Anda mungkin juga menyukai

- 02chapters1 3Dokumen113 halaman02chapters1 3ALTERINDONESIABelum ada peringkat

- Corporate Governance and Firms' Financial Performance: Cite This PaperDokumen12 halamanCorporate Governance and Firms' Financial Performance: Cite This PaperRahmat KaswarBelum ada peringkat

- Corporate Governance and Firms PerformanceDokumen12 halamanCorporate Governance and Firms PerformanceDrSekhar Muni AmbaBelum ada peringkat

- Corporate Governence TNBDokumen4 halamanCorporate Governence TNBSyurga FathonahBelum ada peringkat

- Voluntary Disclosure and Corporate GovernanceDokumen21 halamanVoluntary Disclosure and Corporate GovernanceAngela NixxBelum ada peringkat

- Corporate Governance Proposal Partial WorkDokumen9 halamanCorporate Governance Proposal Partial Workkeen writerBelum ada peringkat

- A Comparative Study of The Corporate Governance Codes of A Developing Economy With Developed EconomiesDokumen14 halamanA Comparative Study of The Corporate Governance Codes of A Developing Economy With Developed EconomiesAlexander DeckerBelum ada peringkat

- CORPORATE_GOVERNANCE,_ANALYSESDokumen15 halamanCORPORATE_GOVERNANCE,_ANALYSESPavithra GopalakrishnanBelum ada peringkat

- 2831 4849 1 PB PDFDokumen4 halaman2831 4849 1 PB PDFVivianBelum ada peringkat

- Audit Committee Practice in The Polish Listed Stock Companies. Present Situation and Development Perspectives Piotr SzczepankowskiDokumen16 halamanAudit Committee Practice in The Polish Listed Stock Companies. Present Situation and Development Perspectives Piotr Szczepankowski1moss123Belum ada peringkat

- (2010 Rev Jan 19 Teehankee) Corporate GovernanceDokumen19 halaman(2010 Rev Jan 19 Teehankee) Corporate GovernanceRaymond Pacaldo100% (2)

- Corporate Governance and its Impact on Bank PerformanceDokumen66 halamanCorporate Governance and its Impact on Bank PerformanceSadia NBelum ada peringkat

- Corporate governance, leadership, and performanceDokumen8 halamanCorporate governance, leadership, and performancemanishaamba7547Belum ada peringkat

- Bank Research TopicsDokumen13 halamanBank Research TopicsnobleconsultantsBelum ada peringkat

- Influence of Corporate Governance On Accounting Outcomes & Firms PerformanceDokumen16 halamanInfluence of Corporate Governance On Accounting Outcomes & Firms PerformanceVarga AlinBelum ada peringkat

- The Internal Audit As Function To The Corporate GoDokumen17 halamanThe Internal Audit As Function To The Corporate GoBharat BhushanBelum ada peringkat

- Susan Abed (2012) - Corporate Governance and Earnings Management Jordanian EvidenceDokumen10 halamanSusan Abed (2012) - Corporate Governance and Earnings Management Jordanian Evidenceheryp123Belum ada peringkat

- Mahlet Fikiru ThesisDokumen66 halamanMahlet Fikiru ThesisYohannes KassaBelum ada peringkat

- Corporate Governance Impact on Indian Firm PerformanceDokumen11 halamanCorporate Governance Impact on Indian Firm PerformanceAbhishek GagnejaBelum ada peringkat

- Corporate Governance and Financial Crises: What Have We MissedDokumen15 halamanCorporate Governance and Financial Crises: What Have We MissedTarun SinghBelum ada peringkat

- International Journal of Advanced Research in Management and Social Sciences (ISSN: 2278-6236)Dokumen16 halamanInternational Journal of Advanced Research in Management and Social Sciences (ISSN: 2278-6236)ijgarph0% (1)

- Asian Economic and Financial Review: Neeraj K. Sehrawat Amit Kumar Nandita Lohia Satvik Bansal Tanya AgarwalDokumen11 halamanAsian Economic and Financial Review: Neeraj K. Sehrawat Amit Kumar Nandita Lohia Satvik Bansal Tanya AgarwalGhulam NabiBelum ada peringkat

- CG and FDDokumen12 halamanCG and FDAkhil1101Belum ada peringkat

- 218-Article Text-662-1-10-20211130Dokumen21 halaman218-Article Text-662-1-10-20211130Emmanuel KimeuBelum ada peringkat

