Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Risk-Neutral Skewness - Evidence From Stock OptionsDokumen24 halamanRisk-Neutral Skewness - Evidence From Stock OptionsdbjnBelum ada peringkat

- Smiles, Bid-Ask Spreads and Option PricingDokumen24 halamanSmiles, Bid-Ask Spreads and Option PricingdbjnBelum ada peringkat

- Extra Credit Fall '12Dokumen4 halamanExtra Credit Fall '12dbjnBelum ada peringkat

- Option Hapiness and LiquidityDokumen53 halamanOption Hapiness and LiquiditydbjnBelum ada peringkat

- Introduction To Variance SwapsDokumen6 halamanIntroduction To Variance Swapsdbjn100% (1)

- Dynamics of Implied Volatility SurfacesDokumen16 halamanDynamics of Implied Volatility SurfacesdbjnBelum ada peringkat

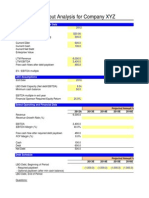

- Quick LBO ModelDokumen10 halamanQuick LBO ModeldbjnBelum ada peringkat

- Final Exam Fall '12Dokumen7 halamanFinal Exam Fall '12dbjnBelum ada peringkat

- Brealey. Myers. Allen Chapter 17 TestDokumen13 halamanBrealey. Myers. Allen Chapter 17 TestMarcelo Birolli100% (2)

- Chap 006Dokumen95 halamanChap 006dbjnBelum ada peringkat

- Of Smiles and SmirksDokumen30 halamanOf Smiles and SmirksdbjnBelum ada peringkat

- Chap 002Dokumen75 halamanChap 002dbjnBelum ada peringkat

- BMA 20 8eDokumen11 halamanBMA 20 8edbjnBelum ada peringkat

- BMA TB 33 8eDokumen8 halamanBMA TB 33 8edbjnBelum ada peringkat

- On The Properties of Equally-Weighted Risk Contributions PortfoliosDokumen23 halamanOn The Properties of Equally-Weighted Risk Contributions PortfoliosdbjnBelum ada peringkat

- Chap 011Dokumen81 halamanChap 011dbjnBelum ada peringkat

- Annual Report 2011 Current OPECDokumen65 halamanAnnual Report 2011 Current OPECdbjnBelum ada peringkat

- 2013 World Economic Situation and ProspectsDokumen37 halaman2013 World Economic Situation and ProspectsdbjnBelum ada peringkat

- Chap 021Dokumen122 halamanChap 021dbjnBelum ada peringkat

- Answer Key QuizDokumen4 halamanAnswer Key QuizdbjnBelum ada peringkat

- Bloomberg ExcelDokumen52 halamanBloomberg Exceldbjn100% (2)

- Erc SlidesDokumen56 halamanErc SlidesdbjnBelum ada peringkat

- Excel Short CutsDokumen42 halamanExcel Short CutsdbjnBelum ada peringkat

- Acadian Portfolio RiskDokumen14 halamanAcadian Portfolio RiskdbjnBelum ada peringkat

- Chap 019Dokumen11 halamanChap 019dbjnBelum ada peringkat

- Chap 018Dokumen19 halamanChap 018dbjnBelum ada peringkat

- Spiceland IA 6e Excel GuideDokumen31 halamanSpiceland IA 6e Excel Guidemondew99Belum ada peringkat

- Chap 020Dokumen10 halamanChap 020dbjnBelum ada peringkat

- Chap 021Dokumen18 halamanChap 021dbjnBelum ada peringkat

- Chap 013Dokumen8 halamanChap 013dbjnBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- United Wholesale Mortgage, Llc's Motion To Dismiss America's Moneyline, Inc.'s Amended CounterclaimDokumen79 halamanUnited Wholesale Mortgage, Llc's Motion To Dismiss America's Moneyline, Inc.'s Amended CounterclaimMatias SmithBelum ada peringkat

- CV Kleber HerreraDokumen10 halamanCV Kleber HerreraGaby Vaca PitaBelum ada peringkat

- Certificate Cum Policy Schedule: MOTOR 2 WHEELER (PACKAGE POLICY) - UIN NO. IRDAN137RP0017V01200809 - SAC Code. 997134Dokumen1 halamanCertificate Cum Policy Schedule: MOTOR 2 WHEELER (PACKAGE POLICY) - UIN NO. IRDAN137RP0017V01200809 - SAC Code. 997134Rohit YadavBelum ada peringkat

