Anda mungkin juga menyukai

- Supervision of Banks and Nonbanks Operating Through AgentsDokumen49 halamanSupervision of Banks and Nonbanks Operating Through AgentsCGAP PublicationsBelum ada peringkat

- Smallholder Households: Understanding Demand, Driving InnovationDokumen15 halamanSmallholder Households: Understanding Demand, Driving InnovationCGAP PublicationsBelum ada peringkat

- Designing Digital Financial Services For Smallholder FamiliesDokumen44 halamanDesigning Digital Financial Services For Smallholder FamiliesCGAP PublicationsBelum ada peringkat

- Doing Digital Finance RightDokumen40 halamanDoing Digital Finance RightCGAP PublicationsBelum ada peringkat

- Competition in Mobile Financial Services: Lessons From Kenya &tanzaniaDokumen31 halamanCompetition in Mobile Financial Services: Lessons From Kenya &tanzaniaCGAP PublicationsBelum ada peringkat

- National Survey & Segmentation of Smallholder Households in MozambiqueDokumen90 halamanNational Survey & Segmentation of Smallholder Households in MozambiqueCGAP PublicationsBelum ada peringkat

- Mystery Shopping For Financial ServicesDokumen108 halamanMystery Shopping For Financial ServicesCGAP PublicationsBelum ada peringkat

- Juntos Finanzas: A Case StudyDokumen15 halamanJuntos Finanzas: A Case StudyCGAP PublicationsBelum ada peringkat

- Customer Empowerment Through Gamification: Absa SheshaDokumen8 halamanCustomer Empowerment Through Gamification: Absa SheshaCGAP PublicationsBelum ada peringkat

- Promoting Competition in Mobile Payments: The Role of USSDDokumen4 halamanPromoting Competition in Mobile Payments: The Role of USSDCGAP PublicationsBelum ada peringkat

- Early Insights From Financial Diaries of Smallholder HouseholdsDokumen20 halamanEarly Insights From Financial Diaries of Smallholder HouseholdsCGAP PublicationsBelum ada peringkat

- How M-Shwari Works: The Story So FarDokumen24 halamanHow M-Shwari Works: The Story So FarCGAP PublicationsBelum ada peringkat

- Financial Diaries With Smallholder FamiliesDokumen107 halamanFinancial Diaries With Smallholder FamiliesCGAP PublicationsBelum ada peringkat

- Costs and Sustainability of Sharia Compliant Microfinance ProductsDokumen12 halamanCosts and Sustainability of Sharia Compliant Microfinance ProductsCGAP PublicationsBelum ada peringkat

- Recourse in Digital Financial ServicesDokumen4 halamanRecourse in Digital Financial ServicesCGAP PublicationsBelum ada peringkat

- Spotlight On International Funders' Commitments To Financial InclusionDokumen4 halamanSpotlight On International Funders' Commitments To Financial InclusionCGAP PublicationsBelum ada peringkat

- Inclusive Finance and Shadow BankingDokumen4 halamanInclusive Finance and Shadow BankingCGAP PublicationsBelum ada peringkat

- Understanding Consumer Risks in Digital Social PaymentsDokumen4 halamanUnderstanding Consumer Risks in Digital Social PaymentsCGAP PublicationsBelum ada peringkat

- Current Trends in International FundingDokumen4 halamanCurrent Trends in International FundingCGAP PublicationsBelum ada peringkat

- Digital Financial InclusionDokumen4 halamanDigital Financial InclusionCGAP PublicationsBelum ada peringkat

- BKash Bangladesh: A Fast Start For Mobile Financial ServicesDokumen4 halamanBKash Bangladesh: A Fast Start For Mobile Financial ServicesCGAP PublicationsBelum ada peringkat

- Costs and Sustainability of Sharia Compliant Microfinance ProductsDokumen12 halamanCosts and Sustainability of Sharia Compliant Microfinance ProductsCGAP PublicationsBelum ada peringkat

- Facilitating The Market For Capacity Building ServicesDokumen16 halamanFacilitating The Market For Capacity Building ServicesCGAP PublicationsBelum ada peringkat

- The Potential of Digital Data: How Far Can It Advance Financial InclusionDokumen12 halamanThe Potential of Digital Data: How Far Can It Advance Financial InclusionCGAP PublicationsBelum ada peringkat

- Informed Consent in Mobile Credit ScoringDokumen20 halamanInformed Consent in Mobile Credit ScoringCGAP PublicationsBelum ada peringkat

- Smart Aid Index Brochure PDFDokumen4 halamanSmart Aid Index Brochure PDFCGAP PublicationsBelum ada peringkat

- Promoting Competition in Mobile Payments: The Role of USSDDokumen4 halamanPromoting Competition in Mobile Payments: The Role of USSDCGAP PublicationsBelum ada peringkat

