Anda mungkin juga menyukai

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- John Carlton The Grizzled Pro ReportDokumen46 halamanJohn Carlton The Grizzled Pro ReportFabio Gomes100% (2)

- ICI Paints ProjectDokumen24 halamanICI Paints Projectlongman4200% (1)

- Commercial InvoiceDokumen4 halamanCommercial InvoiceEric Luna0% (1)

- Strategic Management Report On Unilever PakistanDokumen23 halamanStrategic Management Report On Unilever PakistanAbdur RehmanBelum ada peringkat

- Sale and Purchase Contract of Indonesian Bauxite: The SellerDokumen13 halamanSale and Purchase Contract of Indonesian Bauxite: The SellerRadhitya Adzan Hidayah67% (3)

- Ukay-Ukay Business - Is It Still FeasibleDokumen7 halamanUkay-Ukay Business - Is It Still FeasibleJayPee De Guzman100% (1)

- s) 商务英语口语900句Dokumen75 halamans) 商务英语口语900句07032007Belum ada peringkat

- Fraud Detection in The Financial Services IndustryDokumen24 halamanFraud Detection in The Financial Services Industrychiragjuneja234100% (3)

- THE HEIRS OF PROTACIO GO, SR. vs. SERVACIODokumen2 halamanTHE HEIRS OF PROTACIO GO, SR. vs. SERVACIOJoan MagasoBelum ada peringkat

- CH9-Capacity Planning and Location DecisionDokumen35 halamanCH9-Capacity Planning and Location DecisionChristian John Linalcoso Arante100% (1)

- Pricing Decisions: By: DR Shahinaz AbdellatifDokumen30 halamanPricing Decisions: By: DR Shahinaz AbdellatifLooga MoogaBelum ada peringkat

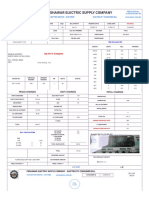

- Pesco Online Billl PDFDokumen2 halamanPesco Online Billl PDFFazal Rahim RahimBelum ada peringkat

- JD - TVS Motors - IMI New DelhiDokumen4 halamanJD - TVS Motors - IMI New DelhiChetan SaxenaBelum ada peringkat

- Quiz-Ch4 FJFJDokumen5 halamanQuiz-Ch4 FJFJAaron DudekBelum ada peringkat

- MKT 202 Course OutlineDokumen6 halamanMKT 202 Course OutlineFoo Cheok HwaBelum ada peringkat

- Forecasting The Revenues of The BusinessDokumen2 halamanForecasting The Revenues of The Businessveronica relente100% (1)

- 2014 Bar Exam QuestionsDokumen5 halaman2014 Bar Exam QuestionsMarrielDeTorresBelum ada peringkat

- Rizwan Munaf KhanDokumen2 halamanRizwan Munaf KhanSazeed Sha52hBelum ada peringkat

- Exercises: Unit: Sales - A/R Topic: Sales Process - Item Availability CheckDokumen4 halamanExercises: Unit: Sales - A/R Topic: Sales Process - Item Availability CheckClint-Daniel AbenojaBelum ada peringkat

- Monopoly: Monopoly and The Economic Analysis of Market StructuresDokumen15 halamanMonopoly: Monopoly and The Economic Analysis of Market StructuresYvonneBelum ada peringkat

- Suffolk Times Classifieds and Service Directory: Sept. 7, 2017Dokumen14 halamanSuffolk Times Classifieds and Service Directory: Sept. 7, 2017Timesreview0% (1)

- On Stock Turover RatioDokumen31 halamanOn Stock Turover RatioArpit RuiaBelum ada peringkat

- Analyzing Business Markets: Prepared By, Mr. Nishant AgrawalDokumen20 halamanAnalyzing Business Markets: Prepared By, Mr. Nishant AgrawalAisha NadeemBelum ada peringkat

- Next PLC - Press ReleaseDokumen20 halamanNext PLC - Press Releasecasefortrils0% (1)

- Spy Optic v. Alibaba PDFDokumen25 halamanSpy Optic v. Alibaba PDFMark JaffeBelum ada peringkat

- Unit 1Dokumen36 halamanUnit 1Sonny JoseBelum ada peringkat

- H.Randall TrialDokumen20 halamanH.Randall TrialMahad Imran100% (1)

- Corporate Communication II 7 To 10Dokumen9 halamanCorporate Communication II 7 To 10layfon519Belum ada peringkat

- Bedford Hills SFDokumen1 halamanBedford Hills SFapi-23721120Belum ada peringkat

- Tata NanoDokumen27 halamanTata NanoHardik MalaviaBelum ada peringkat