BOOK - 32 Ways To Stop Foreclosure

Diunggah oleh

TRISTARUSAJudul Asli

Hak Cipta

Format Tersedia

Bagikan dokumen Ini

Apakah menurut Anda dokumen ini bermanfaat?

Apakah konten ini tidak pantas?

Laporkan Dokumen IniHak Cipta:

Format Tersedia

BOOK - 32 Ways To Stop Foreclosure

Diunggah oleh

TRISTARUSAHak Cipta:

Format Tersedia

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

32 Ways to Quickly Stop Foreclosure a Complete Course for Homeowners

by Dave Dinkel

How To Gain Back Control Of Your Personal Finances By Putting The Brakes On All Those People And Institutions Who Want To Take Your Home And Make Money Off Your Personal Financial Hardship.

Included are FIVE Special Bonus Reports:

Bonus Report #1 - Making Money with Your Home, Even if You Lose It Bonus Report #2 - Getting Your Home back at 50% to 90% of Loan Value Bonus Report #3 - Secrets of Lease Options for Homeowners Bonus Report #4 Buying a Home (Possibly Yours) at the Foreclosure Auction Bonus Report #5 - Do-It-Yourself Credit Repair for Homeowners

-132 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

-WARNINGIf you havent been contacted by a horde of investors, realtors, investors disguised as professionals who want to help you keep your home, lenders, attorneys, mortgage brokers, and even outright scam artists, - YOU WILL BE SHORTLY! A few of these individuals could possibly have a product or service that may make sense to your financial well-being but these are FEW and FAR BETWEEN. For your sake, trust no one! Read this Manual so you are informed of what choices you have and specifically, what options no one else will tell you!

We STRONGLY suggest you DO NOT SIGN ANYTHING, unless your attorney reviews it first.

We always ask homeowners we work with to give us their incoming correspondence so we can review it. At least 25% - 50% of these letters, postcards and other written documents contain Fraudulent Information, because the industry is almost entirely unregulated!

Do not let yourself be duped into making a decision that you cant change.

The single worst enemy you face is PROCRASTINATION! If you hesitate or are indecisive, you will likely lose your home to foreclosure. To save your home or to stall for time to sell it at the highest possible price you will need to take action and do so immediately. Frankly, it is very therapeutic to KEEP MOVING toward a resolution in what can be a very depressing situation. Take charge of your life today by first printing this text so you can read it as soon as possible. The highlighted areas and colored print were placed here to stress their importance. You do not nee to print the text in color as you can print it in black to save on your color ink. Next, set aside quiet time to read this text and finally, keep yourself active daily by making a list of what needs to be done and, no matter how aggrieving, get the list completed each and every day. Whatever you dont want to do, you should do it FIRST!

-232 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

TABLE of CONTENTS

Cover Page Warning Table of Contents Introduction

CHAPTER 1 - Understanding the Foreclosure Process

Types of Liens Where Foreclosure Is Possible HOA Liens IRS Liens Mechanics Liens Tip #1 - Sub-contractor Payments Municipal Code Violation Liens Mortgages Tip #2 - Cost of Prepayment Types of Mortgages Tip #3 Accelerated Prepays Conventional Mortgages Adjustable Rate (ARMs) Second or Third Mortgages Home Equity Lines (HELOCs) Hard Money Loans Government Insured FHA HUD VA FHA HUD Reverse Mortgage (HECMs) Tip #4 Getting Good Faith Tip #5 Which to Pay? Judicial Foreclosure Tip #6 - Seconds are $$$ Makers Tip #7 - Partial Payments Non-solution Tip #8 - Behind Again and Out Tip #9 - Get it in Writing List of Mortgage and Deed of Trust States EXTREMELY IMPORTANT The Actual Process of Judicial Foreclosure Tip #10 - Dont Answer the Phone or Door Tip #11 - Summary Final Judgment Tip #12 - SCAM ALERT Beware at Hearing Possible Reasons for a Continuance Examples Not Acceptable for Continuance Tip #13 - Supervisor Interventions IMPORTANT NOTE How Long? Tip #14 - What is the Difference The Actual Process of Non-judicial Foreclosure Eviction What to Expect

CHAPTER 2 - Determining Your Ability to Keep Your Home

Tip #15 - Relapse Rate & Its Consequences Tip #16 - Single vs. Dual Contracting Sample Monthly Income and Expense Estimator Your Monthly Income and Expense Estimator Tip #17 - Special IRS Lien Treatment So What is Your Decision?

CHAPTER 3 - Determining The Amount of Equity in Your Home

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

PAGE 1 2 3 7 11 12 12 12 13 13 13 14 14 15 15 15 15 16 16 16 17 17 17 17 17 18 18 18 19 20 20 21 21 23 24 25 27 27 27 28 29 29 31 32 35 37 37 37 38 39 41 43 44

-3-

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009 The Majority of Foreclosures Are of Two Types 1.) Refinance and Cash Out 2.) Personal Crisis Extracting Your Homes Equity Minimal Equity Tip #18 - Deed in Lieu Of Foreclosure or Not Some Equity Large Equity 45 44 45 47 47 47 48 48 50 51 51 52 52 53 53 53 55

CHAPTER 4 - Understanding Your Mortgage

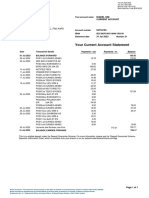

Tip #19 - Seller Financing Do You Have a Mortgage or a Deed of Trust? Important Features of Deeds of Trust and Mortgages Your Monthly Mortgage Statement Tip #20 - ARMs, Resets, & Penalties Tip #21 - Same Lender Application Soft and Hard Prepayment Penalties Types of Ownership

CHAPTER 5 - Specific Methods of Stopping or Postponing Your Foreclosure

Tip #22 - SCAM ALERT I was at the courthouse Tip #23 - SCAM ALERT Deed Stripping Tip #24 - SCAM ALERT Contract Wrangling Tip #25 - SCAM ALERT Equity Rebate Summary of What Not to Do (Dont Dos) 32 Ways to Immediately Stop or Postpone Your Foreclosure Methods of Keeping Your Home #1 Friends and Family Tip #26 - Get Confirmation of Partial Tip #27 - Options for CDs #2 Stocks and Bonds #3 Second Home Financing #4 Home Equity Line at Your Bank #5 Home Equity Loan Other than Yours #6 Challenge Legality of the Foreclosure Docs #7 Forbearance Agreement IMPORTANT It Isnt Over Just Because You Signed #8 Small Second Mortgage Tip #28 - SCAM ALERT I can do it oops! #9 Refinance Delinquent Loan Consumer Alert! Reverse Me Out Tip #29 - How Not to Loan Shop #10 Outside Funding #11 Employer Advance #12 Liquidate Assets Tip #30 Ask Again and Again #13 Rent-a-Room(s) Tip #31 Guideline for Rooms #14 Rent Your Home #15 Only for FHA, HUD, and VA Loans WARNING Violation of Federal Law EXTREMELY IMPORTANT Rights under SCRA #16 Credit Cards Tip #32 - Quick Credit Score Boost #17 401-K Retirement Loan #18 Cash Value Life Insurance #19 Employer Hardship Advance 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

57 57 58 59 62 63 64 64 64 65 65 66 66 67 68 68 69 71 71 71 72 73 73 74 74 75 75 75 75 76 77 77 77 78 78 79 79 79

