO and SPL (Shell) ........ TAHIR SAMISAM100% (1)

- SFH Rental AnalysisDokumen6 halamanSFH Rental AnalysisA jBelum ada peringkat

- CRDB Bank Annual Report-2009Dokumen138 halamanCRDB Bank Annual Report-2009John SekaBelum ada peringkat

- Management of Monetary Resource of GSK: Course: Faculty: Group NameDokumen27 halamanManagement of Monetary Resource of GSK: Course: Faculty: Group Nameborn2growBelum ada peringkat

- A Global Organisation: An Analysis of Marriott InternationalDokumen22 halamanA Global Organisation: An Analysis of Marriott InternationalTulshi NaikBelum ada peringkat

- Question 1: Overall WACCDokumen15 halamanQuestion 1: Overall WACCSaadatBelum ada peringkat

- Working Capital ManagementDokumen19 halamanWorking Capital ManagementSandeep KumarBelum ada peringkat

- "Financial Statement Analysis Using Uk Gaap PrinciplDokumen14 halaman"Financial Statement Analysis Using Uk Gaap Principlrayjit2003Belum ada peringkat

- Business ValuationDokumen2 halamanBusiness Valuationahmed HOSNYBelum ada peringkat

- The Discounted Free Cash Flow Model For A Complete BusinessDokumen2 halamanThe Discounted Free Cash Flow Model For A Complete BusinessBacarrat BBelum ada peringkat

- The Discounted Free Cash Flow Model For A Complete BusinessDokumen2 halamanThe Discounted Free Cash Flow Model For A Complete BusinessHẬU ĐỖ NGỌCBelum ada peringkat

- Axis Bank Analyst 08 09Dokumen34 halamanAxis Bank Analyst 08 09goyalabhiBelum ada peringkat

- SVA ModelDokumen15 halamanSVA ModelArshdeep SaroyaBelum ada peringkat

- A Summer Internship Project PresentationDokumen17 halamanA Summer Internship Project Presentationkaushalsharma2488Belum ada peringkat

- Building: Annual 2 0 2 1 / 2 2Dokumen128 halamanBuilding: Annual 2 0 2 1 / 2 2TharushikaBelum ada peringkat

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADokumen6 halamanParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemBelum ada peringkat

- Integrative Case Track Software LTDDokumen19 halamanIntegrative Case Track Software LTDDang DangBelum ada peringkat

- M.Sc. Microbiology Bio TechnologyDokumen6 halamanM.Sc. Microbiology Bio Technologymmumullana0098Belum ada peringkat

- Economic Analysis: Company Name Suscok Jaya GemilangDokumen1 halamanEconomic Analysis: Company Name Suscok Jaya GemilangSamuel ArelianoBelum ada peringkat

- Sag Annual Report 2016 e Data PDFDokumen184 halamanSag Annual Report 2016 e Data PDFÁkos SlezákBelum ada peringkat

- Rdy Mad e Pmegp 5lacsDokumen12 halamanRdy Mad e Pmegp 5lacssyedBelum ada peringkat

- Book 1Dokumen10 halamanBook 1Sakhwat Hossen 2115202660Belum ada peringkat

- Project Work On Financial Management: Prepared By:-Siddharth S. KothariDokumen22 halamanProject Work On Financial Management: Prepared By:-Siddharth S. Kotharisunilsims2Belum ada peringkat

- EPL LTD Financial Statements - XDokumen16 halamanEPL LTD Financial Statements - XAakashBelum ada peringkat

- Pakistan State Oil Company Limited (Pso)Dokumen6 halamanPakistan State Oil Company Limited (Pso)Maaz HanifBelum ada peringkat

- Invest Analysis TablesDokumen2 halamanInvest Analysis TablesNiña PacoBelum ada peringkat

- Radasham Chandra Sarkar (038) JONY RAJ (098) Minhaz ArafatDokumen37 halamanRadasham Chandra Sarkar (038) JONY RAJ (098) Minhaz Arafatitsp.solution104Belum ada peringkat

- SPS Sample ReportsDokumen61 halamanSPS Sample Reportsphong.parkerdistributorBelum ada peringkat

- Arun 1Dokumen2 halamanArun 1Nishanth RioBelum ada peringkat

- Namrata Gadkari Ceres IMTDokumen6 halamanNamrata Gadkari Ceres IMTnamratagadkari05Belum ada peringkat

- Novartis Astrazeneca Novartis Astrazeneca Novartis AstrazenecaDokumen8 halamanNovartis Astrazeneca Novartis Astrazeneca Novartis AstrazenecaHashim ShahzadBelum ada peringkat

- Company Info - Print FinancialsDokumen2 halamanCompany Info - Print FinancialsKavitha prabhakaranBelum ada peringkat

- Pescadero MRSDokumen20 halamanPescadero MRStomconne100% (2)

- Markaz-GL On Financial ProjectionsDokumen10 halamanMarkaz-GL On Financial ProjectionsSrikanth P School of Business and ManagementBelum ada peringkat

