Anda mungkin juga menyukai

- Empirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveDari EverandEmpirical Note on Debt Structure and Financial Performance in Ghana: Financial Institutions' PerspectiveBelum ada peringkat

- Degree of Leverage: Empirical Analysis from the Insurance SectorDari EverandDegree of Leverage: Empirical Analysis from the Insurance SectorBelum ada peringkat

- Capital Structure and Firm PerformanceDokumen15 halamanCapital Structure and Firm PerformanceAcademicBelum ada peringkat

- The Impact of Capital StructureDokumen27 halamanThe Impact of Capital StructureJoy JepchirchirBelum ada peringkat

- Capital Structure and Profitability of Nigerian Quoted Firms. Chechet & Olayiwola 2014 PDFDokumen20 halamanCapital Structure and Profitability of Nigerian Quoted Firms. Chechet & Olayiwola 2014 PDFTalal ItoBelum ada peringkat

- Capital Structure and Profitability of N PDFDokumen20 halamanCapital Structure and Profitability of N PDFFerdausur RahmanBelum ada peringkat

- Determinants of Capital StructureDokumen38 halamanDeterminants of Capital StructureAbdul QadoosBelum ada peringkat

- Final ProjectDokumen55 halamanFinal ProjectAnjan KumarBelum ada peringkat

- MSC Accounting Seminar PaperDokumen15 halamanMSC Accounting Seminar PaperElias Samuel UnekwuBelum ada peringkat

- Effect of Capital Structure On The Profitability of Selected Companies in NigeriaDokumen8 halamanEffect of Capital Structure On The Profitability of Selected Companies in NigeriaFerdausur RahmanBelum ada peringkat

- Effect of Capital Structure on ProfitabilityDokumen8 halamanEffect of Capital Structure on ProfitabilitysuelaBelum ada peringkat

- Effect of Capital Structure on ProfitabilityDokumen8 halamanEffect of Capital Structure on Profitabilitysuela100% (1)

- Profitability, Growth Opportunity, Capital Structure and The Firm ValueDokumen22 halamanProfitability, Growth Opportunity, Capital Structure and The Firm ValueYohanes Danang PramonoBelum ada peringkat

- Proposal ThesisDokumen8 halamanProposal ThesisFahad Ali 3516-FBAS/BSSE/F17Belum ada peringkat

- Leverage Analysis ProjectDokumen106 halamanLeverage Analysis Projectbalki123Belum ada peringkat

- Thesis Optimal Capital StructureDokumen5 halamanThesis Optimal Capital Structurejennysmithportland100% (1)

- Empirical Use of Financial LeverageDokumen3 halamanEmpirical Use of Financial Leveragesam abbasBelum ada peringkat

- The Impact of Financial Leverage To Profitability Study of Vehicle Companies From PakistanDokumen21 halamanThe Impact of Financial Leverage To Profitability Study of Vehicle Companies From PakistanAhmad Ali100% (1)

- HARSHIT VIJAY 138 corporate finance2Dokumen7 halamanHARSHIT VIJAY 138 corporate finance2harshitvj24Belum ada peringkat

- MSCTHESISDokumen84 halamanMSCTHESISPtomsa KemuelBelum ada peringkat

- The Effect of Debt Equity Ratio, Dividend Payout Ratio, and Profitability On The Firm ValueDokumen6 halamanThe Effect of Debt Equity Ratio, Dividend Payout Ratio, and Profitability On The Firm ValueThe IjbmtBelum ada peringkat

- Banking SectorDokumen27 halamanBanking SectorMiss IqbalBelum ada peringkat

- Thesis Capital Structure and Firm PerformanceDokumen8 halamanThesis Capital Structure and Firm Performancelaurasmithkansascity100% (2)

- A Study On Capital Structure in Sri Pathi Paper and Boards Pvt. LTD., SivakasiDokumen69 halamanA Study On Capital Structure in Sri Pathi Paper and Boards Pvt. LTD., SivakasiGold Gold50% (4)

- MBA Firm Size Capital Structure Liquidity Performance ValueDokumen18 halamanMBA Firm Size Capital Structure Liquidity Performance ValuePatya NandaBelum ada peringkat