- AML/CFT and Financial InclusionDokumen28 halamanAML/CFT and Financial InclusionCGAP PublicationsBelum ada peringkat

- Financial Inclusion in Russia: The Demand-Side PerspectiveDokumen134 halamanFinancial Inclusion in Russia: The Demand-Side PerspectiveCGAP PublicationsBelum ada peringkat

- Getting Smart About Financial InclusionDokumen12 halamanGetting Smart About Financial InclusionCGAP PublicationsBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Peanut Processing PlantDokumen19 halamanPeanut Processing PlantfaizkauBelum ada peringkat

- Loan LetterDokumen4 halamanLoan Lettermohd.hadi36Belum ada peringkat

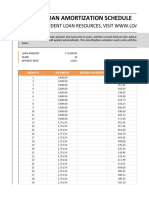

- Calculate student loan paymentsDokumen18 halamanCalculate student loan paymentsIsmail UsmanBelum ada peringkat

- Banking Operations ExplainedDokumen51 halamanBanking Operations Explainedamita venkateshBelum ada peringkat

- Definition, Benefits of Cash FlowDokumen2 halamanDefinition, Benefits of Cash FlowFerial FerniawanBelum ada peringkat

- Business Finance ABM StrandDokumen107 halamanBusiness Finance ABM StrandMiss Anonymous23Belum ada peringkat

- Partnership Acc - ScannerDokumen88 halamanPartnership Acc - ScannerAruna RajappaBelum ada peringkat

- Estimating Spot Rates and FWD Rates (Using Bootstrapping Method)Dokumen3 halamanEstimating Spot Rates and FWD Rates (Using Bootstrapping Method)9210490991Belum ada peringkat

- Tata Motors Equity Research ReportDokumen29 halamanTata Motors Equity Research Reportjohn paulBelum ada peringkat

- FA-III Question BankDokumen13 halamanFA-III Question BankmeenasarathaBelum ada peringkat

- Lala Trading's Profit & Loss, Assets & Equity for 2018Dokumen27 halamanLala Trading's Profit & Loss, Assets & Equity for 2018ummi sabrina100% (1)

- Oblicon (67Q)Dokumen8 halamanOblicon (67Q)Ron Nixon MendozaBelum ada peringkat

- PROJECT REPORT - Docx ForfaitingDokumen41 halamanPROJECT REPORT - Docx ForfaitingShwetha BvBelum ada peringkat

- Understanding the Cost of Capital from Investors' PerspectiveDokumen14 halamanUnderstanding the Cost of Capital from Investors' Perspectivejepu jepBelum ada peringkat

- Debts Recovery Tribunal - Laws & ProceduresDokumen3 halamanDebts Recovery Tribunal - Laws & ProceduresankitaBelum ada peringkat

- Equity Analysis of Vodafone PLCDokumen11 halamanEquity Analysis of Vodafone PLCBethelBelum ada peringkat

- PGINVIT - Q3 FY24 Earnings CallDokumen17 halamanPGINVIT - Q3 FY24 Earnings CallBuvanesh BalajiBelum ada peringkat

- English Learning Guide Competency 1 Unit 7: Business English Workshop 1 Centro de Servicios Financieros-CSFDokumen5 halamanEnglish Learning Guide Competency 1 Unit 7: Business English Workshop 1 Centro de Servicios Financieros-CSFKaren GaleanoBelum ada peringkat

- Islamic Finance Book - 2nd Edition PDFDokumen140 halamanIslamic Finance Book - 2nd Edition PDFMhmdBelum ada peringkat

- Birla Institute of Technology: Master of Business AdministrationDokumen16 halamanBirla Institute of Technology: Master of Business Administrationdixit_abhishek_neoBelum ada peringkat

- Automatic Millionaire PDFDokumen23 halamanAutomatic Millionaire PDFلاجئة لله100% (13)

- Description: Tags: 06 Top 100 Current Holders PublicDokumen3 halamanDescription: Tags: 06 Top 100 Current Holders Publicanon-603613Belum ada peringkat

- Unit 2 (Fundamental Analysis)Dokumen19 halamanUnit 2 (Fundamental Analysis)Ramya RamamurthyBelum ada peringkat

- PArtDokumen6 halamanPArtMay DabuBelum ada peringkat

- Rehabilitation Finance Corp. v. Court of Appeals ruling on third party debt paymentDokumen2 halamanRehabilitation Finance Corp. v. Court of Appeals ruling on third party debt paymentJet Siang100% (3)

- PV 5Dokumen23 halamanPV 52guntanBelum ada peringkat

- ObligationsDokumen10 halamanObligationsCharrie Grace Pablo100% (1)

- Straight-Line Amortization of Bond PremiumDokumen4 halamanStraight-Line Amortization of Bond PremiumMarko Zero FourBelum ada peringkat

- Assess Hutchison WhampoaDokumen4 halamanAssess Hutchison WhampoaAyesha KhalidBelum ada peringkat