Anda mungkin juga menyukai

- 2 SampleDokumen23 halaman2 Sampleaaaaammmmm8900% (1)

- 2018 10 Exam FM Sample QuestionsDokumen137 halaman2018 10 Exam FM Sample QuestionsRuoyuBelum ada peringkat

- Sample FM QuestionsDokumen23 halamanSample FM Questionstimstarr88Belum ada peringkat

- Extra Problems For Test 1Dokumen4 halamanExtra Problems For Test 1night_98036Belum ada peringkat

- Practice Multiple Choice Test 5: I.J K IDokumen8 halamanPractice Multiple Choice Test 5: I.J K Iapi-3834751Belum ada peringkat

- ECN801 - F2012 Midterm2Dokumen15 halamanECN801 - F2012 Midterm2Zoloft Zithromax ProzacBelum ada peringkat

- Exam FM QuestioonsDokumen102 halamanExam FM Questioonsnkfran100% (1)

- Edu 2015 Exam FM Ques TheoryDokumen44 halamanEdu 2015 Exam FM Ques TheoryLueshen WellingtonBelum ada peringkat

- Edu 2015 Exam FM Ques Theory PDFDokumen65 halamanEdu 2015 Exam FM Ques Theory PDFAviR14Belum ada peringkat

- Edu 2015 Exam FM Ques Theory PDFDokumen65 halamanEdu 2015 Exam FM Ques Theory PDF彭雅欣Belum ada peringkat

- Interest Theory QuestionsDokumen65 halamanInterest Theory Questionsshivanithapar13100% (1)

- CH 6Dokumen24 halamanCH 6Joko AnilaBelum ada peringkat

- Practice Multiple Choice Test 3: II-llDokumen10 halamanPractice Multiple Choice Test 3: II-llapi-3834751Belum ada peringkat

- Feedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceDokumen30 halamanFeedback and Warm-Up Review: - Feedback of Your Requests - Cash Flow - Cash Flow Diagrams - Economic EquivalenceSajid IqbalBelum ada peringkat

- Practice Multiple Choice Test 8Dokumen8 halamanPractice Multiple Choice Test 8api-3834751Belum ada peringkat

- 5 Financial EvaluationDokumen22 halaman5 Financial EvaluationAdnan RizviBelum ada peringkat

- Edu 2009 Fall Exam FM QuesDokumen34 halamanEdu 2009 Fall Exam FM Quescl85ScribBelum ada peringkat

- Assg1Dokumen3 halamanAssg1WESTON MALAMABelum ada peringkat

- TVM-Practical QuestionsDokumen6 halamanTVM-Practical Questionsparag nimjeBelum ada peringkat

- Chapter Three (1) - 1Dokumen40 halamanChapter Three (1) - 1Embassy and NGO jobsBelum ada peringkat

- Week 6Dokumen36 halamanWeek 6allaintamangBelum ada peringkat

- Md. Al Amin: Lecturer Department of Marketing Jagannath UniversityDokumen41 halamanMd. Al Amin: Lecturer Department of Marketing Jagannath UniversityMd. Ebrahim SheikhBelum ada peringkat

- Loan Prob SolDokumen3 halamanLoan Prob SolAnonymous pH3jHscX9Belum ada peringkat

- Compound InterestDokumen35 halamanCompound InterestToukaBelum ada peringkat

- Assignment 2 PDFDokumen10 halamanAssignment 2 PDFvamshiBelum ada peringkat

- Assignment 2Dokumen10 halamanAssignment 2নীল জোছনাBelum ada peringkat

- Exam FM Practice Exam 1Dokumen12 halamanExam FM Practice Exam 1nad_natt100% (2)

- 1.0 Time Value of MoneyDokumen54 halaman1.0 Time Value of MoneyAbuBakerBelum ada peringkat

- Math 149 Problem Set (Assignment)Dokumen8 halamanMath 149 Problem Set (Assignment)raddy.tahilBelum ada peringkat

- Assignment 3Dokumen8 halamanAssignment 3octoBelum ada peringkat

- Intro Finance QuestionsDokumen3 halamanIntro Finance QuestionsstanleyBelum ada peringkat

- Compound Interest Quiz 1-1 PDFDokumen10 halamanCompound Interest Quiz 1-1 PDFSurayyaBelum ada peringkat

