Anda mungkin juga menyukai

- Chart of Accounts: BackgroundDokumen10 halamanChart of Accounts: Backgroundjohn irsyamBelum ada peringkat

- Chapter 1Dokumen22 halamanChapter 1Severus HadesBelum ada peringkat

- Service Delivery Model A Complete Guide - 2021 EditionDari EverandService Delivery Model A Complete Guide - 2021 EditionBelum ada peringkat

- Quickbooks Month End Close ChecklistDokumen2 halamanQuickbooks Month End Close ChecklistNyasha MakoreBelum ada peringkat

- Daylong Training On QuickBooks OnlineDokumen45 halamanDaylong Training On QuickBooks OnlineMoshiar RahmanBelum ada peringkat

- Sales Tax GuideDokumen6 halamanSales Tax GuideakhileshkantBelum ada peringkat

- Income Tax Under Canadian RegulationsDokumen10 halamanIncome Tax Under Canadian Regulationshemayal0% (1)

- Financial Leverage Ratios, Sometimes Called Equity or Debt Ratios, MeasureDokumen11 halamanFinancial Leverage Ratios, Sometimes Called Equity or Debt Ratios, MeasureBonDocEldRicBelum ada peringkat

- Chapter 1 Quickbooks Online Test Drive NovellaDokumen52 halamanChapter 1 Quickbooks Online Test Drive NovellaBest IT ProductsBelum ada peringkat

- Open Zero Balance Savings Account Online - Kotak 811Dokumen8 halamanOpen Zero Balance Savings Account Online - Kotak 811Mr. DuedullBelum ada peringkat

- Registration Procedure Under Central Sales Act (SectionDokumen23 halamanRegistration Procedure Under Central Sales Act (SectionkgudiyaBelum ada peringkat

- What Is Bank Reconciliation?Dokumen5 halamanWhat Is Bank Reconciliation?ayesha_khalidBelum ada peringkat

- Cargo Express Freight PRDokumen3 halamanCargo Express Freight PRRavinder VermaBelum ada peringkat

- DTC ProvisionsDokumen3 halamanDTC ProvisionsrajdeeppawarBelum ada peringkat

- Administrative Processing A Complete Guide - 2019 EditionDari EverandAdministrative Processing A Complete Guide - 2019 EditionBelum ada peringkat

- Chapter-5-Drafting Fundamental Documents PDFDokumen4 halamanChapter-5-Drafting Fundamental Documents PDFShubham AgarwalBelum ada peringkat

- QuickBooks Training &global Certification - IndiaDokumen10 halamanQuickBooks Training &global Certification - IndiaswayamBelum ada peringkat

- Law of PersonsDokumen21 halamanLaw of PersonsFatma KhamisBelum ada peringkat

- Direct Tax CodeDokumen25 halamanDirect Tax CodeHk MeherBelum ada peringkat

- QUICKBOOKS COURSE COMPLETE Edit Right PDFDokumen327 halamanQUICKBOOKS COURSE COMPLETE Edit Right PDFrbreddy74Belum ada peringkat

- Accounting TerminologiesDokumen16 halamanAccounting TerminologiesRidhanrhsnBelum ada peringkat

- Payroll Brochure For Prospective ClientsDokumen2 halamanPayroll Brochure For Prospective Clientsanon-414607100% (3)

- Asset RegisterDokumen51 halamanAsset RegisterangelBelum ada peringkat

- All About Credit Reports - Rev2Dokumen8 halamanAll About Credit Reports - Rev2kabBelum ada peringkat

- Equifax - Canadian Income PredictorDokumen2 halamanEquifax - Canadian Income PredictorANDREW SAMPSONBelum ada peringkat

- Invoice 420351761Dokumen2 halamanInvoice 420351761uxunBelum ada peringkat

- Risk ManagementDokumen15 halamanRisk ManagementanupkallatBelum ada peringkat

- Sample Chart of AccountsDokumen15 halamanSample Chart of AccountsFhandy RihiBelum ada peringkat

- Advanced Tax Laws CS Professional, YES AcademyDokumen33 halamanAdvanced Tax Laws CS Professional, YES AcademyKaran AroraBelum ada peringkat

- Tax Codes TransportDokumen2 halamanTax Codes TransportVenkat ReddyBelum ada peringkat

- Companies Law: Presented by Deepshikha Meeta Nikita ShivaniDokumen63 halamanCompanies Law: Presented by Deepshikha Meeta Nikita ShivaniSahil SherasiyaBelum ada peringkat

- USMCASmallBusinessExportChecklis PDFDokumen16 halamanUSMCASmallBusinessExportChecklis PDFAtif MahmoodBelum ada peringkat

- Offshore Accounting Outsourcing The Case of IndiaDokumen66 halamanOffshore Accounting Outsourcing The Case of IndiaPeter ThomasBelum ada peringkat

- Expenses and Vendors - Module IV Beginner SkillsDokumen26 halamanExpenses and Vendors - Module IV Beginner SkillsHumberto PortilloBelum ada peringkat