-4-

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009 Tip #33 Repeated Second for Insurance VERY IMPORTANT If Unemployed #20 Grant Money If You Have to Sell Your Home #1 Talk to Investors Tip #34 New Laws Effecting Your Rights Tip #35 Whose Name, Who is Responsible #2 Lease Option Tip #36 Avoid a Law Suit Tip #37 Court Hearing Exception #3 Sell Subject To Existing Mortgage(s) #4 Sell Your Home as a Wholesale/Retail #5 Sell as an Equity Split Tip #38 Splitting it Up #6 Sign a Sales Contract #7 Sell Using a Modified Auction Procedure #8 Short Sale Strategy #9 Combo of Strategies Tip #39 Investor Feeding Frenzy IMPORTANT Buyers Agent Only #10 File Chapter 13 Bankruptcy (or Not) EXTREMELY IMPORTANT Tip #40 - Bankruptcy vs. Foreclosure #11 Deed in Lieu of Foreclosure IMPORTANT NOTE Deed in Lieu vs. Foreclosure Hot, Hot, Hot Money Making Idea Tip #41 Asset Info That Will Come Back #12 Secret Method Not Disclosed Elsewhere Tip #42 - Repeated- HUGE SCAM Tip #43 How to Get Escrowed Funds Reviewing Your Escrow Options Beware Predatory Loans Tip #44 Negotiating With Investors Foreclosure in a Probate Another Word of Caution I have a buyer for Real Estate Investors Foreclosure Tip #45 - Double Your Advertising Tip #46 Appraisal Restriction In Summary Summary of Homeowner Strategies 79 80 80 80 80 81 81 81 81 82 82 83 84 84 85 85 85 86 86 87 87 88 89 89 90 91 91 91 93 93 94 95 93 96 97 98 99 99 100 102 103 116 116 117 118 118 119 119 119 120 120 121 121 122 123

CHAPTER 6 - Quick Start Check List to End Your Foreclosure BONUS Report #1 - TOP SECRET 12 Ways to Make Money From Your

Foreclosure, Even if You Already Lost Your Home Twelve Ways to Make Money Even If You Lose Your Home 1. Investor Abuse Super Powerful Information - Statute of Limitations 2. Loan Reinstatement 3. Predatory Lending Practices 4. Elder Abuse 5. Right of Redemption 6. Overage Tip #47 Illegal Actions for Overage Tip #48 - SCAM ALERT Worthless Deed? 7. Money Opportunity at the Auction 8. Get Rid of Nagging Junior Liens 9. Sell Everything 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

-5-

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009 10. 11. 12. Victims Funds Judgment vs. 1099 IRS Workout UNIQUE OPPORTUNITY Renter Buys 123 123 124 124 126 126 128 129 131 137 138 138 139 139 140 140

BONUS Report #2 - TOP SECRET - How to Get Your Home Back at

50% to 90% of Loan Value Tip #49 - SCAM ALERT Some Lease Options Tip #50 Extinguish vs. Transfer Tip #51 Larger Discount Request What You Can Expect to Supply to the Lender

BONUS Report #3 - TOP SECRET - Secrets Homeowners Should Know

About Lease Options Two Ways to Keep Your Home Using Lease Options Lease Option Out Tip #52 Special Signage VERY IMPORTANT Option Consideration Lease Option Yourself Tip #53 One vs. Two Agreements

BONUS Report #4 - TOP SECRET - Buying Your Home Back at the

Foreclosure Auction Tip #54 Finding a Buyer Tip #55 Redemptive Rights Tip #56 Stick to it Pricing 141 142 144 146

BONUS Report #5 - TOP SECRET - Do-It-Yourself Credit Repair

for Homeowners Tip #57 How long Bankruptcy - NOT 10 Years Getting Started Tip #58 FRAUD ALERT Tip #59 Exceptions to One Free Report Tip #60 Cost for Mortgage Broker to Pull Tip #61 - Reporting Identity Theft How the Credit Scoring System Works 42 Ways to Improve Your Credit Score or Get Payback Tip #62 Medical Bill Minimal Repay Tip #63 Divorce and Credit Issues General Information on Codes The Bankruptcy Myth US Department of Housing and Urban Development Foreclosure Information General and Earnings Disclaimers General Disclosures GLOSSARY 147 148 149 150 152 152 152 153 154 158 161 162 164 167 177 178 179

-632 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

Introduction

Congratulations on purchasing this book and taking the first step to resolving your foreclosure. You are to be commended for taking control of your situation and not falling into the foreclosure trap that over Two Million homeowners will experience in the next several years. We have found the knowledge in this text, combined with immediate action on your part, will achieve the goal of getting a foreclosure stopped or postponed very quickly sometimes within 24 hours. The not so obvious benefit of stopping your foreclosure is to keep your credit score as intact as possible and get you into a credit repair mode for the future. Your credit score dictates how much your insurance rates will be, your ability to get a job, and more obviously, how much interest you will pay on consumer loans. A single percentage point of higher interest rates on these loans will easily become tens of thousands of extra dollars you will have to pay in the future. The material in this text and a soon-to-be sister book should help to improve your credit score. This book contains everything to take you through all the methods that are used conventionally and many underground but legal methods of stopping foreclosure and possibly profiting from your foreclosure - if it does happen. You will be learning secret tips and tricks that investors, lenders, mortgage brokers, and even attorneys will not tell you. They wont tell you because it is not in their best interest since they wont be able to steal your home at a ridiculous price, charge you exorbitant fees, or make huge chunks of YOUR money that YOU should be making. As soon as possible print this text and start reading it so you get a head start on taking appropriate action to save your home. It also contains 80 tips, hints and scam notifications that will help you make your journey easier and reveal useful information that you can use in the future. Included is Bonus Report #1 which details twelve methods of making money even if you lose your home to foreclosure and since the statute of limitations is as much as seven years in some states, you can use these techniques to possibly get back some of your lost money or equity from your foreclosure. Foreclosure is the result of a homeowner not being able to pay his mortgage or in more and more cases, not wanting to pay his mortgage. It usually starts because of a job loss; disability income loss; divorce;

-732 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

death of a wage earner; serious illness of a family member and the resultant medical bills; or in the growing trend in the United States, because the homeowner re-financed with the intention of cashing out his equity and never making any further mortgage payments. Whichever situation caused you to stop making your mortgage payments, or if you are contemplating not making your mortgage payments, we have solutions for you! Foreclosure is a great travesty and a true blight on todays society that results in the breakup of families, horrendous financial loss, and continuing financial costs because of credit damage to the foreclosure victim. The foreclosure victims credit has been first damaged because of his late payments and if a foreclosure results, the victim will have his credit score impacted for years to come. The lower a persons credit score, the higher the interest rate charged on all future items he finances. The lower the credit score, the greater the reason for a lender to make a windfall profit on the same loan they would have financed otherwise at a lower rate because most large loans are collateralized by major items (i.e. homes, automobiles, boats, etc.). The goal of this text is to help homeowners to either save their homes or, if absolutely necessary, to get the most possible equity out of their homes if they are forced to leave. The strategies you will see work for homeowners who have little or no equity, some equity (10% - 15%), and large amounts of equity (15%+) in essence, everyone facing or already in foreclosure. Our intent with this book is to do what is best for you, the homeowner, and you should be forewarned that we will be stepping on the toes of investors, realtors, lenders, and attorneys because their interests are often times to make money off your personal crisis. It is just a business decision to them and you are just a product to make money for them. Am I being harsh on realtors, lenders, attorneys and investors? No, because it is the truth! If you arent going to make them money, they have no altruistic goal of helping you. Frankly, you are at the bottom of the food chain and some of these individuals are the sharks looking to take chunks of money from your property. However, we will show you how they can help in certain situations and how to work the investors to your advantage as options of last resort. They do have their place, you just need to be informed about how to handle them you must take control of your situation and we will show you how.

