Anda mungkin juga menyukai

- Depreciation Methods and Composite Rates CalculationDokumen2 halamanDepreciation Methods and Composite Rates CalculationSwiss Han100% (2)

- Management Accounting: Page 1 of 6Dokumen70 halamanManagement Accounting: Page 1 of 6Ahmed Raza MirBelum ada peringkat

- Chapter 28Dokumen6 halamanChapter 28Shane Ivory ClaudioBelum ada peringkat

- Chapter 29Dokumen19 halamanChapter 29Darlianne Klyne BayerBelum ada peringkat

- Chapter 5 Property, Plant and Equipment GuideDokumen14 halamanChapter 5 Property, Plant and Equipment GuideNaSheeng100% (1)

- DepletionDokumen6 halamanDepletionjemjem14Belum ada peringkat

- Section 1 : Mastering Depreciation Testbank Solutions Depreciation On The Financial Statements V. Tax ReturnDokumen4 halamanSection 1 : Mastering Depreciation Testbank Solutions Depreciation On The Financial Statements V. Tax ReturnSamuel ferolinoBelum ada peringkat

- UntitledDokumen15 halamanUntitledemielyn lafortezaBelum ada peringkat

- Class Exercise CH 10Dokumen5 halamanClass Exercise CH 10Iftekhar AhmedBelum ada peringkat

- Ans. Basic Fin. AcctDokumen13 halamanAns. Basic Fin. AcctHashimRazaBelum ada peringkat

- PPE2-sample - Debi Comia PPE2-sample - Debi ComiaDokumen16 halamanPPE2-sample - Debi Comia PPE2-sample - Debi ComiaAngelica Pagaduan50% (2)

- Group 1Dokumen11 halamanGroup 1Cherie Soriano AnanayoBelum ada peringkat

- For Reg 1Dokumen7 halamanFor Reg 1Shynne MabantaBelum ada peringkat

- 93 - Final Preaboard AFAR SolutionsDokumen11 halaman93 - Final Preaboard AFAR SolutionsLeiBelum ada peringkat

- Assignment - Service Cost AllocationDokumen4 halamanAssignment - Service Cost AllocationRoselyn LumbaoBelum ada peringkat

- Answers - Chapter 1 Vol 2 2009Dokumen10 halamanAnswers - Chapter 1 Vol 2 2009Shiela PilarBelum ada peringkat

- In Class File Chapter 11Dokumen17 halamanIn Class File Chapter 11kathleen fajardoBelum ada peringkat

- Chapter 11 Supplemental Questions: E11-3 (Depreciation Computations-SYD, DDB-Partial Periods)Dokumen9 halamanChapter 11 Supplemental Questions: E11-3 (Depreciation Computations-SYD, DDB-Partial Periods)Dyan Novia67% (3)

- Module 3 DepreciationDokumen4 halamanModule 3 DepreciationLouie Jay JadraqueBelum ada peringkat

- Q3a. Capital Budget AssignmentDokumen1 halamanQ3a. Capital Budget AssignmentMorgan MunyoroBelum ada peringkat

- Financial Accounting Baysa and Lupisan 2008 Volume 2 EditionDokumen21 halamanFinancial Accounting Baysa and Lupisan 2008 Volume 2 EditionAsfjaslkf Dsgsdhsd0% (2)

- Depreciation AnswersDokumen22 halamanDepreciation AnswersGabrielle Joshebed Abarico100% (1)

- Depreciation AnswersDokumen13 halamanDepreciation AnswersGabrielle Joshebed Abarico100% (2)

- AFAR First Preboard 93 - SolutionsDokumen12 halamanAFAR First Preboard 93 - SolutionsEpfie SanchesBelum ada peringkat

- ACCT105 Quiz 11 - Depreciation calculationsDokumen8 halamanACCT105 Quiz 11 - Depreciation calculationsAway To PonderBelum ada peringkat

- Business Combi CH 6 de JesusDokumen9 halamanBusiness Combi CH 6 de JesusMerel Rose FloresBelum ada peringkat

- Cost accounting analysisDokumen14 halamanCost accounting analysismanasa k pBelum ada peringkat

- FinalDokumen6 halamanFinalRoronoa ZoroBelum ada peringkat

- Solutions to Depreciation ExercisesDokumen38 halamanSolutions to Depreciation ExercisesHira Farooq100% (1)

- FM Paper Solution (2012)Dokumen6 halamanFM Paper Solution (2012)Prreeti ShroffBelum ada peringkat