- Understanding Ebix IP Asset TransferDokumen41 halamanUnderstanding Ebix IP Asset TransferspinvestorBelum ada peringkat

- Prepare and Match ReciptsDokumen15 halamanPrepare and Match Reciptstafese kuracheBelum ada peringkat

- List of Business Transactions (Edited) : The Rose and Flower Owned by Rose GreenDokumen2 halamanList of Business Transactions (Edited) : The Rose and Flower Owned by Rose GreenJon DonBelum ada peringkat

- Intro To Bookkeeping - SlidesDokumen47 halamanIntro To Bookkeeping - SlidesEdemson NavalesBelum ada peringkat

- Supplemental Guide: Module 1: Complex ConversionsDokumen48 halamanSupplemental Guide: Module 1: Complex ConversionsEdward DubeBelum ada peringkat

- Credit Education: Credit Reports Sub-TabDokumen4 halamanCredit Education: Credit Reports Sub-TabmunivenkatBelum ada peringkat

- Oracle Customer Case Study Maruti Supports Business Growth With ScalableDokumen34 halamanOracle Customer Case Study Maruti Supports Business Growth With ScalableMohit GolechaBelum ada peringkat

- Legal Aspects of Business Unit 4 Ms Neha RaniDokumen123 halamanLegal Aspects of Business Unit 4 Ms Neha Ranihari haranBelum ada peringkat

- Recording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDDokumen34 halamanRecording Transactions: Powerpoint Presentation by Phil Johnson ©2015 John Wiley & Sons Australia LTDShiTheng Love UBelum ada peringkat

- Accounting Financial: General LedgerDokumen8 halamanAccounting Financial: General LedgerSumeet KaurBelum ada peringkat

- Chart of Accounts: Home BlogDokumen5 halamanChart of Accounts: Home BlogJose Luis Becerril BurgosBelum ada peringkat

- Fusion Accounts PayableDokumen68 halamanFusion Accounts PayableTanay BeheraBelum ada peringkat

- The Corporation Code of The Philippines B.P. Blg. 68: Lecture 3 (Parts 1 and 2) June 22, 2011Dokumen86 halamanThe Corporation Code of The Philippines B.P. Blg. 68: Lecture 3 (Parts 1 and 2) June 22, 2011MaanParrenoVillarBelum ada peringkat

- Joan Leach Approval LetterDokumen4 halamanJoan Leach Approval LetterutilitiesBelum ada peringkat

- Accounts - Accounts Receivable Process - Process - STDokumen10 halamanAccounts - Accounts Receivable Process - Process - STmatthew mafaraBelum ada peringkat

- 13 Free Tips To Make Your Windows PC Run Faster - PCWorldDokumen20 halaman13 Free Tips To Make Your Windows PC Run Faster - PCWorldBikash AhmedBelum ada peringkat

- Ethics ComplaintDokumen18 halamanEthics ComplaintRob PortBelum ada peringkat

- Protect Your IdentityDokumen8 halamanProtect Your IdentityChristopher MillerBelum ada peringkat

- webERP Manual PDFDokumen270 halamanwebERP Manual PDFLeonard MaramisBelum ada peringkat

- 2018-Income-Statement Copy-2Dokumen9 halaman2018-Income-Statement Copy-2api-464285260Belum ada peringkat

- Accounting Payroll Services 1Dokumen18 halamanAccounting Payroll Services 1Donna MarieBelum ada peringkat

- Debt Recovery AgentDokumen16 halamanDebt Recovery AgentrameshBelum ada peringkat

- Accounting ProcessDokumen79 halamanAccounting ProcessKeanna Ashley GutingBelum ada peringkat

- Enterprise Florida - Established Projects With Incentive Information FY 2011-2012Dokumen13 halamanEnterprise Florida - Established Projects With Incentive Information FY 2011-2012Integrity FloridaBelum ada peringkat

- Accounts Outsourcing, Outsourced Accounting and Bookkeeping ServicesDokumen16 halamanAccounts Outsourcing, Outsourced Accounting and Bookkeeping ServicespoortiBelum ada peringkat

- Mobey Forum Whitepaper - The MPOS Impact PDFDokumen32 halamanMobey Forum Whitepaper - The MPOS Impact PDFDeo ValenstinoBelum ada peringkat

- Property Tax Payment ReceiptDokumen3 halamanProperty Tax Payment ReceiptRagini KumariBelum ada peringkat

- Invoice JulyDokumen2 halamanInvoice JulyGabriel de Souza Pereira GomesBelum ada peringkat

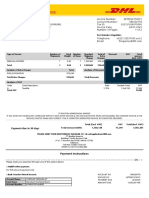

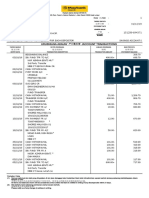

- Invoice DHL No. JKTR002114131Dokumen3 halamanInvoice DHL No. JKTR002114131Tri Wahyuni100% (2)