- Term Paper New SeniDokumen7 halamanTerm Paper New SeniBiniyam YitbarekBelum ada peringkat

- Impact of Financial Leverage On DividendDokumen5 halamanImpact of Financial Leverage On DividendIkhsan FerdiyanBelum ada peringkat

- Corporate FinanceDokumen14 halamanCorporate FinanceAldi Des SagitariusBelum ada peringkat

- The Effect of Financial Leverage and Market Size on Stock ReturnsDokumen20 halamanThe Effect of Financial Leverage and Market Size on Stock ReturnsSaad HassanBelum ada peringkat

- 8402 Report Fahad Ul HassanDokumen10 halaman8402 Report Fahad Ul HassanSaira KhanBelum ada peringkat

- What Determines The Capital Structure of Ghanaian FirmsDokumen12 halamanWhat Determines The Capital Structure of Ghanaian FirmsHughesBelum ada peringkat

- Capital Structure and Market Values of CompaniesDokumen7 halamanCapital Structure and Market Values of CompaniesKingston Nkansah Kwadwo EmmanuelBelum ada peringkat

- Capital Structure On Bank Performance Report.Dokumen25 halamanCapital Structure On Bank Performance Report.Aniba ButtBelum ada peringkat

- Literature Review On Optimal Capital StructureDokumen6 halamanLiterature Review On Optimal Capital Structureafmzaoahmicfxg100% (2)

- The Effects of Corporate Financing Decisions On Firm Value in Bursa MalaysiaDokumen9 halamanThe Effects of Corporate Financing Decisions On Firm Value in Bursa MalaysiaArif RahmanBelum ada peringkat

- Capital Structure of NTPCDokumen49 halamanCapital Structure of NTPCArunKumar100% (1)

- Factors Determining Capital Structure of Chetinad Cement CorporationDokumen5 halamanFactors Determining Capital Structure of Chetinad Cement CorporationKarthik RamBelum ada peringkat

- CAPITAL STRUCTURE Ultratech 2018Dokumen75 halamanCAPITAL STRUCTURE Ultratech 2018jeevanBelum ada peringkat

- Capital Structure Impact on Steel Manufacturer PerformanceDokumen22 halamanCapital Structure Impact on Steel Manufacturer PerformanceKolaBelum ada peringkat

- Impact of Capital Structure AllDokumen3 halamanImpact of Capital Structure AllAfsana PollobiBelum ada peringkat

- Leverage Analysis ProjectDokumen105 halamanLeverage Analysis ProjectLakshmi_Mudigo_17220% (2)

- Group - 3 - Assignment (Term Paper)Dokumen13 halamanGroup - 3 - Assignment (Term Paper)Biniyam YitbarekBelum ada peringkat

- Active Adjustment Towards Target Capital Structure of Consumer Goods FirmsDokumen6 halamanActive Adjustment Towards Target Capital Structure of Consumer Goods FirmsaijbmBelum ada peringkat

- Impact of Capital Structure On Profitability of Listed Companies of Cement SectorDokumen44 halamanImpact of Capital Structure On Profitability of Listed Companies of Cement SectorZia SiddiquiBelum ada peringkat

- Capital Structure and Financial Performance: Evidence From IndiaDokumen17 halamanCapital Structure and Financial Performance: Evidence From IndiaanirbanccimBelum ada peringkat

- The Effect of Sales Growth On The Determinants of Capital Structure of Listed Companies in Tehran Stock ExchangeDokumen6 halamanThe Effect of Sales Growth On The Determinants of Capital Structure of Listed Companies in Tehran Stock ExchangeJonathan SangimpianBelum ada peringkat

- Determinants of Corporate Capital Structure Under Different Debt Maturities (2011)Dokumen8 halamanDeterminants of Corporate Capital Structure Under Different Debt Maturities (2011)Lê DiệuBelum ada peringkat

- UEU Master 6274 Capital Structure Determinants and Its Influence To Value of The Firm Jurnal Bahasa Inggris DikonversiDokumen18 halamanUEU Master 6274 Capital Structure Determinants and Its Influence To Value of The Firm Jurnal Bahasa Inggris DikonversiNovita IntanBelum ada peringkat