-832 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

We will also be discussing various scams and near-scams that you will be hearing or seeing from various professionals. While we have seen numerous ones, one of the most offensive ploys is having an investor pose as a Consultant and having you pay him $900 $1,300 to fill out a lender form called a Reinstatement Request, or a Forbearance Agreement. You can fill this form out yourself or if you need help, get an attorney to help for 1/2 to 1/3 of the investors (Consultants) fee! With an attorney you have malpractice insurance to go back to if he does it wrong. With an investor you have little recourse other than a civil suit unless your state has specific laws against this practice and a growing number of states are passing these regulations because of investor abuse of homeowners in foreclosure. The above documents are legally binding obligations and should be filled out by an attorney not a person portraying themselves as a professional or expert. Since 1975 we and our associates have worked with literally thousands of homeowners to help solve their pending foreclosures. In most cases we have been able to either help the homeowners get as much equity out of their property as possible if they had to leave, or help them stay in the property if they could afford to stay. These homeowners are mostly honest people, who about 95% of the time, want desperately to stay in their homes and continue their life. This is not much to ask, but once the lender files a foreclosure notice with the courts, their pending foreclosure becomes public record and the hungry sharks will start sending you mailings, calling you using sophisticated telephone scripts, and even start knocking at your door almost immediately to get there before their competition (other investors, mortgage brokers, attorneys, realtors, etc.). We dont work with foreclosure victims unless our proposed solution is a win-win for all parties (the homeowner, us, and the lender) involved. Ironically, some times, because of the resale of loans, the lender involved has made accounting mistakes and the resolution is as simple as showing the lender the problem. So after 32+ years investing in real estate, we thought we had seen most everything, but we are often shocked by the material we see mailed to homeowners and the statements and promises some greedy individuals make to homeowners in their worst time of need.

-932 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

To the best of our knowledge, the text you are about to read reveals some secrets of the real estate and banking industries that have never been revealed to the public. Again, we are focused on helping you either keep your home, or getting you as much equity out as quickly as possible if you have to leave. We will also show you how to determine if you can afford to own your home because you need to take this into account when making your decision about staying or leaving. Unlike any book, text, or individual that we have read, interviewed, or been involved with, we will disclose the Best Kept Secrets of real estate investors a way you may still be able to make money on your home - even if you have already lost it to foreclosure! To our knowledge, no one has ever disclosed this information to the public and especially to the foreclosure victims. We do know that some investors have used these techniques to get equity from a property that was due to homeowners who didnt know they had money coming or how to get these funds. You will learn how to do exactly this in this text! The most important thing that you can grasp, and do so IMMEDIATELY, is that your foreclosure is TIME SENSITIVE! The longer you wait to get started, the fewer options you have available. You have many options available to get money out of your home, AND even if you lose your property or HAVE ALREADY LOST IT, you may have as many as ten possible ways to still make money or save on potential liabilities (see Chapter 6). HOWEVER, if you want to stay in your home you must get started NOW. Start by reading this Manual completely, except for parts that do not apply to your situation, and start taking action to make your plan as quickly as possible. Everything you should need to start is in this Manual and has been consolidated into lists for your convenience and ease of use. The hints and tips are strategically located in the text after an important related topic. The biggest misconception foreclosure victims have is that they will have to pay off their entire mortgage to stay in their home. This is very rarely true, so we will be focusing on the ways to keep you in your property that are the best for you. Please read this text in its entirety before you start assuming any path to take.

- 10 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

Chapter 1

Understanding the Foreclosure Process

Even though you may already be involved, or you are just contemplating getting into the foreclosure process, it is important that no matter how much you think you know about the foreclosure process, you should read this chapter so you completely understand the fundamentals of how the system works. This will help answer questions that you may not know exist now and that you may not have realized before you lost your home. Stick to it and read everything in this text, unless it is obvious that it doesnt pertain to you. Specifically, any of the 32 methods of stopping or delaying your foreclosure and the type of foreclosure process that affects you - judicial, non-judicial, or any other foreclosure process your state uses. Lets get over this issue right now whether you believe your lender or mortgage broker misled you or defrauded you, it is the courts who will have to decide that issue. Ask Legal Aid Services in your community about how you can take action against the company or individuals that got you your mortgage. The lender agent gave you a contract which you signed in at least duplicate, and it falls under what is called Contract Law. This means if it is in writing in the contract, and the contract is legal under the law of your state, it is the law. It is wasted effort to vent your anger on either the mortgage broker or the lender at this time. There may be a time and a place to do this and we will discuss it later. Focus ENTIRELY on resolution of your foreclosure or you will lose your home. Lets first review the foreclosure process and where you fit in it. Foreclosure is the legal process of a lender taking legal action to claim a property which has a lien (mortgage or deed of trust) against it that was issued by the lender, but which is currently in default. The process is regulated by the state in which the property is located and administered by the county but varies depending on which type of legal jurisdiction the State has chosen either you live in a Mortgage State, a Deed of Trust State, or a state that uses a combination of both procedures. The difference is that most Mortgage States use the Judicial Process and the Deed of Trust States generally use the Power of Sale Process. In the following pages, we have enclosed a list of each State and its

- 11 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

method of handling the foreclosure process, BUT we also suggest strongly that you discuss the exact process with your attorney because the exact process in many states is dependent on the language in your mortgage contract (VERY IMPORTANT).

Types of Liens Where Foreclosure Is Possible

There are a number of types of liens where the lien holder can start a foreclosure proceeding. In your best interest, you should understand who are these individuals or institutions. The IRS (Internal Revenue Service) has the awesome power to lien your property, whether it is homesteaded or not, and with only a reason to believe that you are guilty of some tax evasion or non-payment of taxes due. Other lien holders must have either lent money to the homeowner or provided services or materials that were not paid. Certain states allow homestead exemption have exceptions to the foreclosure process for certain types of liens. The following types of liens can be foreclosed on in most states: 1.) Homeowners Associations Liens or HOA liens are issued by a Board of Directors of your Homeowners Association (i.e. Condo Association) for nonpayment of a number of infractions, including nonpayment of your association dues, special assessments, or unpaid fines for any number of reasons. The Board doesnt want to actually purchase your property but they are seldom negotiable on discounting what are sometimes absurd fines because they know the liens will have to be paid in full to transfer title. Dont mess with the Board of Directors, they can and will make your life a living nightmare because they have the power of deed convent law behind them. These liens can be a VERY small dollar amount to more than the property is worth if they go unpaid for an extended period. The HOA Board generally doesnt want to own the property because they are always strapped for cash. But they will advertise it for sale within the Association Members or try and find a buyer first before foreclosing especially if there is no other mortgage or lien on the property. Be careful, deal with the Board INSTANTLY if this is what is causing your foreclosure. This may require you to show extreme humbleness to get it done, but do it whether you want to or not! This is our personal recommendation from extensive experience in dealing with HOA Boards. 2.) IRS Liens were mentioned briefly above, but the IRS doesnt like to foreclose unless it is an abandoned property or the homeowner (tax

