Anda mungkin juga menyukai

- BE Lecture 2 Demand & SupplyDokumen47 halamanBE Lecture 2 Demand & SupplyRenata Cleia Lopes HenriquesBelum ada peringkat

- Economics 302 (Sec. 001) Intermediate Macroeconomic Theory and Policy Theory and PolicyDokumen46 halamanEconomics 302 (Sec. 001) Intermediate Macroeconomic Theory and Policy Theory and Policytai2000Belum ada peringkat

- The Science of Macroeconomics: AcroeconomicsDokumen29 halamanThe Science of Macroeconomics: AcroeconomicsAnkur GoelBelum ada peringkat

- Important Issues in MacroeconomicsDokumen4 halamanImportant Issues in MacroeconomicsPatricia AyalaBelum ada peringkat

- The Science of Macroeconomics: AcroeconomicsDokumen29 halamanThe Science of Macroeconomics: AcroeconomicsjitinchandelBelum ada peringkat

- Lec 114Dokumen26 halamanLec 114Kennard ChiaBelum ada peringkat

- MCQ TestDokumen4 halamanMCQ TestChristine ChuahBelum ada peringkat

- Economics: PAPER 1 Multiple Choice (Core)Dokumen12 halamanEconomics: PAPER 1 Multiple Choice (Core)LaLaaLynnBelum ada peringkat

- Chap 01Dokumen29 halamanChap 01mnadiriBelum ada peringkat

- Macroeconomics & International Economics: Orientation LectureDokumen45 halamanMacroeconomics & International Economics: Orientation LectureHitendra KaliaBelum ada peringkat

- Allen ScottDokumen240 halamanAllen ScottosvaldoblancoBelum ada peringkat

- N. Gregory Mankiw: MacroeconomicsDokumen29 halamanN. Gregory Mankiw: MacroeconomicsCarlotta Charlie MarinoBelum ada peringkat

- Macroeconomic Insights from Recent DataDokumen44 halamanMacroeconomic Insights from Recent DataRahul AuddyBelum ada peringkat

- YY YY: II IIDokumen36 halamanYY YY: II IIjoashiBelum ada peringkat

- Assignment Economics 9708Dokumen16 halamanAssignment Economics 9708yddBelum ada peringkat

- Introduction To MacroeconomicsDokumen10 halamanIntroduction To Macroeconomicsthrphys1940Belum ada peringkat

- 3 EcoDokumen33 halaman3 EcoChandan VermaBelum ada peringkat

- 9708 w04 QP 1 PDFDokumen12 halaman9708 w04 QP 1 PDFOng Wei LingBelum ada peringkat

- LIMITATIONS OF GDPDokumen8 halamanLIMITATIONS OF GDPjohn nashBelum ada peringkat

- Memes of Misinformation: Federal Spending: Unraveling the controversial, socio-economic and political issues behind those annoying social media memesDari EverandMemes of Misinformation: Federal Spending: Unraveling the controversial, socio-economic and political issues behind those annoying social media memesBelum ada peringkat

- Macro Ch2 F10Dokumen25 halamanMacro Ch2 F10EEO_MurphyBelum ada peringkat

- Learning ObjectivesDokumen28 halamanLearning Objectivesmihir ambaniBelum ada peringkat

- MN - Economic Practice QuestionsDokumen11 halamanMN - Economic Practice QuestionsMartin GerardBelum ada peringkat

- Econ202 WK1S1Dokumen48 halamanEcon202 WK1S1James DeanBelum ada peringkat

- 3 Demand and Supply AnalysisDokumen24 halaman3 Demand and Supply AnalysisHebziba BeulaBelum ada peringkat

- Demand Supply MarketDokumen53 halamanDemand Supply MarketwasisiBelum ada peringkat

- Analysis of Substitution Changes in The Phillips Curve in V4 Countries Over The Course of Economic CyclesDokumen16 halamanAnalysis of Substitution Changes in The Phillips Curve in V4 Countries Over The Course of Economic CyclesPegy Melati SukmaBelum ada peringkat

- The Science of Macroeconomics: AcroeconomicsDokumen29 halamanThe Science of Macroeconomics: AcroeconomicsDeri YantoBelum ada peringkat

- International Economics:: Trade Theory and PolicyDokumen68 halamanInternational Economics:: Trade Theory and PolicyMuhammad Ateeq Ur RehmanBelum ada peringkat

- 9708 s03 QP 1Dokumen12 halaman9708 s03 QP 1Diksha KoossoolBelum ada peringkat

- Working Paper No 3 Crowding Out 101210Dokumen25 halamanWorking Paper No 3 Crowding Out 101210Fórum de Desenvolvimento do RioBelum ada peringkat

- 2 Micro WS14 15 Demand and SupplyDokumen36 halaman2 Micro WS14 15 Demand and SupplyNeculseanu AndreiBelum ada peringkat

- GE273 Homework Week3Dokumen3 halamanGE273 Homework Week3MrDiazBelum ada peringkat

- Measuring Total Surplus Using Supply and Demand CurvesDokumen68 halamanMeasuring Total Surplus Using Supply and Demand CurvesRashid AyubiBelum ada peringkat