- The Impact of Capital Structure On Profitability of Ethiopian Construction Companies Evidence From Large Tax Pay Organizations 1528 2635 25-2-680Dokumen28 halamanThe Impact of Capital Structure On Profitability of Ethiopian Construction Companies Evidence From Large Tax Pay Organizations 1528 2635 25-2-680Kefi BelayBelum ada peringkat

- The Effect of Debt Capacity On Firms Growth - CompletedDokumen10 halamanThe Effect of Debt Capacity On Firms Growth - CompletedThanh Xuân100% (1)

- Impact of capital structure on FMCG sector profitabilityDokumen9 halamanImpact of capital structure on FMCG sector profitabilityMehmood MuradBelum ada peringkat

- The Handbook of Financing GrowthDokumen6 halamanThe Handbook of Financing GrowthJeahMaureenDominguezBelum ada peringkat

- Matriculation NoDokumen11 halamanMatriculation NoKetz NKBelum ada peringkat

- Capitasl Expenditure (Final Project)Dokumen42 halamanCapitasl Expenditure (Final Project)nikhil_jbp100% (1)

- EIB Working Papers 2018/08 - Debt overhang and investment efficiencyDari EverandEIB Working Papers 2018/08 - Debt overhang and investment efficiencyBelum ada peringkat

- Lessons from Private Equity Any Company Can UseDari EverandLessons from Private Equity Any Company Can UsePenilaian: 4.5 dari 5 bintang4.5/5 (12)

- Analytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationDari EverandAnalytical Corporate Valuation: Fundamental Analysis, Asset Pricing, and Company ValuationBelum ada peringkat

- The EVA Challenge (Review and Analysis of Stern and Shiely's Book)Dari EverandThe EVA Challenge (Review and Analysis of Stern and Shiely's Book)Belum ada peringkat

- Customer Perception ArticleDokumen11 halamanCustomer Perception ArticleAli ShahanBelum ada peringkat

- New Microsoft Office PowerPoint PresentationDokumen1 halamanNew Microsoft Office PowerPoint PresentationGbsReddyBelum ada peringkat

- Reference Proposal CopiedDokumen42 halamanReference Proposal CopiedAli ShahanBelum ada peringkat

- EmeratesDokumen1 halamanEmeratesAli ShahanBelum ada peringkat

- Coke Report For SMDokumen11 halamanCoke Report For SMAli ShahanBelum ada peringkat

- Information SystemsDokumen7 halamanInformation SystemsBalajiBelum ada peringkat

- The Need For Market SegmentationDokumen8 halamanThe Need For Market SegmentationAli ShahanBelum ada peringkat

- Determinants of Capital Structure ChoiceDokumen36 halamanDeterminants of Capital Structure ChoiceAli ShahanBelum ada peringkat

- HBL ReportDokumen7 halamanHBL ReportAli ShahanBelum ada peringkat

- GDP Total: GDP Per Capita: GDP Growth Rate (%) : 6.0 (At Constant Prices 2009-10) Total Exports: Total Imports: Total FDI: Forex Reserves: CurrencyDokumen6 halamanGDP Total: GDP Per Capita: GDP Growth Rate (%) : 6.0 (At Constant Prices 2009-10) Total Exports: Total Imports: Total FDI: Forex Reserves: CurrencyAli ShahanBelum ada peringkat

- Basic StructureDokumen3 halamanBasic StructureAli ShahanBelum ada peringkat

- Corporate Finance OverviewDokumen12 halamanCorporate Finance Overviewadi809hereBelum ada peringkat

- Financial Statement Analysis Problem SolutionsDokumen35 halamanFinancial Statement Analysis Problem SolutionsMaria Younus78% (9)

- Chapter 7 Importance of Money and Capital MarketsDokumen9 halamanChapter 7 Importance of Money and Capital MarketsSyrill CayetanoBelum ada peringkat

