Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- 0132067331Dokumen47 halaman0132067331Hoàng HuyBelum ada peringkat

- BUS 415 Investment and Portfolio Management Spring 2011, AUBG Quiz #6 (A)Dokumen3 halamanBUS 415 Investment and Portfolio Management Spring 2011, AUBG Quiz #6 (A)Hoàng HuyBelum ada peringkat

- CH 01Dokumen4 halamanCH 01Hoàng HuyBelum ada peringkat

- CH 14Dokumen4 halamanCH 14Hoàng HuyBelum ada peringkat

- Chapter 2 Problem SolutionsDokumen5 halamanChapter 2 Problem SolutionsHoàng HuyBelum ada peringkat

- Ch003.Lam2e TBDokumen25 halamanCh003.Lam2e TBHoàng HuyBelum ada peringkat

- Chap 3 SolutionsDokumen70 halamanChap 3 SolutionsHoàng Huy80% (10)

- 157957Dokumen18 halaman157957Hoàng Huy0% (1)

- Chapter 3 Exercise SolutionsDokumen14 halamanChapter 3 Exercise SolutionsHoàng HuyBelum ada peringkat

- Introduction To MicroeconomicsDokumen13 halamanIntroduction To MicroeconomicsHoàng HuyBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Hills, Hutman, Et Miles, 2008, The Evolution and Development of Entrepreneurial MarketingDokumen14 halamanHills, Hutman, Et Miles, 2008, The Evolution and Development of Entrepreneurial MarketingMaalejBelum ada peringkat

- Dividend Policy: Answers To QuestionsDokumen10 halamanDividend Policy: Answers To QuestionsLee JBelum ada peringkat

- FM09-CH 17Dokumen5 halamanFM09-CH 17Mukul KadyanBelum ada peringkat

- 3 Departmental AccountsDokumen13 halaman3 Departmental AccountsJayesh VyasBelum ada peringkat

- (Solved) Lombard Company Is Contemplating The PurDokumen5 halaman(Solved) Lombard Company Is Contemplating The PurFahmi Ilham Akbar0% (1)

- CBOE S&P 500 2% OTM BuyWrite Index (BXY) Micro SiteDokumen4 halamanCBOE S&P 500 2% OTM BuyWrite Index (BXY) Micro SiteALBelum ada peringkat

- Agency, Trust and Partnership - Course OutlineDokumen9 halamanAgency, Trust and Partnership - Course OutlineKhay GonzalesBelum ada peringkat

- Account 1Dokumen3 halamanAccount 1Harshal JadhavBelum ada peringkat

- Fundamental Forces of Change in Banking 2869Dokumen50 halamanFundamental Forces of Change in Banking 2869Pankaj_Kuamr_3748Belum ada peringkat

- Trading Blueprint EbookDokumen6 halamanTrading Blueprint EbookJohn Atox Petrucci100% (4)

- Jesse Lauriston LivermoreDokumen4 halamanJesse Lauriston LivermoreJoseph JofreeBelum ada peringkat

- Business PlanDokumen3 halamanBusiness PlanGenevieve BarengBelum ada peringkat

- SynopsisFormat Antra PitchDokumen2 halamanSynopsisFormat Antra PitchKavit ThakkarBelum ada peringkat

- Investment QuestionnaireDokumen6 halamanInvestment QuestionnaireChristieBelum ada peringkat

- Trial BalanceDokumen1 halamanTrial BalancePUSPA Ghalda ShafaBelum ada peringkat

- Ch05 Beams12ge SMDokumen22 halamanCh05 Beams12ge SMOmar HadeBelum ada peringkat

- Malaysia: Country M&A Team Country Leader Frances Po Khoo Chuan Keat Lim Yiek LeeDokumen18 halamanMalaysia: Country M&A Team Country Leader Frances Po Khoo Chuan Keat Lim Yiek LeeNabila SurayaBelum ada peringkat

- Asset Management Tactical QuarterlyDokumen19 halamanAsset Management Tactical QuarterlyDavid QuahBelum ada peringkat

- Financial-Ratios Q'sDokumen8 halamanFinancial-Ratios Q'szesrtyryytshrtBelum ada peringkat

- Nifty OAT V.10 OCT - XLSMDokumen34 halamanNifty OAT V.10 OCT - XLSMKalpesh ShahBelum ada peringkat

- Michael Burry Op-Ed Contributor - I Saw The Crisis Coming. Why Didn't The FedDokumen3 halamanMichael Burry Op-Ed Contributor - I Saw The Crisis Coming. Why Didn't The FedArthur O'KeefeBelum ada peringkat

- Investing Terms PDFDokumen5 halamanInvesting Terms PDFdavidiazhaoBelum ada peringkat

- Volpips Accademy ™...Dokumen12 halamanVolpips Accademy ™...Sanal V VBelum ada peringkat

- Overview of Financial SystemDokumen50 halamanOverview of Financial SystemshahyashrBelum ada peringkat

- Chapter 4 BondDokumen60 halamanChapter 4 BondSRAR Nurul HudaBelum ada peringkat

- (Kotak) Reliance Industries, October 29, 2023Dokumen36 halaman(Kotak) Reliance Industries, October 29, 2023Naushil ShahBelum ada peringkat

- Lecture 5 InterestRateFutures (Part1)Dokumen36 halamanLecture 5 InterestRateFutures (Part1)efflux 1990Belum ada peringkat

- Chapter 3 Financial InstrumentsDokumen64 halamanChapter 3 Financial InstrumentsCyryll PayumoBelum ada peringkat

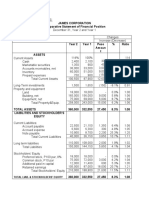

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDokumen7 halamanHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananBelum ada peringkat

- Cop - Chap 13-15Dokumen6 halamanCop - Chap 13-15Estrella RoseteBelum ada peringkat