- A) Calculate The Straight-Line Depreciation. (Straight-Line Method)Dokumen3 halamanA) Calculate The Straight-Line Depreciation. (Straight-Line Method)VIKRAM KUMARBelum ada peringkat

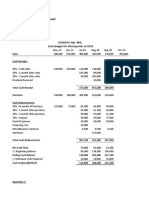

- Ritz-Carlton Monthly Cash Budget AnalysisDokumen6 halamanRitz-Carlton Monthly Cash Budget AnalysisAnsuman MohapatroBelum ada peringkat

- Problem 27 5Dokumen20 halamanProblem 27 5Cjezerei Dangue VerdaderoBelum ada peringkat

- Test 1 (2019672728) (NBF2D)Dokumen5 halamanTest 1 (2019672728) (NBF2D)Masnur Aina Md RajehBelum ada peringkat

- CVP Solutions and ExercisesDokumen8 halamanCVP Solutions and ExercisesGizachew NadewBelum ada peringkat

- Solution Set - Costing & O.R.-4th EditionDokumen417 halamanSolution Set - Costing & O.R.-4th EditionRonny Roy50% (4)

- Chapter 29Dokumen6 halamanChapter 29Shane Ivory ClaudioBelum ada peringkat

- DepreciationDokumen14 halamanDepreciationKris Hazel RentonBelum ada peringkat

- Chapter 27Dokumen12 halamanChapter 27Crizel DarioBelum ada peringkat

- CHAP 29gDokumen17 halamanCHAP 29gYen YenBelum ada peringkat

- Group 1Dokumen9 halamanGroup 1Cherie Soriano AnanayoBelum ada peringkat

- Functional Budgets GuideDokumen14 halamanFunctional Budgets Guidelinh nguyễnBelum ada peringkat

- Personal ProfileDokumen13 halamanPersonal ProfileKristine Lei Del MundoBelum ada peringkat

- Depreciation ExercisesDokumen21 halamanDepreciation Exercisesgiezele ballatan100% (2)

- Depreciation Schedules and Asset Impairment CalculationsDokumen8 halamanDepreciation Schedules and Asset Impairment CalculationsRehab ElsamnyBelum ada peringkat

- F.A. - Robles Empleo MC CH 1 2 3 4 5 6 7 8 9Dokumen12 halamanF.A. - Robles Empleo MC CH 1 2 3 4 5 6 7 8 9Carlyn Joy Paculba67% (9)

- COST MANAGEMENT AND FINANCIAL INFORMATIONDokumen7 halamanCOST MANAGEMENT AND FINANCIAL INFORMATIONSamuel DwumfourBelum ada peringkat

- Decesion MakingDokumen11 halamanDecesion MakingShoaib NaeemBelum ada peringkat

- Property, Plant and Equipment DepreciationDokumen13 halamanProperty, Plant and Equipment DepreciationJannelle SalacBelum ada peringkat

- Nahmias Chapter 3 SolutionsDokumen9 halamanNahmias Chapter 3 SolutionsDiego Andres Vasquez100% (1)

- Libro 7.5 InglesDokumen14 halamanLibro 7.5 InglesChristopher StrongBelum ada peringkat

- Calculate breakeven point, target sales, and safety margin for contribution margin analysisDokumen5 halamanCalculate breakeven point, target sales, and safety margin for contribution margin analysisAbhijit AshBelum ada peringkat

- Solutions Ch07Dokumen15 halamanSolutions Ch07KyleBelum ada peringkat

- Intermediate Accounting Midterm Exam KeyDokumen10 halamanIntermediate Accounting Midterm Exam KeyRenalyn ParasBelum ada peringkat

- Engineers Precision Data Pocket ReferenceDari EverandEngineers Precision Data Pocket ReferencePenilaian: 3 dari 5 bintang3/5 (1)

- Advanced AutoCAD® 2017: Exercise WorkbookDari EverandAdvanced AutoCAD® 2017: Exercise WorkbookPenilaian: 1 dari 5 bintang1/5 (1)

- Production and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesDari EverandProduction and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesBelum ada peringkat

- Macro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsDari EverandMacro Economics: A Simplified Detailed Edition for Students Understanding Fundamentals of MacroeconomicsBelum ada peringkat

- Materials Science and Technology of Optical FabricationDari EverandMaterials Science and Technology of Optical FabricationBelum ada peringkat

- Prepayments & Other Current Assets: GL - SL ReconciliationDokumen3 halamanPrepayments & Other Current Assets: GL - SL ReconciliationAnn Kristine TrinidadBelum ada peringkat

