Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (120)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Dr. M.D. Chase Long Beach State University Advanced Accounting 525-46B Intercompany Leases-Illustrative Examples Page 1Dokumen8 halamanDr. M.D. Chase Long Beach State University Advanced Accounting 525-46B Intercompany Leases-Illustrative Examples Page 1Zenni T XinBelum ada peringkat

- Direct TaxationDokumen39 halamanDirect TaxationSethu SangurajanBelum ada peringkat

- Valuation of Cold Storage Plant R Jayaraman F.I.V.: Registered Valuer (TN)Dokumen25 halamanValuation of Cold Storage Plant R Jayaraman F.I.V.: Registered Valuer (TN)Venkat Deepak SarmaBelum ada peringkat

- Domestic Pressure Cookers Market AnalysisDokumen9 halamanDomestic Pressure Cookers Market AnalysisAnkit AgrawalBelum ada peringkat

- Sem - 3 Advanced Corporate Accounting - 1 MCQ Accounting Standards (As) /lease AccountingDokumen11 halamanSem - 3 Advanced Corporate Accounting - 1 MCQ Accounting Standards (As) /lease Accountinglol0% (1)

- 55910bosintermay20 p3 cp12Dokumen50 halaman55910bosintermay20 p3 cp12Anand PandeyBelum ada peringkat

- 704Dokumen8 halaman704Bhoomi GhariwalaBelum ada peringkat

- Iubat - International University of Business Agriculture and TechnologyDokumen35 halamanIubat - International University of Business Agriculture and TechnologyMohammad Jubayer Ahmed100% (3)

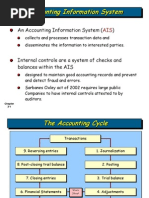

- Wiley - Chapter 3: The Accounting Information SystemDokumen36 halamanWiley - Chapter 3: The Accounting Information SystemIvan BliminseBelum ada peringkat

- Mumbai Kamgar M.G.S.S.Maryadit CKS: Apna Bazar Co-Op Department Store (Mulund)Dokumen21 halamanMumbai Kamgar M.G.S.S.Maryadit CKS: Apna Bazar Co-Op Department Store (Mulund)Gaurav SavlaniBelum ada peringkat

- FIN202 Test BankDokumen294 halamanFIN202 Test BankNguyen Le Khanh Thy (K17 DN)Belum ada peringkat

- Checklist For Various Heads of Audit Working Paper FileDokumen54 halamanChecklist For Various Heads of Audit Working Paper Filesialkotia92% (25)

- ICAEW 2021 Chapter 15: Sole Trader and Partnership Financial Statements Under UK GAAPDokumen28 halamanICAEW 2021 Chapter 15: Sole Trader and Partnership Financial Statements Under UK GAAPHankhnilBelum ada peringkat

- Monday 4 May 2020: AccountingDokumen20 halamanMonday 4 May 2020: AccountingDURAIMURUGAN MIS 17-18 MYP ACCOUNTS STAFFBelum ada peringkat

- Pub - Accounting A Foundation PDFDokumen705 halamanPub - Accounting A Foundation PDFwivadaBelum ada peringkat

- ch13 PDFDokumen83 halamanch13 PDFCoita Dewi100% (1)

- Rama Krishna Edible OilsDokumen24 halamanRama Krishna Edible OilskrishnanikhilBelum ada peringkat

- Chap 013Dokumen45 halamanChap 013daylicious88Belum ada peringkat

- Entrepreneurship ManagementDokumen18 halamanEntrepreneurship Managementcandy lollipoBelum ada peringkat

- Chap 014Dokumen67 halamanChap 014Nitesh Agrawal100% (2)

- Profit and Loss Statement TemplateDokumen6 halamanProfit and Loss Statement TemplateyashveerBelum ada peringkat

- Manufacture of Sulfuric Acid: S.R.M. Engineering CollegeDokumen76 halamanManufacture of Sulfuric Acid: S.R.M. Engineering CollegeCharles RiosBelum ada peringkat

- Manufacturing Account (With Answers) : Advanced LevelDokumen15 halamanManufacturing Account (With Answers) : Advanced LevelMomoh Kebiru0% (1)

- Mark Scheme (Results) Summer 2008: GCE Accounting (6002) Paper 01Dokumen19 halamanMark Scheme (Results) Summer 2008: GCE Accounting (6002) Paper 01Faiz Mohammed ChowdhuryBelum ada peringkat

- DepreciationDokumen26 halamanDepreciationBalu BalireddiBelum ada peringkat

- Acc Gr11 May 2009 PaperDokumen13 halamanAcc Gr11 May 2009 PaperSam ChristieBelum ada peringkat

- Registry of Public Infrastructures: - Registry of Reforestation Projects - Shall Be Maintained For Each CategoryDokumen31 halamanRegistry of Public Infrastructures: - Registry of Reforestation Projects - Shall Be Maintained For Each CategoryAllen Gonzaga100% (1)

- Auditing and Assurance Services A Systematic Approach Messier 8th Edition Solutions ManualDokumen13 halamanAuditing and Assurance Services A Systematic Approach Messier 8th Edition Solutions ManualRichardThomasrfizy100% (31)

- Estimated Balance Sheet 2020 PDFDokumen2 halamanEstimated Balance Sheet 2020 PDFsantosh ghotekarBelum ada peringkat

- Omde 606 Excel A2Dokumen8 halamanOmde 606 Excel A2api-237484773Belum ada peringkat