- Donor'S Tax: BIR Form 1800Dokumen4 halamanDonor'S Tax: BIR Form 1800JAYAR MENDZBelum ada peringkat

- Accounting For Labor ProblemsDokumen2 halamanAccounting For Labor ProblemsRyan Maliwat0% (1)

- Itzcash - Finly Expense Management: We Make Every Penny Ac'Count'Dokumen11 halamanItzcash - Finly Expense Management: We Make Every Penny Ac'Count'vinod1994Belum ada peringkat

- Statement - 652900 XXXX XXXX 2982 - 022023Dokumen2 halamanStatement - 652900 XXXX XXXX 2982 - 022023Vikrant JaiswalBelum ada peringkat

- Service Bill StatusDokumen2 halamanService Bill StatusKR RamanBelum ada peringkat

- Kerala State Electricity Board Limited: Demand Cum Disconnection NoticeDokumen2 halamanKerala State Electricity Board Limited: Demand Cum Disconnection NoticeAskar AsaruBelum ada peringkat

- Anil Neerukonda Institute of Technology & Sciences: Fee Structure For B.Tech., 1 Year 2018 - 2019Dokumen5 halamanAnil Neerukonda Institute of Technology & Sciences: Fee Structure For B.Tech., 1 Year 2018 - 2019p.narendraBelum ada peringkat

- Fixed Deposit Maintenance FormDokumen1 halamanFixed Deposit Maintenance FormSridhar Ramachandran SrinivasanBelum ada peringkat

- India: Type of Transactions CoveredDokumen20 halamanIndia: Type of Transactions Coveredss_scribdBelum ada peringkat

- Cpwa Form 2Dokumen5 halamanCpwa Form 2rkthbdBelum ada peringkat

- Blessing Plastic: Tax Invoice Original For CompanyDokumen1 halamanBlessing Plastic: Tax Invoice Original For CompanyCharles NaveenBelum ada peringkat

- VAT Syllabus - BaniquedDokumen5 halamanVAT Syllabus - BaniquedJN CEBelum ada peringkat

- Professional Fees CalculationDokumen1 halamanProfessional Fees CalculationKris Kachi NwanebuBelum ada peringkat

- 430 Si Rameswaram N Ac PDFDokumen6 halaman430 Si Rameswaram N Ac PDFSRI RAMANA SEVA ASHARAMAMBelum ada peringkat

- Usage Guide - Exclusive PDFDokumen36 halamanUsage Guide - Exclusive PDFHemant JainBelum ada peringkat

- Bangalore Electricity Supply Company Limited: Thank You!Dokumen12 halamanBangalore Electricity Supply Company Limited: Thank You!Ranjan VBelum ada peringkat

- Computing Gross Taxable Income and Tax DueDokumen21 halamanComputing Gross Taxable Income and Tax DuepearlBelum ada peringkat

- Number of Instalments and Payment Mode Received Date Coll. Br. Serv. Br. Premium/ Additional Premium Amount Service Tax / GST Amount ReceivedDokumen1 halamanNumber of Instalments and Payment Mode Received Date Coll. Br. Serv. Br. Premium/ Additional Premium Amount Service Tax / GST Amount ReceivedSaumy VishwakarmaBelum ada peringkat

- Hostel Fee ReceiptDokumen1 halamanHostel Fee Receiptanoucha JordanBelum ada peringkat

- Mixer Juicer BillDokumen1 halamanMixer Juicer BillRoshanBelum ada peringkat

- Ibs Tampoi 1 31/12/19Dokumen5 halamanIbs Tampoi 1 31/12/19Azani OmarBelum ada peringkat

- Orderconfirmation 2211375989 From 01.09.2021: VWR International GMBH AustriaDokumen2 halamanOrderconfirmation 2211375989 From 01.09.2021: VWR International GMBH Austriaarman1704Belum ada peringkat

- Jonathan M Luna Account Number: 5779 81XX XXXX 2560: Account Activity Since Your Last StatementDokumen4 halamanJonathan M Luna Account Number: 5779 81XX XXXX 2560: Account Activity Since Your Last StatementJonathan LunaBelum ada peringkat

- Deposit Confirmation/Renewal AdviceDokumen1 halamanDeposit Confirmation/Renewal AdviceRitu PatelBelum ada peringkat

- PFG Credit Card Design Solution-Part 2 Gaurav ChaturvediDokumen4 halamanPFG Credit Card Design Solution-Part 2 Gaurav Chaturvedikkiiidd0% (1)

- 6018-P1-SPK-AKUNTANSI-Data Mentah SoalDokumen20 halaman6018-P1-SPK-AKUNTANSI-Data Mentah Soaliqbal kamilBelum ada peringkat

- Remittance Transfers: Small Entity Compliance GuideDokumen46 halamanRemittance Transfers: Small Entity Compliance GuideAnomieBelum ada peringkat