Anda mungkin juga menyukai

- NEED FOR PROJECT APPRAISAL - October 15th, 2010Dokumen1 halamanNEED FOR PROJECT APPRAISAL - October 15th, 2010sachin_chawlaBelum ada peringkat

- Depository Bank Shares AccountDokumen1 halamanDepository Bank Shares Accountsachin_chawlaBelum ada peringkat

- Ifp 21 Understanding Investment RiskDokumen9 halamanIfp 21 Understanding Investment Risksachin_chawlaBelum ada peringkat

- Ifp 20 Fundamentals of Investment PlanningDokumen4 halamanIfp 20 Fundamentals of Investment Planningsachin_chawlaBelum ada peringkat

- 10 December: Negativity Necessary For Constructive WorkDokumen3 halaman10 December: Negativity Necessary For Constructive Worksachin_chawlaBelum ada peringkat

- Ifp 36 Environment of A Financial PlannerDokumen8 halamanIfp 36 Environment of A Financial Plannersachin_chawlaBelum ada peringkat

- Overall Role PurposeDokumen2 halamanOverall Role Purposesachin_chawlaBelum ada peringkat

- Faridabad Telecom District: Account SummaryDokumen1 halamanFaridabad Telecom District: Account Summarysachin_chawlaBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Claim For Refund and Request For AbatementDokumen1 halamanClaim For Refund and Request For AbatementIRSBelum ada peringkat

- Toshiba Information v. CIR G.R. No. 157594 March 9, 2010Dokumen6 halamanToshiba Information v. CIR G.R. No. 157594 March 9, 2010Emrico CabahugBelum ada peringkat

- IRS Issues Guidance On State Tax Payments To Help TaxpayersDokumen2 halamanIRS Issues Guidance On State Tax Payments To Help TaxpayersMeaghan BellavanceBelum ada peringkat

- Fernando Vazquez567935467Dokumen21 halamanFernando Vazquez567935467Richivee100% (2)

- Swami Samarth Tax Consultants: If You Miss This Vital Step, Your Return Will Be Treated As Not FiledDokumen2 halamanSwami Samarth Tax Consultants: If You Miss This Vital Step, Your Return Will Be Treated As Not FiledmakamkkumarBelum ada peringkat

- Fundamentals of Taxation 2019 Edition 12th Edition Cruz Solutions ManualDokumen48 halamanFundamentals of Taxation 2019 Edition 12th Edition Cruz Solutions ManualGregWilsonarsdn100% (15)

- Pay Slip 37000140 - Apr - 2020 PDFDokumen1 halamanPay Slip 37000140 - Apr - 2020 PDFSumantrra ChattopadhyayBelum ada peringkat

- Taxation: Home Case Digest Notes and Legal Forms Commentary GuestbookDokumen157 halamanTaxation: Home Case Digest Notes and Legal Forms Commentary GuestbookDyëng RäccâBelum ada peringkat

- Coi Ay 22-23Dokumen2 halamanCoi Ay 22-23vikash pandeyBelum ada peringkat

- Commissioner of Internal Revenue Vs Algue Inc., and Court of Tax Appeals GR No. L-28896. February 17, 1988 FactsDokumen61 halamanCommissioner of Internal Revenue Vs Algue Inc., and Court of Tax Appeals GR No. L-28896. February 17, 1988 FactsShall PMBelum ada peringkat

- BAYER FinalDokumen17 halamanBAYER Finalravina bhuvadBelum ada peringkat

- 2019 07 23 09 00 40 881 - 452619484 - PDFDokumen6 halaman2019 07 23 09 00 40 881 - 452619484 - PDFSadhana TiwariBelum ada peringkat

- Tax Practice MCQDokumen16 halamanTax Practice MCQZenedel De JesusBelum ada peringkat

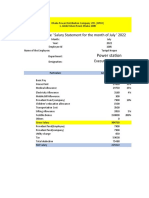

- Tariqul Hoque ' Salary Statement For The Month of July ' 2022Dokumen6 halamanTariqul Hoque ' Salary Statement For The Month of July ' 2022Sadman Rafid FardeenBelum ada peringkat

- Petitioner Respondent: Second DivisionDokumen19 halamanPetitioner Respondent: Second DivisionJeffrey JosolBelum ada peringkat

- CA Inter N22 - Tax Model QPDokumen14 halamanCA Inter N22 - Tax Model QPNAVEEN SURYA MBelum ada peringkat

- Return of Income: Basic InformationDokumen8 halamanReturn of Income: Basic InformationSudmanBelum ada peringkat

- Court Oft Ax Appeal: DecisionDokumen18 halamanCourt Oft Ax Appeal: Decisionjsus22Belum ada peringkat

- COMMISSIONER OF INTERNAL REVENUE Vs CommonwealthDokumen52 halamanCOMMISSIONER OF INTERNAL REVENUE Vs CommonwealthM Azeneth JJBelum ada peringkat

- BPI vs. CA, GR#122480, April 12, 2000Dokumen7 halamanBPI vs. CA, GR#122480, April 12, 2000Khenlie VillaceranBelum ada peringkat

- Goods and Services Tax Refund Tutorial PDFDokumen27 halamanGoods and Services Tax Refund Tutorial PDFMOHANBelum ada peringkat

- NTA Annual ReportDokumen293 halamanNTA Annual ReportAustin DeneanBelum ada peringkat

- The Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATDokumen8 halamanThe Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATDipen AdhikariBelum ada peringkat

- Star Novel Coronavirus (Ncov) (Covid-19) Insurance Policy (Pilot Product)Dokumen2 halamanStar Novel Coronavirus (Ncov) (Covid-19) Insurance Policy (Pilot Product)Me SutradharBelum ada peringkat

- Chapter 06 - Share of Profit From Association of PersonsDokumen6 halamanChapter 06 - Share of Profit From Association of PersonsSuniel JamilBelum ada peringkat

- Tax Remedies DigestsDokumen50 halamanTax Remedies DigestsybunBelum ada peringkat

- Rapid Meal Marketing PlanDokumen26 halamanRapid Meal Marketing PlanAng JamesBelum ada peringkat

- FTFCS 2023-04-14 1681510273125 PDFDokumen17 halamanFTFCS 2023-04-14 1681510273125 PDFIvel RhaenBelum ada peringkat

- Taxation Law (2007-2013)Dokumen125 halamanTaxation Law (2007-2013)Axel FontanillaBelum ada peringkat

- CIR vs. PL Management Intl Phils. Inc. GR No. 160949Dokumen4 halamanCIR vs. PL Management Intl Phils. Inc. GR No. 160949ZeusKimBelum ada peringkat