- Drug StudyDokumen14 halamanDrug StudyAnn Kristine TrinidadBelum ada peringkat

- AcknowledgementsDokumen1 halamanAcknowledgementsAnn Kristine TrinidadBelum ada peringkat

- Ia ConDokumen1 halamanIa ConAnn Kristine TrinidadBelum ada peringkat

- List of Books in TvetDokumen51 halamanList of Books in TvetAdeline HoBelum ada peringkat

- Ngas Module Government AccountingDokumen11 halamanNgas Module Government AccountingAnn Kristine Trinidad50% (2)

- The Accounting Policies: Manual On The New Government Accounting System For Local Government UnitsDokumen1 halamanThe Accounting Policies: Manual On The New Government Accounting System For Local Government UnitsAnn Kristine TrinidadBelum ada peringkat

- Community Problem PrioritizationDokumen5 halamanCommunity Problem PrioritizationAnn Kristine TrinidadBelum ada peringkat

- Humanities 1Dokumen1 halamanHumanities 1Ann Kristine TrinidadBelum ada peringkat

- GovERNMENT MANDATED FUNCTIONSDokumen1 halamanGovERNMENT MANDATED FUNCTIONSAnn Kristine TrinidadBelum ada peringkat

- Research Paper About OJTDokumen12 halamanResearch Paper About OJTJane Katigbak67% (3)

- Trinidad, Ann Kristine A. /ac09301 Payroll Department: Timekeeping ClerkDokumen2 halamanTrinidad, Ann Kristine A. /ac09301 Payroll Department: Timekeeping ClerkAnn Kristine TrinidadBelum ada peringkat

- Chapter 1 - Scope-Def of TermsDokumen4 halamanChapter 1 - Scope-Def of TermsAnn Kristine TrinidadBelum ada peringkat

- Guide On The Audit of Procurement - 1st Update-December 2009Dokumen768 halamanGuide On The Audit of Procurement - 1st Update-December 2009Ann Kristine TrinidadBelum ada peringkat

- The Accounting Books, Records, Forms and ReportsDokumen1 halamanThe Accounting Books, Records, Forms and ReportsAnn Kristine TrinidadBelum ada peringkat

- Teaching Plan Fior English TutorialDokumen1 halamanTeaching Plan Fior English TutorialAnn Kristine TrinidadBelum ada peringkat

- Ant Grass Hopper StoryDokumen11 halamanAnt Grass Hopper StoryAnn Kristine Trinidad100% (1)

- Assessment TestDokumen2 halamanAssessment TestAnn Kristine TrinidadBelum ada peringkat

- Spelling Basic EnglishDokumen6 halamanSpelling Basic EnglishAnn Kristine TrinidadBelum ada peringkat

- 1 - Altsol - 6e, Spiceland 6e Chapter 1 SolutionDokumen3 halaman1 - Altsol - 6e, Spiceland 6e Chapter 1 Solutionmondew99Belum ada peringkat

- Statement BeginningsDokumen1 halamanStatement BeginningsAnn Kristine TrinidadBelum ada peringkat

- Children save fare sitting on parents' lapDokumen1 halamanChildren save fare sitting on parents' lapAnn Kristine TrinidadBelum ada peringkat

- Trinidad, Ann Kristine A. /ac09301 Payroll Department: Timekeeping ClerkDokumen2 halamanTrinidad, Ann Kristine A. /ac09301 Payroll Department: Timekeeping ClerkAnn Kristine TrinidadBelum ada peringkat

- Sing your heart out at The Voice of JPIADokumen2 halamanSing your heart out at The Voice of JPIAAnn Kristine TrinidadBelum ada peringkat

- Capital BudgetingDokumen120 halamanCapital BudgetingAnn Kristine Trinidad100% (1)

- Chapter 12 Relevant Costs For Decision Making Answer KeyDokumen6 halamanChapter 12 Relevant Costs For Decision Making Answer KeyfrankmarsonBelum ada peringkat

- Sacrilege and Scandal in "SoledadDokumen1 halamanSacrilege and Scandal in "SoledadAnn Kristine TrinidadBelum ada peringkat

- PSAE-3000 Assurance Engagements Other Than Audits and Review of Historical Fin InfoDokumen23 halamanPSAE-3000 Assurance Engagements Other Than Audits and Review of Historical Fin InfocolleenyuBelum ada peringkat

- Republic Vs AcojeDokumen3 halamanRepublic Vs AcojeAnn Kristine TrinidadBelum ada peringkat

