Anda mungkin juga menyukai

- GST Question BankDokumen109 halamanGST Question Bankneeraj goyalBelum ada peringkat

- Hapter 9-Company AccountsDokumen48 halamanHapter 9-Company AccountsJINENDRA JAINBelum ada peringkat

- Goods and Service Tax: Submitted To DR. Gulnaz BanuDokumen21 halamanGoods and Service Tax: Submitted To DR. Gulnaz BanuShrutiBelum ada peringkat

- Financial Management Mba Question PaperDokumen4 halamanFinancial Management Mba Question Paperpalak2407Belum ada peringkat

- Assessment of Co-Operative SocietiesDokumen10 halamanAssessment of Co-Operative SocietiesrajeshvjdBelum ada peringkat

- Tutorial 1 & 2Dokumen11 halamanTutorial 1 & 2Annyi Chan100% (1)

- GSTDokumen51 halamanGSTINDERDEEPBelum ada peringkat

- Account PlansDokumen6 halamanAccount PlansaniketpavlekarBelum ada peringkat

- Honda Activa 4G Owners ManualDokumen75 halamanHonda Activa 4G Owners ManualRoyal EBelum ada peringkat

- Credit ReportDokumen23 halamanCredit ReportHDFC BANKBelum ada peringkat

- NYSE & NASDAQ New 52 Week Highs and Lows - 20220510Dokumen58 halamanNYSE & NASDAQ New 52 Week Highs and Lows - 20220510matrixitBelum ada peringkat

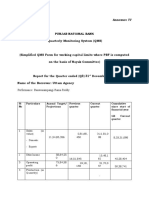

- Annexure IV Simplified QMSDokumen2 halamanAnnexure IV Simplified QMSIndra Nag Prasad0% (2)

- E-Book On GST by CA. (DR.) G. S. Grewal - 2020Dokumen58 halamanE-Book On GST by CA. (DR.) G. S. Grewal - 2020Aarav DhingraBelum ada peringkat

- Tutorial 1 PDFDokumen2 halamanTutorial 1 PDFchirag chhabraBelum ada peringkat

- Tax Invoice, Debit Note and Credit Note PDFDokumen29 halamanTax Invoice, Debit Note and Credit Note PDFNaveed AnsariBelum ada peringkat

- Customs DutyDokumen27 halamanCustoms DutyMANSI MANOJ 1923061Belum ada peringkat

- Jyoti-2017-2018 Bank Statement PDFDokumen1 halamanJyoti-2017-2018 Bank Statement PDFjyoti moreBelum ada peringkat

- E-Filing PresentationDokumen48 halamanE-Filing PresentationAnkit Mehta R67% (3)

- Cash FlowDokumen25 halamanCash Flowshaheen_khan6787Belum ada peringkat

- GST STeps To File ReturnDokumen22 halamanGST STeps To File ReturnAnnu KashyapBelum ada peringkat

- Ca Inter Advanced Accounting MCQDokumen210 halamanCa Inter Advanced Accounting MCQVikramBelum ada peringkat

- Accounts (1) FinalDokumen28 halamanAccounts (1) FinalManan MullickBelum ada peringkat

- Module I - Income Tax and GSTDokumen4 halamanModule I - Income Tax and GSTMuhammed Yaseen MBelum ada peringkat

- Act202-Project Final. Tea StallDokumen17 halamanAct202-Project Final. Tea StallAniruddha Rantu100% (1)

- Family Health Optima - RevisedDokumen33 halamanFamily Health Optima - Revisedcuckoo1976Belum ada peringkat

- Ifs Cia 1Dokumen12 halamanIfs Cia 1sachith chandrasekaranBelum ada peringkat

- GST User ManuelDokumen195 halamanGST User Manuelsakthi raoBelum ada peringkat

- FA-6 Banking Company Final Accounts RevisedDokumen20 halamanFA-6 Banking Company Final Accounts RevisedPaulomi LahaBelum ada peringkat

- Vardhman Textile 2011 12 PDFDokumen84 halamanVardhman Textile 2011 12 PDFSachin PatilBelum ada peringkat

- Nov 2019Dokumen39 halamanNov 2019amitha g.sBelum ada peringkat

- Course 1 The Commercial Corporate Credit Landscape in India PDFDokumen57 halamanCourse 1 The Commercial Corporate Credit Landscape in India PDFShikha Sharma100% (1)