- The Impact of Board Characteristics On Earnings Management 1528 2635 23-1-339Dokumen26 halamanThe Impact of Board Characteristics On Earnings Management 1528 2635 23-1-339F LBelum ada peringkat

- Internal Control and Corporate Governance Among CooperativesDokumen14 halamanInternal Control and Corporate Governance Among CooperativesThe IjbmtBelum ada peringkat

- Proposed Research Work For Major Research Project On: "A Study On Indian Corporate Governance Practices"Dokumen11 halamanProposed Research Work For Major Research Project On: "A Study On Indian Corporate Governance Practices"Yepuru ChaithanyaBelum ada peringkat

- Institutional Ownership and Discretionary Accruals: Empirical Evidences From Pakistani Listed Non-Financial CompaniesDokumen6 halamanInstitutional Ownership and Discretionary Accruals: Empirical Evidences From Pakistani Listed Non-Financial CompaniesrseteaBelum ada peringkat

- Corporate Governance Mechanism and Cost of Capital To Firm ValueDokumen14 halamanCorporate Governance Mechanism and Cost of Capital To Firm ValuetanviBelum ada peringkat

- For Plag CheckDokumen259 halamanFor Plag CheckAftab TabasamBelum ada peringkat

- Research Work Halimat-OriginalDokumen83 halamanResearch Work Halimat-Originalibrodan681Belum ada peringkat

- Sample Article For IBR AuthorDokumen26 halamanSample Article For IBR AuthorA.K. JyoteBelum ada peringkat

- Auditing For Corporate Governance in The GCC: Prof. Wael E. AL-RashedDokumen15 halamanAuditing For Corporate Governance in The GCC: Prof. Wael E. AL-RashedaijbmBelum ada peringkat

- Enron ScandalDokumen9 halamanEnron ScandalSalman JindranBelum ada peringkat

- Corporate Governance and Organizational PerformanceDokumen3 halamanCorporate Governance and Organizational PerformanceEshanokpe DanielBelum ada peringkat

- Audit and GCGDokumen10 halamanAudit and GCGGerry Ditan SibueaBelum ada peringkat

- Daba Research ProposalDokumen33 halamanDaba Research Proposalyifru gizachewBelum ada peringkat

- Dividend PoliciesDokumen16 halamanDividend PoliciesSrinivasa BalajiBelum ada peringkat

- Corporate Governance and Firms Financial Performance in The United KingdomDokumen15 halamanCorporate Governance and Firms Financial Performance in The United KingdomYoung On Top BaliBelum ada peringkat

- Corporate Governance and Reporting: An Empirical Study of The Listed Companies in BangladeshDokumen32 halamanCorporate Governance and Reporting: An Empirical Study of The Listed Companies in BangladeshShakib ShakibBelum ada peringkat

- The Impact of Ownership Structure on Information AsymmetryDokumen11 halamanThe Impact of Ownership Structure on Information AsymmetryMohamed EL-MihyBelum ada peringkat

- Corporate Governance - Presentation-12Dokumen53 halamanCorporate Governance - Presentation-12Puneet MittalBelum ada peringkat

- CGBEDokumen28 halamanCGBEmaddymatBelum ada peringkat

- Good Corporate Governance and Cost of Debt: Listed Companies On Indonesian Institute For Corporate GovernanceDokumen20 halamanGood Corporate Governance and Cost of Debt: Listed Companies On Indonesian Institute For Corporate GovernanceReynold SimangunsongBelum ada peringkat

- Corporate Governance Attributes and Financial Reporting Quality: Empirical Evidence From IranDokumen7 halamanCorporate Governance Attributes and Financial Reporting Quality: Empirical Evidence From Iranbig birdBelum ada peringkat

- Implementasi Sarbanes-Oxley Act Dalam Meningkatkan Praktik Corporate GovernanceDokumen18 halamanImplementasi Sarbanes-Oxley Act Dalam Meningkatkan Praktik Corporate GovernancemiraBelum ada peringkat

- Internal Audit AktivityDokumen17 halamanInternal Audit AktivityhomeschoolingBelum ada peringkat

- Corporate Governance Mechanism and Firm Performance A Study of Listed Manufacturing Firms in Nigeri1Dokumen59 halamanCorporate Governance Mechanism and Firm Performance A Study of Listed Manufacturing Firms in Nigeri1jamessabraham2Belum ada peringkat