- 12 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

litigant) acts like a real jerk. They dont need to foreclose because they are in first position above any other lien including city or county liens! At the IRSs discretion, these liens can be removed if there is no equity in the property and if the homeowner (seller) will not receive any proceeds from the sale of the property. However, the removal of the lien does not mean it disappears; it is carried forward and attached to the individual owing the money. This is detailed later because it is an important point if you are trying to sell your home and it has an IRS lien attached, because most buyers and lenders wont touch it. 3.) Mechanics liens are generally placed against properties by contractors or material suppliers for non-payment of services rendered. There is usually a time period (90 days from completion of services) in which these liens must be filed or they can not be filed at all, but this varies by state and county. We have seen lawn maintenance services file liens for non-payment of service when they actually did not cut the homeowners grass. The homeowner would not be notified by the County Clerk of the filing and wouldnt find out until he went to closing. Mechanics liens usually expire after a certain number of years so they dont last forever as do most liens and mortgages (unless they are paid off). Tip (#1) Some vendors or contractors, especially those involved in the concrete trade (driveways, curbs, decks, etc.) may have other vendors or sub-contractors deliver material (i.e. concrete) to the job site. Unfortunately, if you picked the contractor with the lowest price, he may not have included the payment for the materials (concrete) and this vendor will be contacting you to pay because the contractor hasnt paid the vendor and doesnt intend to pay! Of course the supply vendor will lien your property for non-payment so MAKE CERTAIN that any contractor doing work for you produces Notice of Payment in Full for Services Rendered, or we prefer a Release of Lien for each and every sub-contractor who worked on your job. This protective action should be done BEFORE you give the contractor his final payment. This is standard practice in commercial building but seldom understood or used in residential construction. 4.) Municipal Code Violations are common for many reasons from something as insignificant as not having your grass mowed, to having junk cars in your yard, or the more serious items such as building additions or any mechanical work that was done without a permit. Code Enforcement is often the city department that enforces issues with Open

- 13 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

Permits. An open permit is where a homeowner or a contractor pulled a permit to do construction, electrical or plumbing work, BUT never had an Inspector come back and Sign Off on the work. It may have been because the contractor thought the homeowner would do it, or the contractors work may not have passed the Final Inspection, but in the end, the result is the same, an open permit in essence becomes a lien against the property. This open permit lien must be resolved before title transfer. When lenders get a property at the courthouse auction, they can sell it with open city or county liens if these liens are properly disclosed to the buyer and he assumes responsibility for resolving them. As an idea of how much these liens can be, we tried to buy a home where the title was clouded by a lien for not mowing the grass. The homeowner was given 10 days to mow his lawn, and he did mow it. However, the code enforcement department was never called back to close the file. Consequently, the fine of $50 per day was imposed and the amount of the lien almost 8.5 years later had grown to $168,568 including interest and penalties! We requested that the county reduce the lien so we could purchase the property and they did to $150! So it is best to fix things quickly and ASK for the city or countys help if you find a problem before it becomes so serious it cant be resolved without paying huge fines. Cities do take properties by Condemnation if the reason(s) for the liens are not cured (fixed) and the property becomes a hazard to the community, so dont mess with them and do what is right. Instead of the city repairing these properties and reselling them, they usually have them demolished and charge the homeowner for the demolition fees. 5.) Mortgages are liens against a property where a lender, either private (individual) or commercial (bank), loans money to the deed holder or lien (mortgage) guarantor for the purchase of the home or some other use of the money. Mortgages are the most common form of property liens. There can be many mortgages against a property, but the first filed has priority or status over any others filed against the property. This is why lenders who do financings or re-financings are so very careful that no other liens are on the property before they issue the funding to the homeowner. Tip (#2) Most mortgages have pre-payment penalties. These pre-payment penalties are a percent of the unpaid balance or a number of regular monthly loan payments. The amounts generally decline as the mortgage gets older. A five year pre-payment is very long and a one year is short. A one year or no-prepayment penalty must usually be

- 14 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

requested at the time of financing and the borrower might have to pay extra for this reduced prepayment penalty. There are two forms of prepayment penalties either they can be a soft prepay, where there is no penalty if the seller (mortgage guarantor) sells the property, but a regular prepayment penalty if he tried to refinance. The other type is a hard prepayment penalty where the seller must pay a penalty if the loan is either re-financed OR the property is sold. It is important that you determine what or if any prepayment penalty you have so you can circumvent this potential problem when you sell or transfer your property!

Types of Mortgages:

a.) Conventional This is a mortgage that is not secured under a government insurance program and is always issued by lending institutions. Most are issued for 15 or 30 years but 40 and 50 year loans are becoming more popular to reduce monthly payments. Historically, most mortgages required 5% to 20% down but in recent years it was not uncommon to get 100% financing for credit worthy individuals. Usually if a borrower puts down less than 20%, the lender requires mortgage insurance (PMI) which helps reduce the loss the lender has if the homeowner defaults.

Tip #3 Lenders are always finding ways to get more money from loans. The newest trick is for the lender to insert a clause in their loan documents that stipulates that if they accelerate your loan (preforeclosure because of a default or late pays), they can collect the prepayment penalty associated with the loan. Previously, when you went into foreclosure the final judgment did not have the pre-payment penalty included. Next time you look to finance, take the time to see if this clause is in your loan and asked to have it removed. No one, except scammers, plan on defaulting when they go into a loan. But stuff happens and you should cover yourself by understanding the terms of your mortgage or lien. b.) Adjustable Rate (ARMs) - These ARMs are the primary cause of the foreclosure rate being so very high. The terms of the mortgage dictate an adjustment to the interest rate at set intervals, with some adjusting as often as monthly. There are 2/28 ARMs which means that the rate doesnt adjust the first 2 years and then adjusts every year for the next 28 years! They are extremely popular because of the low initial cost to buy a home. The problems start

- 15 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

as soon as they start to adjust their interest rates. Some of these adjustments are so extreme that the industry refers to them as Exploding ARMS! c.) Second and Third Mortgages These liens are usually issued by conventional or private lenders, including friends and family members who are willing to take the additional risk of default in exchange for a higher interest rate. These mortgages are recorded after a primary mortgage is recorded first. The order of recording dictates the seniority of the mortgage. The first to be recorded is the senior loan (First Mortgage) and the next loan recorded is a junior loan (Second, Third or Fourth Mortgage). Home Equity Lines of Credit (HELOCS) are usually issued by commercial lenders and are based mostly on a percentage of Fair Market Value (FMV) of the home, and minimally on the credit rating of the borrower. We have seen lenders do 80% of FMV. Some important benefits of home equity loans are that the loans can be repaid without penalty, and interest-only payments can be made monthly to reduce the homeowners mortgage burden. The intent of the loan is generally to do home improvements in the borrowers property, but the use of the proceeds of the loan are seldom restricted to any one use. If the loan is tied to construction at the homeowners property, it is better classified as a construction equity line. Hard Money Loans are mortgages based solely on a percentage of the After Repaired Value (ARV) of the property. Homeowners in foreclosure can easily get these loans from private lenders but must weigh the costs of closing points and fees that could be up to 10% of the loan amount and the fact that these lenders usually only give between 60% and 70% of ARV. For example, if a home needs repairs of $30,000 and the ARV is expected to be $200,000, a hard money lender might advance the homeowner $100,000 (50%) initially and $30,000 (15%) as the repairs are finished, for a total of $130,000 or 65% of the After Repaired Value. Interest rates will range from 10% to 20%, and closing points of 3% to 8% of the loan amount, depending on what your state allows. Remember, if you could not afford your existing mortgage it is very unlikely you will be able to afford a hard money loan. Hand money lenders are traditionally called Predatory Lenders for the obvious reason that they are often hoping that the homeowner will default

- 16 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

d.)

e.)