- CIEN Is A Turnaround StockDokumen8 halamanCIEN Is A Turnaround StockShanti PutriBelum ada peringkat

- 3.2 FCFE Exercise PartDokumen4 halaman3.2 FCFE Exercise PartHTBelum ada peringkat

- Murree Brewery: Beverage IndustryDokumen12 halamanMurree Brewery: Beverage Industrykinza bashirBelum ada peringkat

- YubarajDokumen4 halamanYubarajYubraj ThapaBelum ada peringkat

- Jawaban KOMPUTASI MDA PT SEMEN INDONESIADokumen4 halamanJawaban KOMPUTASI MDA PT SEMEN INDONESIAAyu TriBelum ada peringkat

- Computing The Value of A Growing Finite AnnuityDokumen10 halamanComputing The Value of A Growing Finite AnnuityMahmood AhmadBelum ada peringkat

- Ratio Analysis: Investor Liquidity RatiosDokumen11 halamanRatio Analysis: Investor Liquidity RatiosjayRBelum ada peringkat

- Inputs For Valuation Current InputsDokumen6 halamanInputs For Valuation Current Inputsapi-3763138Belum ada peringkat

- RDInstallmentReport12 01 2024Dokumen4 halamanRDInstallmentReport12 01 2024Khushal TembhekarBelum ada peringkat

- Macroeconomics: Money Supply and Money DemandDokumen7 halamanMacroeconomics: Money Supply and Money DemandSharhie RahmaBelum ada peringkat

- Characteristics of Floating ChargeDokumen4 halamanCharacteristics of Floating ChargeNg GraceBelum ada peringkat

- Banks and Information Technology Complexity FlexibDokumen29 halamanBanks and Information Technology Complexity FlexibJennifer WijayaBelum ada peringkat

- MMW Activity 24Dokumen1 halamanMMW Activity 24Ronaldo R. VillanuevaBelum ada peringkat

- System Enabled Emp DetailsDokumen6 halamanSystem Enabled Emp DetailsAshish PorechaBelum ada peringkat

- Macroeconomics Study GuideDokumen8 halamanMacroeconomics Study GuideAustin WellsBelum ada peringkat

- Screenshot 2023-05-10 at 3.27.24 PMDokumen1 halamanScreenshot 2023-05-10 at 3.27.24 PMvathanirajBelum ada peringkat

- Test Doc 3Dokumen14 halamanTest Doc 3ChaBelum ada peringkat

- BankDokumen4 halamanBankkimba worthBelum ada peringkat

- Bank Services AssignmentDokumen4 halamanBank Services AssignmentERICK MLINGWABelum ada peringkat

- Financial Performance of Kist BankDokumen14 halamanFinancial Performance of Kist BankDeepesh SharmaBelum ada peringkat

- Capital Adequacy Ratios AnalysisDokumen4 halamanCapital Adequacy Ratios AnalysisAsma RajaBelum ada peringkat

- OpTransactionHistory16 06 2018Dokumen1 halamanOpTransactionHistory16 06 2018Shivam BhadouriaBelum ada peringkat

- TSN Information Description Information Source (Filer Name)Dokumen2 halamanTSN Information Description Information Source (Filer Name)C.A. Ankit JainBelum ada peringkat

- Kotak Mahindra Bank - WikipediaDokumen35 halamanKotak Mahindra Bank - WikipediaPriya v Priya vBelum ada peringkat

- Chapter 1 Introduction To Money and BankingDokumen65 halamanChapter 1 Introduction To Money and BankingLâm BullsBelum ada peringkat

- List of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameDokumen102 halamanList of Non-Scheduled Urban Co-Operative Banks Sr. No. Bank Name RO NameSusanBelum ada peringkat

- S2 2023 484916 BibliographyDokumen4 halamanS2 2023 484916 BibliographysalsabilaluvaridianBelum ada peringkat

- Black Book ProjectDokumen59 halamanBlack Book ProjectShruthik GuttulaBelum ada peringkat

- Bonnie Lundbohm - 2025Dokumen5 halamanBonnie Lundbohm - 2025Peter MariluchBelum ada peringkat

- REportDokumen20 halamanREportPrashant MahawarBelum ada peringkat

- Change of Bank Details - Declaration Form: D M M Y Y DDokumen1 halamanChange of Bank Details - Declaration Form: D M M Y Y DSophia ShafiBelum ada peringkat

- MSB ATM GuidanceDokumen3 halamanMSB ATM GuidanceJay CaplanBelum ada peringkat

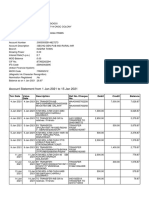

- Account Statement From 1 Jan 2021 To 15 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen2 halamanAccount Statement From 1 Jan 2021 To 15 Jan 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceabhijit gogoiBelum ada peringkat

- Chapter 4Dokumen39 halamanChapter 4Pratikshya KarkiBelum ada peringkat