- Chap4 PDFDokumen45 halamanChap4 PDFFathurBelum ada peringkat

- Influence of Corporate Governance On Accounting Outcomes & Firms PerformanceDokumen16 halamanInfluence of Corporate Governance On Accounting Outcomes & Firms PerformanceVarga AlinBelum ada peringkat

- Sadaf SpinnerDokumen7 halamanSadaf SpinnerDr-Liaqat AliBelum ada peringkat

- Megan MediaDokumen8 halamanMegan Mediarose0% (1)

- Determinants of Governance Parameters Towards Investor's Performance in Perspective of Regulatory and Legal FrameworkDokumen24 halamanDeterminants of Governance Parameters Towards Investor's Performance in Perspective of Regulatory and Legal FrameworkNam Khánh TrầnBelum ada peringkat

- Corporate Governance Capital Structure and Firm Perfromance Eacse PDFDokumen30 halamanCorporate Governance Capital Structure and Firm Perfromance Eacse PDFCharles AkaraBelum ada peringkat

- Impact of Corporate Governance On Corporate Financial PerformanceDokumen5 halamanImpact of Corporate Governance On Corporate Financial PerformanceneppoliyanBelum ada peringkat

- CGP in NGODokumen5 halamanCGP in NGOHashir bariBelum ada peringkat

- The Influence of Corporate Governance Mechanism On Performance of Manufacturing Listed Companies in Indonesia Stock ExchangeDokumen13 halamanThe Influence of Corporate Governance Mechanism On Performance of Manufacturing Listed Companies in Indonesia Stock ExchangeThe IjbmtBelum ada peringkat

- Undertaken by A Govt, MKT or Network, Over A Family, Tribe, Formal or Informal Orgn or Territory & Through Laws, Norms, Power or LanguageDokumen40 halamanUndertaken by A Govt, MKT or Network, Over A Family, Tribe, Formal or Informal Orgn or Territory & Through Laws, Norms, Power or LanguageLeo PanmeiKhangBelum ada peringkat

- Public Accounts Committee and Oversight Function in Nigeria - ADokumen7 halamanPublic Accounts Committee and Oversight Function in Nigeria - AKenneth Enoch OkpalaBelum ada peringkat

- Empirical Relationship Between Capital Base and Profitability of Deposit Money Banks in NigeriaDokumen13 halamanEmpirical Relationship Between Capital Base and Profitability of Deposit Money Banks in NigeriaKenneth Enoch OkpalaBelum ada peringkat

- Venture Capital and The Emergence and Development of Entrepreneurship - A Focus On Employment Generation and Poverty AlleDokumen8 halamanVenture Capital and The Emergence and Development of Entrepreneurship - A Focus On Employment Generation and Poverty AlleKenneth Enoch OkpalaBelum ada peringkat

- Total Quality Management and SMPS PerformanceDokumen16 halamanTotal Quality Management and SMPS PerformanceKenneth Enoch OkpalaBelum ada peringkat

- Strategic Budgeting System and Management of PublicDokumen10 halamanStrategic Budgeting System and Management of PublicKenneth Enoch OkpalaBelum ada peringkat

- Adoption of Ifrs and Fs Effects AjbmrDokumen8 halamanAdoption of Ifrs and Fs Effects AjbmrKenneth Enoch OkpalaBelum ada peringkat

- Fiscal Accountability Dilemma in Nig Public SectorDokumen20 halamanFiscal Accountability Dilemma in Nig Public SectorKenneth Enoch OkpalaBelum ada peringkat

- Security Analysis 6th Edition IntroductionDokumen3 halamanSecurity Analysis 6th Edition IntroductionTheodor ToncaBelum ada peringkat

- UAE Commercial Companies LawDokumen23 halamanUAE Commercial Companies Lawsajida mohdBelum ada peringkat

- Discontinued Operation: Pfrs 5Dokumen19 halamanDiscontinued Operation: Pfrs 5FRITZ IVAN DENIELLE M. GERONABelum ada peringkat

- Investor / Analyst Presentation (Company Update)Dokumen48 halamanInvestor / Analyst Presentation (Company Update)Shyam SunderBelum ada peringkat

- Solution Manual For Financial and Managerial Accounting 8th by WildDokumen45 halamanSolution Manual For Financial and Managerial Accounting 8th by WildTiffanyFowlercftzi100% (41)

- Harsh Mini ProjectDokumen178 halamanHarsh Mini ProjectHarsh Kumar100% (1)