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

so they can get the property to resell to investors at 75% to 85% of FMV. f.) Government or Government Agency Insured Loans there are three types in this category: i.) F.H.A. or Federal Housing Administration is a government agency which issues loans for marginally credit-worthy borrowers and gives them 95% to 97% of the required funds. F.H.A. loans require the seller to pay a majority of closing costs and the property must pass strict inspection standards. FHA is in the process of a reform and is looking to offer 100% loans, 40 year loans, larger amounts of principal so more buyers will qualify, condo loans will be included, credit standards will be lowered, and most seniors will be able to get reverse mortgages. ii.) H.U.D or Housing and Urban Development is another government agency that handles foreclosures on FHA loans but they will allow a work-out program for homeowners to try to keep the homeowner in the property. They also have the ability to purchase conventional loans and do a work-out with the homeowner. It is worth your effort to determine if your loan qualifies by contacting them directly. V.A. or Veterans Administration loans are given to veterans of the armed services as part of their benefit package for serving their country. The credit requirements are minimal and the seller must pay a substantial part of the closing costs as with FHA loans. Again, the VA is very helpful in working with homeowners to work-out a solution to their foreclosure. It is suggested that you contact them EARLY for the most benefit.

iii.)

g.) FHA HUD Reverse Mortgage (HECM) is designed to send the homeowner a check each month instead of paying a mortgage payment. There are strict requirements for getting such a loan homeowner must meet a few basic requirements of being over age 62, living in the property, and having substantial equity in the home. More than 76,000 HECMs were issued in 2006 and they are a growing trend. While they can be used to stop foreclosure by refinancing and paying off the old mortgage at closing, there may be better options available to the homeowner. This method of refinancing is ultimately expensive

- 17 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

especially where there is a penalty when the loan is closed out or the property is sold. Have an attorney review the terms or any conditions of the HECM if you believe it fits your needs or you could find yourself in foreclosure because of unpaid taxes or insurance.

As always, check with your attorney before you make any assumptions regarding any lien(s) against your home.

Tip (#4) If you intend to refinance to stop your foreclosure, make absolutely certain that you get a Good Faith Estimate (GFE) from the mortgage broker, which is required by law! It is all too common for a mortgage broker to have a client sign a blank GFE saying that he needs time to get the various detailed amount filled in and he will give you a copy later. Unfortunately, you may never see the estimate that you already signed and approved in that pile of documents you signed when you applied for the loan. The GFE is not allowed to be different from the final closing costs by more than 10%. By asking in the beginning, you can compare his costs with other mortgage brokers and you shouldnt be surprised at your closing. Tip (#5) When homeowners get into financial problems and have more than one mortgage to pay they are often not sure which one to pay with what funds they have. If you have only enough money to pay one mortgage, pay the first mortgage. If you only have enough money to pay the second or third mortgage, it is probably better if you DONT pay any of them. The issue is not to save your credit on one loan, the issue is you may not be able to afford your home and if this is the case, paying the junior lien(s) will not stop the foreclosure. However, if you can pay the first mortgage (lien), the junior lien holders are less likely to foreclose because they are in a junior position and would have to purchase the first mortgage at the auction and resell your home to get anything back. If you can get back on your feet financially, negotiate with the junior lien holders to take partial payments because it is in their best interest to get some money rather than none at all.

Judicial Foreclosure

Judicial foreclosure, like every foreclosure, starts when the homeowner stops making mortgage payments, tax or insurance payments, flood insurance payments, payments on junior liens (who foreclose themselves), or the homeowners property is no longer their

- 18 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

principal residence. It may also be instituted because the lender receives numerous payments late (after the 15 days grace period) and invokes terms in the mortgage that start the foreclosure process. Generally, when the homeowner gets 90 days (Judicial Proceeding) or 30 days (Deed of Trust) behind on his mortgage or other required payments, the lender will accelerate or call the loan and start the foreclosure procedure. In Judicial Foreclosure States, the lender (Plaintiff) will petition the County Court (file a law suit) to issue a Lis Pendens. In Latin lis pendens means litigation pending and it is your first legal contact with the lender who is putting you on notice that he is taking legal action and will not wait any longer for your overdue mortgage payments. Within the Lis Pendens filing, the lender also gives notice to any other parties that have liens against the property that they have started the foreclosure process and these subordinate or junior interests need to take their own legal actions or their liens will be extinguished at the foreclosure sale. The Lis Pendens should have attached a copy of the original promissory note (an IOU for money) signed by the borrower and the mortgage note (collateralizes the real estate against the IOU) signed by the borrower. The borrower MAY NOT and DOES NOT HAVE TO BE THE OWNER OF THE HOME. If your Lis Pendens does not have either the Note or the Mortgage copies attached, you should find your original copies, or get copies from the County Clerk, as they contain strict legal language about what the lender can and can not do in the foreclosure proceeding. In a Deed of Trust loan, the Trustee will notify the borrower with a Default Notice and in 30 days he will move to sell the property. I go into more detail about both Judicial and Deeds of Trust foreclosures in the next pages because it is very important that you understand what you have and your rights to legally protect your property. Tip (#6) There are a number of unique opportunities to make money on these seemingly worthless second mortgage loans or junior liens by the buyer of your property, which might be yourself in a short sale. You will have to go to these lien holders and negotiate a discount before the auction. Should these lenders or lien holders decide not to negotiate, tell them it is likely they will get NOTHING when your home goes to the auction and you have a perspective buyer who will not be able to pay off all the existing liens (loans) at 100 cents on the dollar. Offer 5% to start, but usually they will take in the neighborhood of 10% - 20% of the

- 19 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

original amount owed. These loans can be used as 100% credits at the auction - which will be explained later. Tip (#7) Your lender has the right not to accept partial payments unless they choose to, depending on the terms of the lien or mortgage. For example, if the homeowner gets four months behind on his payments, and sends in two monthly payments, the lender has the right to decline this payment. Unfortunately, most often the lender mails the check back to the homeowner and never calls or advises the homeowner until weeks later that the loan is even further in arrears. It seems unfair and it is, but often, if the homeowner speaks to a Supervisor and explains the problem in writing, the lender has the option of accepting the partial payment(s). The key to making this work is to keep asking for another HIGHER Supervisor and dont give up! The lender may request you to sign a Reinstatement Agreement or, if you are very fortunate, a Loan Modification Agreement before they will accept any late payments. Remember, if you sign either one, its purpose is to put you on record that if you have late payments again, they will go back into foreclosure IMMEDIATELY and your rights to a hearing before a judge may be lost no second chance! If you believe you want the settlement they offer, have your attorney review it, sign it and get it back to the bank as soon as possible! You now have a temporary solution for a long-term problem, especially if you cant afford to keep your property. Again, if you get your loan reinstated, but you cant afford the payments, look to sell your home as soon as possible instead of trying to stall for a few more months. Tip (#8) If you sign a Reinstatement Agreement that requires substantially higher payments for three to six months, KEEP your new payments going in on time, because if you get behind again, your chances of the lender helping in the future are ZERO. You have actually lost some of your rights by agreeing to the reinstatement terms because the lender usually includes the rights to a speedier auction process if he has to restart the foreclosure process. We understand that bad problems happen to good people and we will detail how to overcome the problems you may encounter in the future be patient and read this entire text. Once the Lis Pendens is issued by the court, it must be served on the homeowner OR whoever the guarantor is of the mortgage. As mentioned previously, sometimes the homeowner and the guarantor are