- Exam FM Practice Exam 1 Answer KeyDokumen71 halamanExam FM Practice Exam 1 Answer Keynad_natt100% (1)

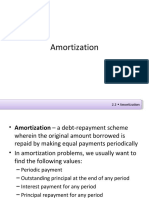

- AmortizationDokumen41 halamanAmortizationrichmond buquingBelum ada peringkat

- Chapter 9 - Time Value of MoneyDokumen29 halamanChapter 9 - Time Value of Moneyrohan angelBelum ada peringkat

- Today Agenda: Time Value of Money: PV FVDokumen10 halamanToday Agenda: Time Value of Money: PV FVNouman SheikhBelum ada peringkat

- Exam FM Practice Exam 3Dokumen71 halamanExam FM Practice Exam 3nad_nattBelum ada peringkat

- ACTL10001 Mid - Semester-Test - 2019+solutionsDokumen5 halamanACTL10001 Mid - Semester-Test - 2019+solutionsCheravinna Angesti MawarBelum ada peringkat

- Acs102 Fundamentals of Actuarial Science IDokumen6 halamanAcs102 Fundamentals of Actuarial Science IKimondo King100% (1)

- Chapter - ThreeDokumen19 halamanChapter - Threemagarsa hirphaBelum ada peringkat

- ProblemsDokumen28 halamanProblemsKevin NguyenBelum ada peringkat

- Microeconomics Canadian 1st Edition Karlan Test BankDokumen24 halamanMicroeconomics Canadian 1st Edition Karlan Test Bankanagogegirdler.kycgr100% (20)

- RSM 332 Problem Set #1Dokumen4 halamanRSM 332 Problem Set #1Paul Huang0% (1)

- Yield RatesDokumen9 halamanYield RatesDoco OkaBelum ada peringkat

- Exam FM Practice Exam With Answer KeyDokumen71 halamanExam FM Practice Exam With Answer KeyAki TsukiyomiBelum ada peringkat

- Finance - Solved Exercises 2Dokumen7 halamanFinance - Solved Exercises 2safura aliyevaBelum ada peringkat

- Edu 2012 04 MLC ExamDokumen30 halamanEdu 2012 04 MLC ExamsamiseechBelum ada peringkat

- Time Value of Money ConceptsDokumen18 halamanTime Value of Money ConceptsJoko AnilaBelum ada peringkat

- Practice Multiple Choice Test 9: .08 (1n C) /.08 (LN 2.5)Dokumen8 halamanPractice Multiple Choice Test 9: .08 (1n C) /.08 (LN 2.5)api-3834751Belum ada peringkat

- S Fma 7 PDFDokumen55 halamanS Fma 7 PDFMuradBelum ada peringkat

- FM1 SolutionsDokumen34 halamanFM1 SolutionsAnton PopovBelum ada peringkat

- Continuous Compounding of InterestDokumen10 halamanContinuous Compounding of InterestMichael Angelo Dela CruzBelum ada peringkat

- Annuities ExplainedDokumen11 halamanAnnuities ExplainedAai A BabaBelum ada peringkat

- Tia 3Dokumen10 halamanTia 3Mariam MagedBelum ada peringkat

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Dari EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Penilaian: 5 dari 5 bintang5/5 (1)

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Dari EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Penilaian: 4.5 dari 5 bintang4.5/5 (5)

- Scan 0001Dokumen1 halamanScan 0001api-3834751Belum ada peringkat

- Practice Multiple Choice Test 3: II-llDokumen10 halamanPractice Multiple Choice Test 3: II-llapi-3834751Belum ada peringkat

- Practice Multiple Choice Test 4: AtidtDokumen9 halamanPractice Multiple Choice Test 4: Atidtapi-3834751Belum ada peringkat

- Practice Multiple Choice Test 7: (E) (D) (B) (A)Dokumen9 halamanPractice Multiple Choice Test 7: (E) (D) (B) (A)api-3834751Belum ada peringkat

- Practice Multiple Choice Test 9: .08 (1n C) /.08 (LN 2.5)Dokumen8 halamanPractice Multiple Choice Test 9: .08 (1n C) /.08 (LN 2.5)api-3834751Belum ada peringkat

- Practice Multiple Choice Test 8Dokumen8 halamanPractice Multiple Choice Test 8api-3834751Belum ada peringkat

- Chapter 5. Financial Analysis of Investment ProjectsDokumen40 halamanChapter 5. Financial Analysis of Investment ProjectsThư Bùi Thị AnhBelum ada peringkat