- 04 ElasticityDokumen63 halaman04 ElasticityKishore GubburiBelum ada peringkat

- 3 Misleading IndicatorsDokumen7 halaman3 Misleading IndicatorsKamilė PociūtėBelum ada peringkat

- Supply and Demand: Mcgraw-Hill/Irwin Rights ReservedDokumen42 halamanSupply and Demand: Mcgraw-Hill/Irwin Rights Reservedshruu92Belum ada peringkat

- Economic Growth and Inequality The Colombian ExperienceDokumen294 halamanEconomic Growth and Inequality The Colombian ExperienceAlexandre FreitasBelum ada peringkat

- Micro EconDokumen14 halamanMicro EconjcnissiBelum ada peringkat

- In This Chapter, There Are Four Objectives We Want To LearnDokumen11 halamanIn This Chapter, There Are Four Objectives We Want To LearnelvienBelum ada peringkat

- Policy The Perfectly Competitive Model: Consumer Producer SurplusDokumen88 halamanPolicy The Perfectly Competitive Model: Consumer Producer SurplusPraveen SharmaBelum ada peringkat

- Macroeconomics Ganesh Kumar NDokumen44 halamanMacroeconomics Ganesh Kumar NHimanshu JainBelum ada peringkat

- Voigtländer and Voth (2013 JEP) Gifts of Mars. Warfare and Europes Early Rise To RichesDokumen23 halamanVoigtländer and Voth (2013 JEP) Gifts of Mars. Warfare and Europes Early Rise To RichesPietro QuerciBelum ada peringkat

- MCQ IMPORTANT REVISION QUESTIONS FOR PRACTICE FEB -2023Dokumen15 halamanMCQ IMPORTANT REVISION QUESTIONS FOR PRACTICE FEB -2023pretzBelum ada peringkat

- Demand, Supply & Market EquilibriumDokumen32 halamanDemand, Supply & Market EquilibriumVingdeswaran Subramaniyan0% (1)

- Policy & The PerfectlyDokumen48 halamanPolicy & The PerfectlyRajan RanjanBelum ada peringkat

- Lecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationDokumen80 halamanLecture 5 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationnivecBelum ada peringkat

- 9708 s06 QP 1Dokumen12 halaman9708 s06 QP 1Robinho FontenelleBelum ada peringkat

- pol-economy_2019_class1Dokumen31 halamanpol-economy_2019_class1kimjimBelum ada peringkat

- 9708 s04 QP 1Dokumen12 halaman9708 s04 QP 1Diksha KoossoolBelum ada peringkat

- 2011 HSC Exam EconomicsDokumen20 halaman2011 HSC Exam Economicshappiinesslahxd0% (1)

- 1 Islamic Macroeconomics Introduction - SPDokumen53 halaman1 Islamic Macroeconomics Introduction - SPMuhammad QodriBelum ada peringkat

- StoryboardDokumen5 halamanStoryboardapi-263932656Belum ada peringkat

- Boom and Bust: Ecuador's Financial RollercoasterDari EverandBoom and Bust: Ecuador's Financial RollercoasterBelum ada peringkat

- Who Adjusts?: Domestic Sources of Foreign Economic Policy during the Interwar YearsDari EverandWho Adjusts?: Domestic Sources of Foreign Economic Policy during the Interwar YearsBelum ada peringkat

- The Battle for Europe: How an Elite Hijacked a Continent - and How we Can Take it BackDari EverandThe Battle for Europe: How an Elite Hijacked a Continent - and How we Can Take it BackPenilaian: 4 dari 5 bintang4/5 (2)

- U.S Economy, Construction Industry, and Residential Market Crisis and Recovery, 2000-2019Dari EverandU.S Economy, Construction Industry, and Residential Market Crisis and Recovery, 2000-2019Belum ada peringkat

- The Butterfly Defect: How Globalization Creates Systemic Risks, and What to Do about ItDari EverandThe Butterfly Defect: How Globalization Creates Systemic Risks, and What to Do about ItBelum ada peringkat

- The Shape of Advertising Response Functions RevisitedDokumen11 halamanThe Shape of Advertising Response Functions RevisitedAhmad Khalid NikbinBelum ada peringkat

- Anger Management TechniquesDokumen22 halamanAnger Management TechniquesNiyanta GuptaBelum ada peringkat

- Kotler03exs-Building Customer Satisfaction, Value, and RetentionDokumen18 halamanKotler03exs-Building Customer Satisfaction, Value, and RetentionAhmad Khalid NikbinBelum ada peringkat

- LifestyleDokumen1 halamanLifestyleAhmad Khalid NikbinBelum ada peringkat

- Stats FormulasDokumen3 halamanStats FormulasPeter PhamBelum ada peringkat

- E-Satisfaction, E-Loyalty Contingency FrameworkDokumen16 halamanE-Satisfaction, E-Loyalty Contingency FrameworkKai KonsapBelum ada peringkat

- Intro To Procurement and Contract ManagementDokumen28 halamanIntro To Procurement and Contract ManagementAhmad Khalid Nikbin86% (7)