- MGRL Practice 2 ModDokumen20 halamanMGRL Practice 2 ModAnn Kristine TrinidadBelum ada peringkat

- Chapter 5 HW SolutionsDokumen39 halamanChapter 5 HW SolutionsemailericBelum ada peringkat

- Annamalai University: Directorate of Distance EducationDokumen314 halamanAnnamalai University: Directorate of Distance EducationMALU_BOBBYBelum ada peringkat

- QuestionsDokumen12 halamanQuestionsNaveen ChaudharyBelum ada peringkat

- Photographic LaboratoriesDokumen5 halamanPhotographic LaboratoriesJosann WelchBelum ada peringkat

- Cma August 2013 SolutionDokumen66 halamanCma August 2013 Solutionফকির তাজুল ইসলামBelum ada peringkat

- SPSC Lecturer Test CommerceDokumen3 halamanSPSC Lecturer Test CommerceDildar Raza100% (1)

- Equity Valuation.Dokumen70 halamanEquity Valuation.prashant1889Belum ada peringkat

- 5207871Dokumen87 halaman5207871sfrhBelum ada peringkat

- DSWD-NCR Audit Program PpeDokumen3 halamanDSWD-NCR Audit Program PpeAnn MarinBelum ada peringkat

- Accounting ExerciseDokumen6 halamanAccounting Exercisenourhan hegazyBelum ada peringkat

- Finance ManualDokumen240 halamanFinance ManualUciSusilawatiBelum ada peringkat

- May 2015 Skills PDFDokumen165 halamanMay 2015 Skills PDFOnaderu Oluwagbenga EnochBelum ada peringkat

- Accounting Standard 6 - DepreciationDokumen34 halamanAccounting Standard 6 - DepreciationSarthak Gupta100% (2)

- Investment in Human Capital: A Theoretical Analysis of Returns to EducationDokumen42 halamanInvestment in Human Capital: A Theoretical Analysis of Returns to EducationAnonymous 4Jp8sAZD7Belum ada peringkat

- Cash Flow or EBITDA - Can't We Have BothDokumen9 halamanCash Flow or EBITDA - Can't We Have Bothmagc69Belum ada peringkat

- Topic 4 - Adjusting Accounts and Preparing Financial StatementsDokumen18 halamanTopic 4 - Adjusting Accounts and Preparing Financial Statementsapi-388504348100% (1)

- Planning New Magic at DisneyDokumen9 halamanPlanning New Magic at Disneyjfrz44Belum ada peringkat

- Airtel - Fixed Asset Management StudyDokumen39 halamanAirtel - Fixed Asset Management StudyMr SmartBelum ada peringkat

- Introduction to Financial Accounting Chapter on DepreciationDokumen61 halamanIntroduction to Financial Accounting Chapter on DepreciationAlty StelleBelum ada peringkat

- FDNACCT C35A Group Project Group 3Dokumen21 halamanFDNACCT C35A Group Project Group 3cBelum ada peringkat

- Customs Duty SynopsisDokumen29 halamanCustoms Duty SynopsisAmrit NeupaneBelum ada peringkat

- Hampton Machine Tool CoDokumen13 halamanHampton Machine Tool CoArdi del Rosario100% (12)

- GL PL Code ChartDokumen12 halamanGL PL Code ChartengrlumanBelum ada peringkat

- Chapter 13-A Regular Allowable Itemized DeductionsDokumen13 halamanChapter 13-A Regular Allowable Itemized DeductionsGeriel FajardoBelum ada peringkat

- ACCA F7 Financial Reporting Mock Exam Questions 1Dokumen16 halamanACCA F7 Financial Reporting Mock Exam Questions 1Ernest75% (4)

- IT Audit Exercise WorkbookDokumen46 halamanIT Audit Exercise WorkbookJulie TungculBelum ada peringkat

- DrillsDokumen4 halamanDrillsKRISTINA DENISSE SAN JOSEBelum ada peringkat

- Ipsas 1 and Ipsas 2Dokumen6 halamanIpsas 1 and Ipsas 2Esther AkpanBelum ada peringkat

- Capital Budgeting Techniques and Project Risk AnalysisDokumen3 halamanCapital Budgeting Techniques and Project Risk AnalysisbalachmalikBelum ada peringkat

- Chapter 2 Financial Statement, Taxes - Cash Flow - Student VersionDokumen4 halamanChapter 2 Financial Statement, Taxes - Cash Flow - Student VersionNga PhamBelum ada peringkat