Anda mungkin juga menyukai

- Applications of Marginal Costing: Presented By, Deepu NaziyaDokumen8 halamanApplications of Marginal Costing: Presented By, Deepu NaziyaNazia RahimanBelum ada peringkat

- Listening: Jasmal Safvan Shafi Naziya DeepuDokumen12 halamanListening: Jasmal Safvan Shafi Naziya DeepuNazia RahimanBelum ada peringkat

- Introduction To Computer Hardware and Software : Presented By, Naziya Prinoob SaneeshDokumen21 halamanIntroduction To Computer Hardware and Software : Presented By, Naziya Prinoob SaneeshNazia RahimanBelum ada peringkat

- SIDBIDokumen23 halamanSIDBINazia RahimanBelum ada peringkat

- SIDBIDokumen23 halamanSIDBINazia RahimanBelum ada peringkat

- Mutual Fund: Naziya - K. ADokumen14 halamanMutual Fund: Naziya - K. ANazia RahimanBelum ada peringkat

- Growth and Dev Elopement of Derivatives Market in India - FINALDokumen52 halamanGrowth and Dev Elopement of Derivatives Market in India - FINALdhruvesh.srlim78% (9)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Terrorism Plot ExposedDokumen35 halamanTerrorism Plot Exposedapi-438483578Belum ada peringkat

- College of Criminal Justice Education: Occidental Mindoro State CollegeDokumen8 halamanCollege of Criminal Justice Education: Occidental Mindoro State Collegerosana f.rodriguez100% (1)

- UK Home Office: Ecaa3Dokumen11 halamanUK Home Office: Ecaa3UK_HomeOfficeBelum ada peringkat

- Property Tax Regimes in East AfricaDokumen58 halamanProperty Tax Regimes in East AfricaUnited Nations Human Settlements Programme (UN-HABITAT)Belum ada peringkat

- Unit 8: Sad Experiences in Europe, Rizal'S 2Nd Homecoming, Hongkong Medical Practice and Borneo Colonization ProjectDokumen21 halamanUnit 8: Sad Experiences in Europe, Rizal'S 2Nd Homecoming, Hongkong Medical Practice and Borneo Colonization ProjectMary Abigail LapuzBelum ada peringkat

- Lesson Element Norms and Values ActivityDokumen6 halamanLesson Element Norms and Values ActivityDianne UdtojanBelum ada peringkat

- Mrunal Explained - Love Jihad, Shuddhi Sabha, Tablighi Jamat, TanzimDokumen2 halamanMrunal Explained - Love Jihad, Shuddhi Sabha, Tablighi Jamat, TanzimAmit KankarwalBelum ada peringkat

- MY Current Affairs NotesDokumen127 halamanMY Current Affairs NotesShahimulk Khattak100% (2)

- SOP of Purchase For SabahDokumen119 halamanSOP of Purchase For SabahAnonymous bjGkyOjtBelum ada peringkat

- Hospital List RajasthanDokumen4 halamanHospital List RajasthanJennyBelum ada peringkat

- PIL ReviewerDokumen23 halamanPIL ReviewerRC BoehlerBelum ada peringkat

- Role of Civil Society Organisations in The Implementation of National Food Security Act, 2013Dokumen14 halamanRole of Civil Society Organisations in The Implementation of National Food Security Act, 2013Mehul SaxenaBelum ada peringkat

- (B.M. No. 986.april 13, 2000) in Re 1999 Bar Examinations en Banc GentlemenDokumen1 halaman(B.M. No. 986.april 13, 2000) in Re 1999 Bar Examinations en Banc GentlemenBGodBelum ada peringkat

- Generational Differences Chart Updated 2019Dokumen22 halamanGenerational Differences Chart Updated 2019barukiBelum ada peringkat

- Letter From Taliban Commander Adnan Rasheed To Malala YousafzaiDokumen4 halamanLetter From Taliban Commander Adnan Rasheed To Malala YousafzaiRobert MackeyBelum ada peringkat

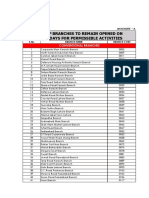

- List of Branches To Remain Opened On Saturdays For Permissible ActivitiesDokumen2 halamanList of Branches To Remain Opened On Saturdays For Permissible Activitiesrai shahzebBelum ada peringkat

- Fundamentals of Argumentation TheoryDokumen19 halamanFundamentals of Argumentation TheoryLaura Georgiana Şiu100% (3)

- Reaction PaperDokumen2 halamanReaction Papermitsuki_sylphBelum ada peringkat

- Test Bank For Business in Action 8th Edition by Bovee IBSN 978013478740Dokumen15 halamanTest Bank For Business in Action 8th Edition by Bovee IBSN 978013478740Jack201100% (4)

- Official Recognition of Kenyan Sign LanguageDokumen10 halamanOfficial Recognition of Kenyan Sign LanguageJack OwitiBelum ada peringkat

- Jake SpeechDokumen2 halamanJake SpeechRandy Jake Calizo Baluscang0% (1)

- Tanada Vs CuencoDokumen3 halamanTanada Vs CuencoJezen Esther Pati100% (2)

- Myanmar)Dokumen25 halamanMyanmar)yeyintBelum ada peringkat

- Apprentice Boys of Derry - Annual Booklet (2019)Dokumen84 halamanApprentice Boys of Derry - Annual Booklet (2019)Andrew CharlesBelum ada peringkat

- The Origins and Development of The Ottoman-Safavid ConflictDokumen214 halamanThe Origins and Development of The Ottoman-Safavid ConflictAbid HussainBelum ada peringkat

- Official Ballot Ballot ID: 25020015 Precinct in Cluster: 0048A, 0048B, 0049A, 0049BDokumen2 halamanOfficial Ballot Ballot ID: 25020015 Precinct in Cluster: 0048A, 0048B, 0049A, 0049BSunStar Philippine NewsBelum ada peringkat

- The Life of Sant Jarnail Singh Khalsa Bhindrawale Part 1Dokumen18 halamanThe Life of Sant Jarnail Singh Khalsa Bhindrawale Part 1www.khojee.wordpress.com50% (2)

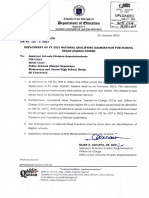

- DM 068, S. 2023-DbNH1KqHMdmtngf8qGznDokumen1 halamanDM 068, S. 2023-DbNH1KqHMdmtngf8qGznJAYNAROSE IBAYANBelum ada peringkat

- Colonial ExpansionDokumen3 halamanColonial ExpansionLaura SumidoBelum ada peringkat

- VFP V ReyesDokumen2 halamanVFP V ReyesRaphael Emmanuel GarciaBelum ada peringkat