- Lesson 5 Agency Problems and Accountability of Corporate Managers and 2Dokumen39 halamanLesson 5 Agency Problems and Accountability of Corporate Managers and 2Dianne Pearl DelfinBelum ada peringkat

- Cast Study - GM MotorsDokumen9 halamanCast Study - GM MotorsAbdullahIsmailBelum ada peringkat

- Sample Questions:: Section I: Subjective QuestionsDokumen8 halamanSample Questions:: Section I: Subjective Questionsnaved katuaBelum ada peringkat

- Turpin BankruptcyDokumen83 halamanTurpin Bankruptcytom cleary100% (1)

- PNB Vs Andrada ElectricDokumen14 halamanPNB Vs Andrada ElectricYe Seul DvngrcBelum ada peringkat

- Luzon Brokerage Co. v. Maritime Building Co. (1972)Dokumen1 halamanLuzon Brokerage Co. v. Maritime Building Co. (1972)Onnie Lee100% (1)

- Chapter 8-SHEDokumen77 halamanChapter 8-SHEVip Bigbang100% (1)

- CommoditiesDokumen5 halamanCommoditiesRachamalla KrishnareddyBelum ada peringkat

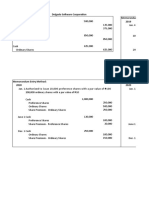

- Memorandum and Journal Entry Methods for Share Capital TransactionsDokumen3 halamanMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- AccountsStatement 63379769Dokumen2 halamanAccountsStatement 63379769omanshBelum ada peringkat

- Agyei Et Al - 2013 - An Assessment of Audit Expectation Gap in GhanaDokumen7 halamanAgyei Et Al - 2013 - An Assessment of Audit Expectation Gap in GhanathoritruongBelum ada peringkat

- Excel TrainingDokumen28 halamanExcel TrainingNiraj Arun ThakkarBelum ada peringkat

- Issue of FCCBs and Ordinary Shares Scheme 1993Dokumen11 halamanIssue of FCCBs and Ordinary Shares Scheme 1993shashasyBelum ada peringkat

- Conservatism in Accounting - Ross L WattsDokumen39 halamanConservatism in Accounting - Ross L WattsDekri FirmansyahBelum ada peringkat

- Updated BIR Citizen's Charter ServicesDokumen40 halamanUpdated BIR Citizen's Charter Servicesfightingmaroon0% (2)

- Altaf CVDokumen2 halamanAltaf CVAyesha AltafBelum ada peringkat

- FIN2004 - 2704 Week 5Dokumen56 halamanFIN2004 - 2704 Week 5ZenyuiBelum ada peringkat

- CH 20 The Mutual Fund IndustryDokumen51 halamanCH 20 The Mutual Fund IndustrynikowawaBelum ada peringkat

- Market Potential Assessment and Road Map Development For The Establishment of Capital Market in EthiopiaDokumen76 halamanMarket Potential Assessment and Road Map Development For The Establishment of Capital Market in EthiopiaAsniBelum ada peringkat

- Export 04 - 08 - 2018 14 - 58Dokumen20 halamanExport 04 - 08 - 2018 14 - 58Anonymous 0JfyYG0Belum ada peringkat

- Negotiable Instruments AIB PDFDokumen488 halamanNegotiable Instruments AIB PDFgomerpiles100% (2)

- CPA - Quizbowl 2008Dokumen10 halamanCPA - Quizbowl 2008frankreedh100% (3)

- Basel Norms in Banking SectorsDokumen36 halamanBasel Norms in Banking SectorsSaikat ChatterjeeBelum ada peringkat

- BANKING ISSUESDokumen17 halamanBANKING ISSUESbhavyaBelum ada peringkat

- 10 Accounting ConceptsDokumen10 halaman10 Accounting ConceptsBurhan Al DangoBelum ada peringkat

- By Otmar, B.A: Leasing PreparedDokumen53 halamanBy Otmar, B.A: Leasing PreparedAnna Mwita100% (1)

- Real Estate Weekly Newsletter Highlights Key Industry UpdatesDokumen27 halamanReal Estate Weekly Newsletter Highlights Key Industry UpdatesAayushi AroraBelum ada peringkat