- Universitas Bina Nusantara: Catering)Dokumen2 halamanUniversitas Bina Nusantara: Catering)Aldo PutraBelum ada peringkat

- India Discovers $410 Billion Lithium DepositDokumen9 halamanIndia Discovers $410 Billion Lithium DepositELC2024-ABelum ada peringkat

- The Role of Law in Business DevelopmentDokumen4 halamanThe Role of Law in Business DevelopmentPsy GannavaramBelum ada peringkat

- Module 7: Making The System WorkDokumen18 halamanModule 7: Making The System WorkshukkurBelum ada peringkat

- Chatting Format 1Dokumen13 halamanChatting Format 1Wilfred Freddy100% (4)

- Business Law and Practice (Skills) : Workshop 9 Task 1 - ExemplarDokumen2 halamanBusiness Law and Practice (Skills) : Workshop 9 Task 1 - ExemplarRo LondonBelum ada peringkat

- Questionnaire of A SurveyDokumen3 halamanQuestionnaire of A Surveynur naher muktaBelum ada peringkat

- HNB Report-2Dokumen37 halamanHNB Report-2Samith GurusingheBelum ada peringkat

- Application of Demand and SupplyDokumen4 halamanApplication of Demand and SupplyFahad RadiamodaBelum ada peringkat

- Analisis Pengaruh Atribut Produk Terhadap Keputusan Pembelian Motor Suzuki Smash Di Kota Semarang Part-1Dokumen10 halamanAnalisis Pengaruh Atribut Produk Terhadap Keputusan Pembelian Motor Suzuki Smash Di Kota Semarang Part-1Aji SetyobudiBelum ada peringkat

- Behavioral FinanceDokumen184 halamanBehavioral FinanceSatya ReddyBelum ada peringkat

- MAF Mixed and Yield Variances (Eng)Dokumen8 halamanMAF Mixed and Yield Variances (Eng)BirukBelum ada peringkat

- General Conditions: Insurance CancellationDokumen5 halamanGeneral Conditions: Insurance CancellationCodruta HiripanBelum ada peringkat

- Restaurant Marketing StrategyDokumen19 halamanRestaurant Marketing StrategyEmily MathewBelum ada peringkat

- Masterclass 3.2Dokumen6 halamanMasterclass 3.2Amit PrasadBelum ada peringkat

- ABSLI Multiplier FundDokumen1 halamanABSLI Multiplier FundTanveer AhmadBelum ada peringkat

- JLPT Application Form Method-July 2024Dokumen4 halamanJLPT Application Form Method-July 2024Sanjyot KolekarBelum ada peringkat

- SAG 23 Heavy-Duty Vehicle Weight Restrictions in The EUDokumen28 halamanSAG 23 Heavy-Duty Vehicle Weight Restrictions in The EUAliBelum ada peringkat

- Global SME Finance Facility Progress Report 2012 2015Dokumen42 halamanGlobal SME Finance Facility Progress Report 2012 2015Aarajita ParinBelum ada peringkat

- TPA Refund ProcessDokumen3 halamanTPA Refund ProcessYuan TianBelum ada peringkat

- Warehouse and Inventory Management: UNIT-1Dokumen29 halamanWarehouse and Inventory Management: UNIT-1Amitrajeet kumarBelum ada peringkat

- Berzanski Indeksi U Realnom Sektoru EkonomijeDokumen131 halamanBerzanski Indeksi U Realnom Sektoru EkonomijeMasal MiroslavBelum ada peringkat

- Monsoon Sim Data Presentation and AnalysisDokumen16 halamanMonsoon Sim Data Presentation and AnalysisMa. Eunice CajesBelum ada peringkat

- Module 2 - Audit Planning Risk-Based AuditDokumen10 halamanModule 2 - Audit Planning Risk-Based AuditCha DumpyBelum ada peringkat

- Global Migration: Amayna, Arabello, Basilio, Gabio, Marco, RonquilloDokumen15 halamanGlobal Migration: Amayna, Arabello, Basilio, Gabio, Marco, RonquilloBrian Angelo Montalvo BasilioBelum ada peringkat

- Tradersworld: Don't Let Faulty Assumptions Sabotage Your Trading CareerDokumen117 halamanTradersworld: Don't Let Faulty Assumptions Sabotage Your Trading CareerMichael RomeroBelum ada peringkat

- Evaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiDokumen12 halamanEvaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiRoshanBelum ada peringkat