- 20 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

different people. This part of the service process leaves itself open to claims of Improper Service as the process server often times assumes the person answering the door is the homeowner, or his spouse and this may not be accurate. For example, improper service could be if the guarantor does not live there or the person served is a renter and the renter is not mentioned in the original filing. The process server should find this out by asking - but sometimes they dont ask and just leave the summons and the renter just throws the document away. Supply your attorney will all the details of your process of service so he can decide if it was done correctly. Tip (#9) Whether you speak to the lenders representative or the attorney for the lender who is filing the Lis Pendens, ONLY believe what you see in writing! NEVER take their word as the truth because it is only your word against theirs and if your home is sold out from under you, you have no recourse without proof. In some states it is illegal to record two party conversations without telling the other party before the conversation starts, so just make sure to get everything in writing. Determine right now if you will be having a Judicial Foreclosure or a Deed of Trust proceeding by looking below at the following table and locate your state. If your state shows both Judicial and NonJudicial in the Foreclosure Process column, you and/or your attorney must READ your mortgage to determine what type of proceeding you will have to go through. Here is a List of Each States Foreclosure Process, ESTIMATED Time to Complete the Foreclosure Process, Any Redemption Period, and Whether a Deficiency Judgment is Possible:

State

Alabama Alaska Arizona Arkansas California Colorado Connecticut Security Instrument(s) Foreclosure Process Est. Time Months Redemption Period Deficiency Judgment

Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage

Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial

13 3 3 4 4 2 2

12 Months Varies by Process None Varies by Process Varies by Process 75 Days None

YES Varies by Process Varies by Process Varies by Process Varies by Process YES YES

- 21 -

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

(Note Below) Delaware Florida Georgia (Note Below) Hawaii Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Mass. Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma

Mortgage Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Deed of Trust Mortgage Mortgage Mortgage Mortgage Mortgage Mortgage Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Mortgage Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Mortgage Mortgage Mortgage or Trust Deed

Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Non-Judicial Judicial Judicial Judicial Judicial Judicial Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial Judicial Judicial or Non-Judicial

3-4 5-6 2-3 2 45 6-7 5 4-5 4 6 2 3 3 3 2 2 2 2 4-5 5-6 3-4 2 3 4 4 2 3 4-5 3

None 10 Days Varies by Process None Either 6 or 12 Months None Yes None 12 Months 12 Months None 12 Months Yes None Yes Yes None Yes None Yes Yes None 10 Days Yes None Yes 6 or 12 Months Yes None

NO YES YES Yes Yes Yes Yes No Yes Yes but Restricted Yes Yes Yes No Varies Yes No No Varies No Yes Yes Yes Yes Yes Varies Yes Yes Varies

- 22 -

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

Oregon Penn. Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington Washington D. C. West Virginia Wisconsin Wyoming

Mortgage or Trust Deed Mortgage Mortgage or Trust Deed Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed Mortgage Mortgage or Trust Deed Mortgage or Trust Deed Mortgage or Trust Deed

Judicial or Non-Judicial Judicial Judicial or Non-Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial Judicial or Non-Judicial Judicial or Non-Judicial Judicial or Non-Judicial

5-6 3 2 Varies 3 2 2 Varies 7 2 4 2 2 3 3

Yes None Varies None Varies Yes None Yes Yes Varies up to 240 Days Yes, but . None None Possibly to 12 Months Yes

Yes Yes Yes Yes Varies Yes Yes Yes Yes Yes Yes Yes No Yes Yes

Connecticut homeowners may be able to claim an exemption from foreclosure under certain circumstances, check with your attorney for full details. Georgia is called a Security Deed state but the process and time involved for the foreclosure is nearly the same as the Deed of Trust states. Beware - if your state has a red box above in the column marked Redemption Period you must formulate your strategy early or you may lose your home by hesitating.

-EXTREMELY IMPORTANTIt is absolutely necessary that after you look at your states parameters above, you get more SPECIFIC information about your judicial or nonjudicial foreclosure process. This information includes an evaluation of

- 23 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

your mortgage or deed of trust document because the clauses in your mortgage determine specifically how your foreclosure will be handled either inside or outside the court system! We suggest that you go online and search for information entitled or related to State Foreclosure Information which should be constantly updated as the laws change and may even give you a referral to a local attorney who can help you. Seek professional help if you have any questions because a few dollars spent now can save your home later KNOW YOUR RIGHTS!

DISCLAIMER - We and our associated companies have no relationship with any of the websites you may encounter online that give state-by-state foreclosure law information, and we can not attest to the information on these sites as being valid or legal. Contact an attorney before making any decision based on information on these websites and in this entire text.

The Actual Process of Judicial Foreclosure

The following is an overview of the sequence of events that occurs when a mortgage guarantor (you) gets thrust into the foreclosure process in a Judicial Foreclosure State: 1.) Homeowner gets behind on his mortgage payments, the actual reason doesnt really matter to the court or the lender since they have heard it all. The lender only cares about solving the problem by the loan being re-instated, paid-off, selling the loan, doing a short sale, or taking the property back at the foreclosure sale. The court is in place to offer judicial settlement of contract law (the mortgage) by one of the following means - postponing the courts decision, dismissing the filing, or issuing a final judgment amount and ordering sale of the property. Lender contacts homeowner by mail and/or telephone but is unable to resolve the late payments, so the lender or Trustee petitions the court to issue a Lis Pendens. The lender(s) can represent themselves in court, as sometimes happens with smaller mortgage amounts (especially second or third mortgages and mechanic liens), but only if your state allows self-representation. The primary lender usually hires a local attorney for court appearances. The attorney for the lender does a title search to determine who has liens against the property, who is on title, sometimes

- 24 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

2.)

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

even who is living at the property. It is important to name both spouses if they are on title or have a spousal interest, otherwise foreclosure would only be for the one spouses interest. Because of the large number of foreclosures, some law firms have huge rooms full of staff attorneys who just do foreclosures. While this process is a gut-wrenching experience to you, it is just a day at the office for the foreclosure attorneys and the court. 3.) A representative of the court (process server, sheriffs officer, privately licensed individual, etc.) serves the homeowner or spouse with the Lis Pendens or Summons as approved by the court. This serving of the homeowner is called the Service of Process. Additionally, duplicate copies of the Summons go to all persons inhabiting the property, any and all persons believed to inhabit the property (John and Jane Does), all persons in the public record who have liens against the property, and the guarantor(s) of the mortgage note.

Tip (#10)- HUGE HINT - Many uninformed homeowners believe that if the process server cant find them the foreclosure will simply go away. The courts have made a contingency for this issue and it is the process called Constructive Notice. This is where the Plaintiff (lender) simply files a notice of the proceeding in the local newspaper for a specified time. So while the homeowner (guarantor) thinks the problem has gone away, it is actually growing worse by leaps and bounds because THE HOMEOWNER IS OUT OF THE INFORMATION LOOP! Dont try and beat the system but rather try and understand it, and have legal representation when necessary. 4.) The homeowner or mortgage guarantor is given 20 calendar days (this varies by county and state) from the Date of Service to answer the summons. Important the 20 days start NOT from the date the court approved the request for the Lis Pendens, but rather from the date of service on the homeowner. The number of days is calculated on Calendar Days which include Saturdays and Sundays, but do not include national holidays. The exact

- 25 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

number of days and whether they are calendar or business days should be explained on the Summons (Lis Pendens). 5.) The homeowner must answer the summons by court appearance or return letter (always refer to the Case Number in your correspondence), or by having an attorney submit a letter or by his making a court appearance again, actual rules vary by county and state. It is critical that you respond so the court isnt forced to issue a Default Judgment which will move you quickly closer to the sale.