- Other ExDokumen17 halamanOther ExDaniel HunksBelum ada peringkat

- Balance Sheet of Coal IndiaDokumen28 halamanBalance Sheet of Coal IndiaShankari MaharajanBelum ada peringkat

- Grade 12 Fabm 2 ReviewerDokumen36 halamanGrade 12 Fabm 2 ReviewerAgabus MoralesBelum ada peringkat

- Definitions: References To Earnings Refer To Net Income (Loss) Attributable To ConocophillipsDokumen10 halamanDefinitions: References To Earnings Refer To Net Income (Loss) Attributable To ConocophillipsRidwan AbdurahmanBelum ada peringkat

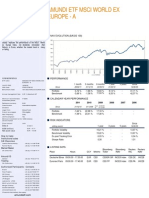

- Amundi ETF Tracks World ex Europe StocksDokumen2 halamanAmundi ETF Tracks World ex Europe Stockshp24714303Belum ada peringkat

- Barclays - Tesco1Q2324salesreview-strongUKLFLsales (90) - Jun - 16 - 2023Dokumen22 halamanBarclays - Tesco1Q2324salesreview-strongUKLFLsales (90) - Jun - 16 - 2023Edward LaiBelum ada peringkat

- Chapter 12 Build a ModelDokumen6 halamanChapter 12 Build a ModelTimothy Gikonyo0% (1)

- Financial Statement Analysis of Microsoft Corporation (Revised)Dokumen7 halamanFinancial Statement Analysis of Microsoft Corporation (Revised)Adhikansh SinghBelum ada peringkat

- ACDVol 2018 2019Dokumen15 halamanACDVol 2018 2019Nirav ShahBelum ada peringkat

- Accounting What The Numbers Mean 11th Edition Marshall Test BankDokumen43 halamanAccounting What The Numbers Mean 11th Edition Marshall Test Bankmalabarhumane088100% (28)

- E - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - SohelDokumen41 halamanE - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - Sohelitika.chaudharyBelum ada peringkat

- Cost and Management Accounting Topic-Ratio Analysis and Cash Flow Statement of Reliance Industries Ltd. 2019 - 2020Dokumen8 halamanCost and Management Accounting Topic-Ratio Analysis and Cash Flow Statement of Reliance Industries Ltd. 2019 - 2020sarans goelBelum ada peringkat

- E5-26A: Cost-Method Consolidation For Majority-Owned SubsidiaryDokumen9 halamanE5-26A: Cost-Method Consolidation For Majority-Owned SubsidiaryeryBelum ada peringkat

- Performance Analysis of Working Capital ManagementDokumen67 halamanPerformance Analysis of Working Capital ManagementRamandeep KaurBelum ada peringkat

- Questions and Answers: On The Common Operation of The Market Abuse DirectiveDokumen9 halamanQuestions and Answers: On The Common Operation of The Market Abuse DirectiveblockakiBelum ada peringkat

- Activity 3-Cae06: 1. The Bookkeeper of Latsch Company, Which Has An Accounting Year EndingDokumen3 halamanActivity 3-Cae06: 1. The Bookkeeper of Latsch Company, Which Has An Accounting Year EndingMarian Gerangaya07Belum ada peringkat

- Account Statement: Folio No.: 18340825 / 96Dokumen3 halamanAccount Statement: Folio No.: 18340825 / 96Gauri BansalBelum ada peringkat

- Finance Live Project/summer Internship Details April-May-June - 2020Dokumen3 halamanFinance Live Project/summer Internship Details April-May-June - 2020Arihant JainBelum ada peringkat

- PWC Deals Retail Consumer Insights q2 2016Dokumen5 halamanPWC Deals Retail Consumer Insights q2 2016Peter ShiBelum ada peringkat

- Amalgamation, Absorption & External Reconstruction: Chapter-IDokumen15 halamanAmalgamation, Absorption & External Reconstruction: Chapter-Ibharat wankhedeBelum ada peringkat

- REO CPA Review: Revaluation and ImaprimentDokumen4 halamanREO CPA Review: Revaluation and ImaprimentAdan NadaBelum ada peringkat

- Piercing the Veil of Corporate FictionDokumen5 halamanPiercing the Veil of Corporate FictionMaddison YuBelum ada peringkat

- Tab A - Pre-Closing Trial BalanceDokumen4 halamanTab A - Pre-Closing Trial Balancearellano lawschoolBelum ada peringkat

- ICARE-Preweek-AFAR-Part 1Dokumen6 halamanICARE-Preweek-AFAR-Part 1john paul100% (1)