- Chap 005Dokumen65 halamanChap 005Fahmi Hamzah100% (1)

- Friend or Enemy MathDokumen1 halamanFriend or Enemy MathNedelyn PayaoBelum ada peringkat

- Interest Rate Derivatives - A Beginner's Module CurriculumDokumen66 halamanInterest Rate Derivatives - A Beginner's Module CurriculumPankaj Bhasin100% (1)

- Signed Off General Mathematics11 q1 m6 Simple and Compound Interests v3Dokumen32 halamanSigned Off General Mathematics11 q1 m6 Simple and Compound Interests v3Joy Dizon100% (1)

- Introduction 1Dokumen3 halamanIntroduction 1HDBelum ada peringkat

- Loan Amortization ScheduleDokumen10 halamanLoan Amortization ScheduleKimberly LagmanBelum ada peringkat

- Calculate Future and Present Values of InvestmentsDokumen13 halamanCalculate Future and Present Values of InvestmentsNguyen Ngoc Thanh (K17 HCM)Belum ada peringkat

- Module 5 - Mathematics of FinanceDokumen6 halamanModule 5 - Mathematics of FinanceBangunan Mengfie Jr.Belum ada peringkat

- MCQ in Engineering Economics Part 11 | ECE Board Exam MCQsDokumen19 halamanMCQ in Engineering Economics Part 11 | ECE Board Exam MCQsDaryl GwapoBelum ada peringkat

- ASS Subject Review 2019 Mid Year PDFDokumen157 halamanASS Subject Review 2019 Mid Year PDFMangala PrasetiaBelum ada peringkat

- Chapter 3 (The Time Value of Money)Dokumen22 halamanChapter 3 (The Time Value of Money)Wilson Dhruba KuluntunuBelum ada peringkat

- Practice Set Time Value of MoneyDokumen5 halamanPractice Set Time Value of MoneyKena Montes Dela PeñaBelum ada peringkat

- MATH 01 Week 11 12 Simple and Compound InterestDokumen47 halamanMATH 01 Week 11 12 Simple and Compound InterestZandriex Tan100% (1)

- Compound Interest Application: Learner's Module in General MathematicsDokumen21 halamanCompound Interest Application: Learner's Module in General MathematicsZack William100% (1)

- Quant - Simple & Compound Interest v2Dokumen5 halamanQuant - Simple & Compound Interest v2Sourin BisalBelum ada peringkat

- Managerical Economics Web VersionDokumen229 halamanManagerical Economics Web VersionBHUVANA SUNDARBelum ada peringkat

- CRT 3rd Year NewDokumen232 halamanCRT 3rd Year NewAkshat agrawalBelum ada peringkat

- Chapter 4 Time Value of Money (Part1)Dokumen41 halamanChapter 4 Time Value of Money (Part1)AbdBelum ada peringkat

- Activity Sheets Obj. 3Dokumen7 halamanActivity Sheets Obj. 3BOBBY BRAIN ANGOSBelum ada peringkat

- E-Marking Notes On General Mathematics SSC I May 2016Dokumen33 halamanE-Marking Notes On General Mathematics SSC I May 2016Mir MusadiqBelum ada peringkat

- Important Compound Interest Practice QuestionsDokumen12 halamanImportant Compound Interest Practice QuestionsKothapalli VinayBelum ada peringkat

- Power of CompoundingDokumen5 halamanPower of CompoundingDasher_No_150% (2)

- Ce22 04 TVM 1 PDFDokumen36 halamanCe22 04 TVM 1 PDFEmman Joshua BustoBelum ada peringkat

- Simple & Compound Interest Practice QuestionsDokumen2 halamanSimple & Compound Interest Practice QuestionsShiVâ Sãi100% (1)

- DocumentDokumen80 halamanDocumentzohaib bilgramiBelum ada peringkat

- How Money WorksDokumen32 halamanHow Money Worksapi-284998491100% (6)

- CompoundDokumen6 halamanCompoundHarvey Leo RomanoBelum ada peringkat

- GenMath Q2 M2Dokumen106 halamanGenMath Q2 M2erikanavzabriganaBelum ada peringkat

- Chapter 5: The Time Value of MoneyDokumen34 halamanChapter 5: The Time Value of MoneyDharmesh GoyalBelum ada peringkat