The summons should tell you exactly what you have to do so read it thoroughly. Usually the judge for the proceeding will schedule five to ten minutes for your hearing. The Plaintiffs (lenders) attorney will ask that the court set a sale date and grant a final judgment amount that is the full amount of the outstanding balance on the mortgage PLUS accelerated interest, late penalties, and attorneys fees and expenses. The judge will ask the Defendant (mortgage guarantor) to state his case and if he is absent, the judge may issue a Default Judgment equal to exactly what the plaintiffs attorney requested. If the guarantor is present, he can speak to defend his case of why he needs an extension of time, or that he has resolved the problem. If the grantor has responded by mail, the Judge will read the response and make a decision in favor either of the Plaintiff (lender) or the Defendant (mortgage guarantor). Generally, the only favorable decision for the Defendant is if a specific solution is offered to resolve the foreclosure process or if there is a question of the legal validity of the law suit. Unfortunately, the court does not care about the WORST of hardship cases, but it is worth a try to tell your story of why you are behind on your payments. However, your response MUST contain a solution for the back payments and future continuance of the mortgage payments (Reinstatement Agreement), indication of a sale of the property, or a payoff of the loan. Very Important If you file a response letter make certain it is Hand Delivered to the Clerk of the Court or sent certified mail with a return receipt requested. The necessary information of

- 26 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

where to send, or deliver your response, should be on the front of the summons. If it is not, immediately call the Clerk of the Court and get what info you need. You may later need proof that you responded to the summons to support your claim for an extension. If you decide to hand deliver it, CALL AHEAD to save yourself time and aggravation in finding the correct room and person at the courthouse. There should be a telephone number on the Summons that you received to start your search for information.

Tip (#11) - If you do not respond to the Summons or do not show up in court for your hearing, the Plaintiff or their attorney can request a Summary Final Judgment which will accelerate the foreclosure process by 30 to 60 days. Show up and make a case for your needing an extension of at least 30 days BUT have a reason and factual proof in hand! Tip (#12) SCAM ALERT- Because your court appearance is a

matter of public record, you may be approached by individuals as you leave the courtroom for the purpose of getting you to use their services to stall, stop, or refinance your foreclosure. BE POLITE but do not assume that the solutions they are offering are in your best interest. These people may even be soliciting for attorneys who want you to do a bankruptcy. Hold off do not make any commitment until you review all your options which we will be discussing later in this text.

Possible Reasons for a Continuance of Your Foreclosure:

1.) 2.) 3.) 4.) 5.) 6.) 7.) Improper service of the summons* Improper notification of all parties to the Lis Pendens* Other deficiencies or mistakes in the Lis Pendens* Other possible deficiencies are listed in Chapter 5 under Challenge Legality of The Foreclosure section Catastrophic medical issues that may result in you leaving the property AGAIN have proof in hand! You are refinancing the property or you have a lender for the amount needed to reinstate the mortgage in foreclosure (proof is essential) You have a qualified buyer for the property and need additional time to close. You MUST present a copy of

- 27 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

the contract to the court, lender, and the lenders attorney.

*All three of these reasons are best left to an attorney to decide and present to the court.

We have seen Defendants get a signed real estate contract** from a relative to stall the sale. This may work but it could be construed as fraud so your situation better be resolved by the end of the extension date.

**It is possible to sell your property in as little as one weekend using a program we have called the FSBO Power Selling System and It even has a section on selling homes in foreclosure. For more information go to www.FSBOAutoPilot.com

Some states actually bar the homeowner that has been foreclosed on from making a bid for his home at the foreclosure auction. The winner of the bidding at the foreclosure auction requires cash on the day of the sale, so we will disclose the super secret method of using a short sale to re-purchase your home at cents on the dollar in Bonus Report #2. Some states do allow up to 30 days to pay for the purchase, which gives you other options.

Reasons the Court Will Probably May Not Grant a Continuance:

1.) 2.) 3.) Any reason that can not be substantiated. Any personal reason, no matter how terrible the event or the situation unless a medical hardship is involved that is related to staying in your home. A hardship situation that resulted from a scam, unless you have proof of it being reported to the Police.

When you are asking for an extension, always have proof of what caused your being late with your payments, including your lender not accepting partial payments. Any correspondence you have in writing with your lender or his attorney should also be sent to all other parties listed in the Lis Pendens. Otherwise, junior lien holders may start their own foreclosure proceeding. We do it by fax so we have a time-stamped receipt from our fax machine, but we also call back the same day to see if it was

- 28 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

delivered and get the name of the person and time we spoke to them.

Tip (#13) - You should always ask the lenders staff to give an extension if your story is horrific enough AND if it can be proven! The key here is to ask for a Supervisor immediately. You will be asked for a Hardship Letter which we will explain later in the Chapter on Short Sales. We have seen people get as much as one year because they simply spoke to the lender and showed proof of their situation. So try it if it applies! IMPORTANT NOTE While we have seen a clever homeowner delay the foreclosure process for TWO years, it is extremely rare to get past six months in Mortgage states and usually less than 60 days in Deed of Trust states. In the case where the homeowner was able to stay for two years, he was an attorney and used the OLD bankruptcy laws to avoid the foreclosure. Dont plan on this happening to you especially if someone says they know how to do it using bankruptcy as the vehicle! Get your act together because time is working against you and you may find yourself watching the Sheriff dumping all your personal belongings on the front yard when the lender and/or new owner, evict you. We will discuss the issue of filing bankruptcy later because it is important that you know IT WILL NOT WORK to stop the foreclosure. It will postpone it for a SHORT TIME, but the cost to your credit report is very negative and very high to your wallet! 6.) At your hearing, the judge will set a date for the auction sale which generally is 30 to 60 days later, and he will determine the final judgment amount. This Summary Final Judgment is the amount owed to the lender, including all interest, fees, expenses, penalties, and attorney charges. The most important part of the courts decree is the Sale Date. If you make an appearance before the judge at your hearing, it is somewhat likely that he will set a second hearing for 30 - 60 days later even if you didnt make a case for a longer extension, and just by appearing and asking for time. In some states these extra days can be as many as 180+. This varies by county and state so be prepared for anything. At this stage you have just begun to fight and

- 29 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

at least you will know your sale day and have time to overcome your getting your loan re-instated, paid off, or work on a short sale! 7.) Lastly, before the actual sale, you can ask for a special hearing and request an extension for a valid reason. However, there must be extenuating circumstances - such as a signed and verifiable sales contract where the buyer needs conventional financing and more time to complete his loan, a letter from a lender who is re-financing your mortgage, or previously unknown deficiencies in the Plaintiffs filing, service or disclosures. Assuming you dont get a further extension, the next thing that happens is the actual sale at the courthouse steps. The sale will take place about 30 to 60 calendar days after the Final Summary Judgment and will be sold to the highest bidder. We will cover the sale process later because it may be a further opportunity to get your property back or to make money that you would not have otherwise known about. The property is sold by open bid auction with the FIRST bidder being the lender who holds the first mortgage (usually but not always the Plaintiff in your case) it could be a second or third mortgage holder, or even a lien holder who filed the foreclosure proceeding against you. The first mortgage lender will bid $100 over the amount of his mortgage and the bidding starts there and goes until the bidding stops or a bidder reneges on the last bid. Chapter 9 discusses the various aspects of the Courthouse Sale. This chapter is very important, so read this chapter a few times so you completely understand the auction sale process. When the sale is complete, the Clerk of the sale will collect a partial payment from the winning bidder, with the full amount paid by the end of the same day (or as much as 30 days later in some states). The transaction is for cash, but if the buyer is also the lender, the lender gets credit for the mortgage amount shown in the public record or the Final Summary Judgment. For example, if the lender has a lien (mortgage) for $100,000, his attorneys first bid will be $100; it means he is bidding $100,100.00. The one

- 30 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

8.)