- Int Computer Center Busy Test Marks:70 Time:1 HRDokumen2 halamanInt Computer Center Busy Test Marks:70 Time:1 HRMonika VermaBelum ada peringkat

- Deductions U/s 80C To 80 U From Gross Total Income: For The AY-2018-19 FY-2017-18Dokumen19 halamanDeductions U/s 80C To 80 U From Gross Total Income: For The AY-2018-19 FY-2017-18Shamrao GhodakeBelum ada peringkat

- Capm HDFC BankDokumen8 halamanCapm HDFC BankSushree SmitaBelum ada peringkat

- Kapil ChitsDokumen14 halamanKapil ChitsAnonymous 22GBLsme1Belum ada peringkat

- 7 Deductions ICAI SM + PCA + Past RTPs + Past Exam Questions WatermarkDokumen25 halaman7 Deductions ICAI SM + PCA + Past RTPs + Past Exam Questions WatermarkSavya SachiBelum ada peringkat

- DuplicateDokumen4 halamanDuplicateSamrat DBelum ada peringkat

- ICICI Merchant ServicesDokumen4 halamanICICI Merchant ServicesPranav GandhiBelum ada peringkat

- Articleship Exam QuestionsDokumen33 halamanArticleship Exam QuestionsVarshiniBelum ada peringkat

- 7 Finalnew Sugg June09Dokumen17 halaman7 Finalnew Sugg June09mknatoo1963Belum ada peringkat

- CA Inter Paper 6 All Question PapersDokumen116 halamanCA Inter Paper 6 All Question PapersNivedita SharmaBelum ada peringkat

- Schedule of Charges: Smart Salary ExclusiveDokumen2 halamanSchedule of Charges: Smart Salary ExclusivevedavakBelum ada peringkat

- TdsDokumen4 halamanTdsshanikaBelum ada peringkat

- Study Note 3, Page 148-196Dokumen49 halamanStudy Note 3, Page 148-196samstarmoonBelum ada peringkat

- Joint Product by ProductDokumen19 halamanJoint Product by ProductDhilipkumarBelum ada peringkat

- TDSDokumen18 halamanTDSPratik NaikBelum ada peringkat

- Ilovepdf MergedDokumen21 halamanIlovepdf MergedDILEEP COMPUTERS0% (1)

- Goods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLADokumen30 halamanGoods and Services Tax (GST) in India: A Presentation by KRISHNA SHUKLAKrishna ShuklaBelum ada peringkat

- 30/03/2013 IH00320590 File No.: Date:: Instrument Type Instrument No. Instrument Date Amount (INR) Infavour ofDokumen6 halaman30/03/2013 IH00320590 File No.: Date:: Instrument Type Instrument No. Instrument Date Amount (INR) Infavour ofAjay DudejaBelum ada peringkat

- Goods and Services Tax in India Progress Performance and Prospects Goods and Services Tax in India Progress Performance and ProspectsDokumen41 halamanGoods and Services Tax in India Progress Performance and Prospects Goods and Services Tax in India Progress Performance and Prospectsshaurya JainBelum ada peringkat

- Unit 7 Cash and Funds Flow StatementsDokumen85 halamanUnit 7 Cash and Funds Flow StatementsASIFBelum ada peringkat

- 2018-Income-Statement Copy-2Dokumen9 halaman2018-Income-Statement Copy-2api-464285260Belum ada peringkat

- Mid MCDokumen47 halamanMid MCPhuong PhamBelum ada peringkat

- Unit1 GSTDokumen26 halamanUnit1 GSTAryan SethiBelum ada peringkat

- Ready Reckoner For Preparing GSTR-9Dokumen12 halamanReady Reckoner For Preparing GSTR-9SATVINDER WALIABelum ada peringkat

- EX - NO:1 Company Creation Query:: Computerized Accounting PracticalDokumen15 halamanEX - NO:1 Company Creation Query:: Computerized Accounting PracticalJinson K JBelum ada peringkat

- Jyoti Joshi HDFCDokumen3 halamanJyoti Joshi HDFCJyoti JoshiBelum ada peringkat

- Loans and Advances 2016Dokumen128 halamanLoans and Advances 2016Anonymous kyvLgSREMBelum ada peringkat

- FBR IncomeTax Return 2016Dokumen40 halamanFBR IncomeTax Return 2016Muhammad Awais100% (1)

- Minimum Alternate TaxDokumen8 halamanMinimum Alternate Taxjainrahul234Belum ada peringkat

