Anda mungkin juga menyukai

- Supreme Court Rules in Favor of Driver in Collision CaseDokumen10 halamanSupreme Court Rules in Favor of Driver in Collision CaseLeomard SilverJoseph Centron LimBelum ada peringkat

- CC Event TemplateDokumen12 halamanCC Event TemplateLeomard SilverJoseph Centron LimBelum ada peringkat

- G.R. No. 75885Dokumen26 halamanG.R. No. 75885Leomard SilverJoseph Centron LimBelum ada peringkat

- Principles of Constitutional ConstructionDokumen11 halamanPrinciples of Constitutional ConstructionLeomard SilverJoseph Centron LimBelum ada peringkat

- Torts Compilation - Standard of ConductDokumen143 halamanTorts Compilation - Standard of ConductLeomard SilverJoseph Centron LimBelum ada peringkat

- IRR A Amended v2006Dokumen12 halamanIRR A Amended v2006Leomard SilverJoseph Centron LimBelum ada peringkat

- IRR A Amended v2006Dokumen12 halamanIRR A Amended v2006Leomard SilverJoseph Centron LimBelum ada peringkat

- Two Schools of Thought On The Bangsamoro BillDokumen6 halamanTwo Schools of Thought On The Bangsamoro BillLeomard SilverJoseph Centron LimBelum ada peringkat

- 2016 Revised IRR Clean Format and Annexes 26 August 2016 PDFDokumen149 halaman2016 Revised IRR Clean Format and Annexes 26 August 2016 PDFRyan JD LimBelum ada peringkat

- Implementing Rules RegulationsDokumen125 halamanImplementing Rules RegulationsDennis TolentinoBelum ada peringkat

- HB 00248Dokumen4 halamanHB 00248Leomard SilverJoseph Centron LimBelum ada peringkat

- BBL Needs Charter Change, Says Senate ReportDokumen3 halamanBBL Needs Charter Change, Says Senate ReportLeomard SilverJoseph Centron LimBelum ada peringkat

- GST AnswersDokumen2 halamanGST AnswersLeomard SilverJoseph Centron LimBelum ada peringkat

- Red Notes: Mercantile LawDokumen36 halamanRed Notes: Mercantile Lawjojitus100% (2)

- MotEx Addl FormDokumen3 halamanMotEx Addl FormLeomard SilverJoseph Centron LimBelum ada peringkat

- Icj 7Dokumen19 halamanIcj 7Leomard SilverJoseph Centron LimBelum ada peringkat

- Barons Marketing Vs - CaDokumen4 halamanBarons Marketing Vs - CaLeomard SilverJoseph Centron LimBelum ada peringkat

- JURIS FE physician consent dialysis benefitsDokumen2 halamanJURIS FE physician consent dialysis benefitsLeomard SilverJoseph Centron Lim100% (1)

- For SribdDokumen1 halamanFor SribdLeomard SilverJoseph Centron LimBelum ada peringkat

- Tax CasesDokumen12 halamanTax CasesLeomard SilverJoseph Centron LimBelum ada peringkat

- 14-027032 NoaDokumen1 halaman14-027032 NoaLeomard SilverJoseph Centron LimBelum ada peringkat

- History of BangsamoroDokumen1 halamanHistory of BangsamoroLeomard SilverJoseph Centron LimBelum ada peringkat

- For Sribd3Dokumen1 halamanFor Sribd3Leomard SilverJoseph Centron LimBelum ada peringkat

- Recruitment ProcessDokumen1 halamanRecruitment ProcessLeomard SilverJoseph Centron LimBelum ada peringkat

- For Sribd2Dokumen1 halamanFor Sribd2Leomard SilverJoseph Centron LimBelum ada peringkat

- Icj 7Dokumen19 halamanIcj 7Leomard SilverJoseph Centron LimBelum ada peringkat

- For SribdDokumen1 halamanFor SribdLeomard SilverJoseph Centron LimBelum ada peringkat

- Icj 7Dokumen19 halamanIcj 7Leomard SilverJoseph Centron LimBelum ada peringkat

- Icj 7Dokumen19 halamanIcj 7Leomard SilverJoseph Centron LimBelum ada peringkat

- International Court of Justice3Dokumen12 halamanInternational Court of Justice3Leomard SilverJoseph Centron LimBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Littlefield Technologies Final Report RedesvouzDokumen10 halamanLittlefield Technologies Final Report RedesvouzLuis MonteroBelum ada peringkat

- Arizona Tax Rates TableDokumen18 halamanArizona Tax Rates TableKaryll Trinidad AyangcoBelum ada peringkat