9.)

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

hundred is usually the minimal incremental bid in most auction sales but it could be as much as $1,000 depending on the countys rules. In Chapter 9 we will discuss secrets of how professionals bid for and get properties at auction. 10.) After a cooling off or Redemption Period period of usually ten days, the Clerk of the Court will issue a Certificate of Title, assuming there has been no challenge by any interested parties to the foreclosure sale. If there is a challenge by a party to the Lis Pendens, the challenger must petition the court for a hearing. As soon as the outcome of this hearing is finished the judge will instruct the Clerk to begin distribution of all proceeds from the sale and overage proceeds to any qualifying entity or individual (COULD BE YOU!). This may give you an opportunity to get some of your equity or principal back (later discussion is coming because this topic of Overage is VERY important). We will discuss your rights as a mortgage guarantor and homeowner in a later chapter. This redemption period could be as long as two years and it varies greatly, so check your local state laws. To have any hearing on the disposition of the property or any moneys that may be due you, you must petition the court for a hearing during the Redemption Period. The redemption period can be as little as ZERO days or as much as TWO years, see your specific state information to determine your rights. Assuming there is no challenge to the auction sale, either the corporate entity, lender, or the individual who purchased the property at the auction will now be issued a deed to the property, they can now sell it or keep it. Certain states have granted homeowners who lose their homes as much as two years to re-purchase their homes by coming back with the full amount owed, any rehab costs incurred by the new owner, and past due interest and costs to the Trustee. This gigantic advantage to re-purchase your lost home will be discussed at length in Chapter 6 because we will show you how you may be able to make money without buying back your home!

Tip (#14) REMEMBER, the above information IS NOT ACCURATE in states where the Trustee or lender has used

- 31 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

the Power of Sale clause to sell your home. The exception is where the Trustee or lender has used the Judicial Process to foreclose. The Deed of Trust clause is sometimes called a Non-judicial foreclosure process. There is a HUGE difference in the final eviction time for Non-judicial foreclosure process where as little as 30 days is common, compared to the Judicial Foreclosure process where 3 to 5+ months is typical.

NOTE- If in your state, the court orders an appraisal, remember that you should not accommodate the appraiser by getting your home or property cleaned up. Often the appraiser will just do a drive by or use the information in the public record to estimate the value of your property. The higher he estimates the value of your property, the less negotiating power you have with your lender! This is especially true for short sales and will be explained fully in Bonus Report #2. You can also challenge the appraisal to stall for additional time should you need it.

The Actual Process of Non-Judicial Foreclosure

REMEMBER: This foreclosure procedure is very much simplified when compared to the Judicial Foreclosure we discussed previously.

1.) Homeowner gets behind on his mortgage payments but, unfortunately, the reason doesnt matter to the court or the lender. The lender only cares about solving the problem by re-instatement, pay-off, or taking the property at the public sale or the foreclosure sale. Depending on the lenders criteria of what they believe to be sufficiently late (as little as 30 days), they can start to sell your property by sending the Trustee a Letter of Authorization to file a default Notice with the Court. The Trustee first sends a letter to the homeowner or mortgage guarantor that stipulates that payment(s) have been missed and immediate action is required to cure or fix the problem. This notice is called a Notice of

- 32 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

2.)

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

Default. If action is not taken, the Trustee has been authorized to sell your property on behalf of the Deed holder (lender or Beneficiary)! If you have the funds to reinstate the loan, the foreclosure procedure will STOP at this time. We will discuss this Reinstatement Option in greater detail later. The only important thing here is that this option requires money to settle and very quickly. Do not tell the lender that you will do the reinstatement if you have no intention or are incapable of doing it THEY REALLY get angry if you fool with them and you may need their empathy later! 3.) The Trustee will next send a second letter stating that the mortgage has been Accelerated and that payment in full is due immediately. This document is often referred to as the Notice of Sale. Usually, but not always, at this time the Trustee will make an Offer of Reinstatement, which allows the mortgage guarantor the right to pay or reinstate all back payments and fees and go back to his same status before his first late payment. This offer expires as soon as the Trustees sale takes place for which a date has been set in the Notice of Sale letter to the homeowner which will be POSTED on his home and in the public records so anyone can find out if he chooses to do so. If no solution is arrived at by the lender and the homeowner or mortgage guarantor, the Trustee will sell your home at auction either on the court house steps or he may have the authority to sell your property on his own at his leisure through a realtor. Once the auction is completed, the homeowner has the ability to get his home back once again BUT ONLY if the Trustee used a Judicial Procedure to foreclose. This last chance is called a Right of Redemption and varies from state to state by as much as no days to two years. HOWEVER, if the Trustee used the Power of Sale clause in the Deed of Trust, YOU HAVE LOST all rights to get your home property back after the sale is complete. The lender would use the Judicial procedure if he felt that he could collect on a deficiency judgment that

- 33 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

4.)

5.)

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

would be issued by the court if he sold your property for less than was due and payable at the time of the foreclosure. If he used the Power of Sale clause to sell your home, the lender CAN NOT get a deficiency judgment no matter how large the loss. Some exceptions may apply if fraud is involved so check with your attorney before you assume anything. The homeowner is not allowed to purchase his home back at the Trustees Sale but someone else could bid, win and lease back the home to the former owner in most states. While there are emergency measures or stays that can be gotten from the court, these must be filed by your attorney and quickly. The actual steps the lender can take are outlined in your original mortgage documents and should be reviewed carefully. It is not uncommon for the lender to take legal action that is not in your mortgage agreement but the homeowner doesnt know any better and neither does the court unless you bring it to the courts attention.

Thats it it is OVER! You are now living in someone elses home and you will be evicted by the Sheriff, pretty much at the whim of THE NEW OWNER!

Again the difference of the judicial and non-judicial foreclosures is the amount of time the entire process takes and how soon you will be evicted varies from as little as 30 days in a Power of Sale - Deed of Trust state, to four months or even longer in a Mortgage or Judicial Process state.

If you have any questions regarding the exact procedure applicable in your state and county, first call the number on your summons as most clerks in the court system are helpful people. However, you MUST preface your questions with Im not asking for legal advice, but could you tell me This statement lets them know that you are not trying to get them to tell you anything they could lose their job over, and that you

- 34 32 Ways To Quickly Stop Foreclosure Homeowners United 2008 - 2009

32 Ways To Quickly Stop Foreclosure Homeowners United 2008 -2009

just want the usual information. Many counties have gone to online assistance to answer the Frequently Asked Questions (FAQs) and the courthouses (or libraries) have computers available for you to use if you dont otherwise have access to a computer. It is pretty much common knowledge that lenders press nonjudicial foreclosures if they believe they can make money on the sale. If the property is sold at auction, they can bid aggressively to take your home, while in flat or declining real estate markets, they are more lenient about helping resolve your problem. Take time and speak to a Supervisor about your situation because their attorney has no vested benefit to help you, because he gets paid whether you lose your home or not.

Eviction What to Expect