- CF - Section A - DR - Sudhindra BhatDokumen5 halamanCF - Section A - DR - Sudhindra BhatAbarna LoganathanBelum ada peringkat

- Multi CurvesDokumen32 halamanMulti CurvesdeepzcBelum ada peringkat

- Project Report: Akrash Mehrotra Dr. Sankalp SrivastavaDokumen120 halamanProject Report: Akrash Mehrotra Dr. Sankalp Srivastavasharath kumarBelum ada peringkat

- Function of GAAP PDFDokumen2 halamanFunction of GAAP PDFnarendraBelum ada peringkat

- Module 5 - Assessment ActivitiesDokumen4 halamanModule 5 - Assessment Activitiesaj dumpBelum ada peringkat

- Dwarka Das Agarwal: Summary of Rated InstrumentDokumen3 halamanDwarka Das Agarwal: Summary of Rated InstrumentVinaykumar MunjiBelum ada peringkat

- Basics of Portfolio Planning and Construction: Presenter Venue DateDokumen32 halamanBasics of Portfolio Planning and Construction: Presenter Venue DateAnonymous 45z6m4eE7pBelum ada peringkat

- Capital Budgeting TopicDokumen8 halamanCapital Budgeting TopicraderpinaBelum ada peringkat

- Financial Profile Analysis of Square Pharmaceuticals Limited BangladeshDokumen32 halamanFinancial Profile Analysis of Square Pharmaceuticals Limited Bangladeshrrashadatt75% (4)

- SALN FormDokumen2 halamanSALN FormFernando B. LopezBelum ada peringkat

- Accounting For SMEs QuestionnaireDokumen4 halamanAccounting For SMEs QuestionnaireGirlie Sison100% (1)

- Educational Material - ICAI Valuation Standard 103 - Valuation Approaches and MethodsDokumen172 halamanEducational Material - ICAI Valuation Standard 103 - Valuation Approaches and MethodsJishnuNichinBelum ada peringkat

- BLL12 - Introduction To NI ActDokumen3 halamanBLL12 - Introduction To NI Actsvm kishoreBelum ada peringkat

- Banking, Financial & General Awareness 2015 For Upcoming ExamsDokumen166 halamanBanking, Financial & General Awareness 2015 For Upcoming Examsshubh9190100% (1)

- Introduction To The Indian Stock MarketDokumen19 halamanIntroduction To The Indian Stock MarketAakanksha SanctisBelum ada peringkat

- Alasseel Financial ResultsDokumen17 halamanAlasseel Financial ResultsmohamedBelum ada peringkat

- Case StudyDokumen2 halamanCase Studyaly catBelum ada peringkat

- 01 - FAR - MODULE 3 - Investments - Agriculture - Borrowing CostDokumen10 halaman01 - FAR - MODULE 3 - Investments - Agriculture - Borrowing CostKristine TiuBelum ada peringkat

- Important Banking Awareness PDFDokumen193 halamanImportant Banking Awareness PDFsidBelum ada peringkat

- Fundamentals of Accounting 1 Draft PDFDokumen78 halamanFundamentals of Accounting 1 Draft PDFyumira khateBelum ada peringkat

- TAX - Documentary Stamp Tax CasesDokumen9 halamanTAX - Documentary Stamp Tax CasesMarife Tubilag ManejaBelum ada peringkat

- Rishabh Kumar Agarwal: Education & Academic AchievementsDokumen1 halamanRishabh Kumar Agarwal: Education & Academic Achievementsapurva1195Belum ada peringkat

- GS 2008 Entire Annual ReportDokumen162 halamanGS 2008 Entire Annual ReportlelaissezfaireBelum ada peringkat

- Balance of PaymentDokumen26 halamanBalance of Paymentnitan4zaara100% (3)

- Ratio Analysis of WiproDokumen7 halamanRatio Analysis of Wiprosandeepl4720% (2)

- Resume Prakhar OmarDokumen1 halamanResume Prakhar Omarcorporate relationBelum ada peringkat

- Next Gen BankingDokumen8 halamanNext Gen BankingTarang Shah0% (1)

- Resume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingDokumen9 halamanResume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingAbdul Aziz FaqihBelum ada peringkat

- Unit 1Dokumen16 halamanUnit 1Rahul kumar100% (1)

- Marketing MCQSDokumen5 halamanMarketing MCQSspeaktoerumBelum ada peringkat