- MANAGEMENT ACCOUNTING RATIO ANALYSIS QUESTIONSDokumen10 halamanMANAGEMENT ACCOUNTING RATIO ANALYSIS QUESTIONSNaveen ReddyBelum ada peringkat

- Labangan Calamansi PlantationDokumen38 halamanLabangan Calamansi PlantationLorisa CenizaBelum ada peringkat

- Complete Exhibit 3. Provide The Answers in A Table FormatDokumen5 halamanComplete Exhibit 3. Provide The Answers in A Table FormatSajan Jose100% (2)

- Indian Aviation Industry - Indigo AirlinesDokumen13 halamanIndian Aviation Industry - Indigo AirlinesArjun Pratap SinghBelum ada peringkat

- Mcdonalds Final Supply ChainDokumen34 halamanMcdonalds Final Supply ChainAmmar Imtiaz100% (1)

- Asian Paints Limited Consolidated Balance SheetDokumen40 halamanAsian Paints Limited Consolidated Balance SheetSehajpal SanghuBelum ada peringkat

- Netherlands Totalization Agreement ExplainedDokumen11 halamanNetherlands Totalization Agreement ExplainedfdarteeBelum ada peringkat

- N Retail Full Mock T4-1Dokumen6 halamanN Retail Full Mock T4-1Josiah MwashitaBelum ada peringkat

- Ravi ResumeDokumen3 halamanRavi ResumeKeerthanaBelum ada peringkat

- Principles of Accounting I (ACFN 211)Dokumen65 halamanPrinciples of Accounting I (ACFN 211)Habibuna Mohammed100% (5)

- Statement of Defence of Stronach Consulting Corp.Dokumen31 halamanStatement of Defence of Stronach Consulting Corp.CTV News100% (1)

- May 20, 2015 Tribune Record GleanerDokumen20 halamanMay 20, 2015 Tribune Record GleanercwmediaBelum ada peringkat

- Body of The ReportDokumen26 halamanBody of The Reportahmed_zavedBelum ada peringkat

- Tax On Individuals Quiz - ProblemsDokumen3 halamanTax On Individuals Quiz - ProblemsJP Mirafuentes100% (1)

- Practical Accounting Problem 1Dokumen19 halamanPractical Accounting Problem 1Christine Nicole BacoBelum ada peringkat

- The Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresDokumen30 halamanThe Expenditure Cycle Part II: Payroll Processing and Fixed Asset ProceduresabmyonisBelum ada peringkat

- Characteristics of Fortune Global 500 - Assignment-2 - Akhil and NamuunDokumen53 halamanCharacteristics of Fortune Global 500 - Assignment-2 - Akhil and NamuunAkhil Agarwal100% (1)

- Nestlé Audit Committee OversightDokumen2 halamanNestlé Audit Committee OversightDisha ShekarBelum ada peringkat

- BDokumen4 halamanBsakuraBelum ada peringkat

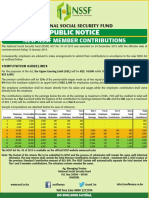

- Public Notice: New NSSF Member ContributionsDokumen1 halamanPublic Notice: New NSSF Member ContributionsDiana Dekatrinah KatrineBelum ada peringkat

- TCS Profit Up 50%, Declares 1:1 Bonus, 1,350% DividendDokumen6 halamanTCS Profit Up 50%, Declares 1:1 Bonus, 1,350% DividendBhaskar NiraulaBelum ada peringkat

- Management Accounting: Level 3Dokumen18 halamanManagement Accounting: Level 3Hein Linn KyawBelum ada peringkat

- Student Proposal 2Dokumen6 halamanStudent Proposal 2aman_lallyBelum ada peringkat

- 12th Biology Important 235 Mark Questions English Medium PDF DownloadDokumen6 halaman12th Biology Important 235 Mark Questions English Medium PDF DownloadNandhakumarBelum ada peringkat

- Norwich Manufacturing Inc Provided You With The Following Comparative BalanceDokumen1 halamanNorwich Manufacturing Inc Provided You With The Following Comparative BalanceFreelance WorkerBelum ada peringkat

- Tax Accounting: Tax On Profit of Juridical PersonsDokumen42 halamanTax Accounting: Tax On Profit of Juridical PersonsBasma MohamedBelum ada peringkat

- Conceptual Framework Purpose Assist Standards Developed IFRSDokumen6 halamanConceptual Framework Purpose Assist Standards Developed IFRSKyleZapantaBelum ada peringkat

- Shuttle Cock Manufacturing Project ProfileDokumen5 halamanShuttle Cock Manufacturing Project Profilepradip_kumarBelum ada peringkat