- Eviews User Guide (All)Dokumen14 halamanEviews User Guide (All)Ahmad Khalid NikbinBelum ada peringkat

- Stats FormulasDokumen3 halamanStats FormulasPeter PhamBelum ada peringkat

- Household Expenses Calculator V1.0Dokumen3 halamanHousehold Expenses Calculator V1.0Ahmad Khalid NikbinBelum ada peringkat

- Post-Closing Trial BalanceDokumen1 halamanPost-Closing Trial BalanceAhmad Khalid NikbinBelum ada peringkat

- BBADokumen27 halamanBBAAhmad Khalid NikbinBelum ada peringkat

- Zeus Asset Management IncDokumen7 halamanZeus Asset Management IncSmitha RajBelum ada peringkat

- Pivot Point Trading Strategy GuideDokumen12 halamanPivot Point Trading Strategy Guideforstermakhado492Belum ada peringkat

- BA 99.1 DiagnosticDokumen1 halamanBA 99.1 Diagnostictikki0219Belum ada peringkat

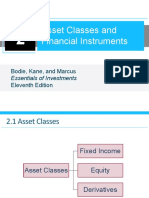

- Asset Classes and Financial Instruments: Bodie, Kane, and Marcus Eleventh EditionDokumen48 halamanAsset Classes and Financial Instruments: Bodie, Kane, and Marcus Eleventh EditionFederico PortaleBelum ada peringkat

- ECO 162-Introduction To MicroeconomicDokumen48 halamanECO 162-Introduction To MicroeconomicNorjiella Binti Mohd NurdinBelum ada peringkat

- Marketing Management - Amul Camel MilkDokumen35 halamanMarketing Management - Amul Camel Milkshreya srivastava100% (1)

- How Knowledge Drives Innovation in the Modern EconomyDokumen15 halamanHow Knowledge Drives Innovation in the Modern EconomysoliekaBelum ada peringkat

- Pas 12Dokumen5 halamanPas 12elle friasBelum ada peringkat

- Marketing ManagementDokumen90 halamanMarketing Managementmech430Belum ada peringkat

- Service Marketing MidtermDokumen2 halamanService Marketing Midtermrıfat serdar kayaBelum ada peringkat

- Natalie Jaeger Resume 1Dokumen1 halamanNatalie Jaeger Resume 1api-384851446Belum ada peringkat

- Analysis of India S National Competitive Advantage in ITDokumen40 halamanAnalysis of India S National Competitive Advantage in ITkapildixit30Belum ada peringkat

- Reserve Management Parts I and II WBP Public 71907Dokumen86 halamanReserve Management Parts I and II WBP Public 71907Primo KUSHFUTURES™ M©QUEENBelum ada peringkat

- GS Guide To Inflation-Linked BondsDokumen8 halamanGS Guide To Inflation-Linked BondsOmer H.Belum ada peringkat

- 1-S2.0-S0040162522000452-Main Digital CapabilityDokumen13 halaman1-S2.0-S0040162522000452-Main Digital CapabilityWafae BarkaniBelum ada peringkat

- Human Resource EconomicsDokumen28 halamanHuman Resource EconomicsAmardeep UpadhyayBelum ada peringkat

- Airtel Bill PaymentDokumen1 halamanAirtel Bill PaymentVipin SinghBelum ada peringkat

- Lecture8 OptionsTrading StrategiesDokumen21 halamanLecture8 OptionsTrading StrategiesRasesh ShahBelum ada peringkat

- Yamaha Corporation (13035676)Dokumen13 halamanYamaha Corporation (13035676)NguyenZumBelum ada peringkat

- Marketing Plan - SampleDokumen35 halamanMarketing Plan - SampleTUMMALAPENTA BHUVAN SAI KARTHIKBelum ada peringkat

- Ambush MarketingDokumen18 halamanAmbush Marketinganish1012Belum ada peringkat

- How Philip Morris Built Marlboro Into A Global Brand For Young AdultsDokumen11 halamanHow Philip Morris Built Marlboro Into A Global Brand For Young AdultsIrvandy Farwezy HamzahBelum ada peringkat

- Procurement Strategies and StructuresDokumen52 halamanProcurement Strategies and StructuresKalkidan100% (1)

- Comparative Analysis of Mutual FundsDokumen76 halamanComparative Analysis of Mutual FundsAditi Atre0% (1)

- International Strategic ManagementDokumen82 halamanInternational Strategic Managementhimanshu sisodia50% (2)

- Bajaj MukeshDokumen93 halamanBajaj Mukeshdharmesh7879Belum ada peringkat

- Jean-Louis Tourne PresentationDokumen20 halamanJean-Louis Tourne PresentationeatnutesBelum ada peringkat

- Re-Thinking Sustainable DeveloDokumen27 halamanRe-Thinking Sustainable DeveloFarhan AlvianaBelum ada peringkat

- Tube Ice FeasibilityDokumen2 halamanTube Ice FeasibilitySiddhartha Bhowmick100% (1)

- International Monetary System HistoryDokumen10 halamanInternational Monetary System HistoryMuhammad RaflyBelum ada peringkat