Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Credit Control MethodsDokumen3 halamanCredit Control Methodsprasal75% (4)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Case QuestionsDokumen5 halamanCase Questionschoijin9870% (1)

- Hybrid Distribution ModelDokumen16 halamanHybrid Distribution ModelDipinderBelum ada peringkat

- Chap - 4 ProblemsDokumen2 halamanChap - 4 Problemspartha_biswas_uiuBelum ada peringkat

- Policies Which A UK Government Could Use To Control The Activities of OligopolistsDokumen4 halamanPolicies Which A UK Government Could Use To Control The Activities of OligopolistsSMEBtheWizard100% (2)

- BNY Mellon PresentationDokumen16 halamanBNY Mellon PresentationAnkit SharmaBelum ada peringkat

- WD 0000001Dokumen108 halamanWD 0000001Navin PadsalaBelum ada peringkat

- Jaimin PatelDokumen92 halamanJaimin PatelNavin PadsalaBelum ada peringkat

- Marketing Mix FinalDokumen87 halamanMarketing Mix FinalNavin PadsalaBelum ada peringkat

- Summer Internship Report DipakDokumen86 halamanSummer Internship Report DipakNavin PadsalaBelum ada peringkat

- Research Methodolog1Dokumen3 halamanResearch Methodolog1Navin PadsalaBelum ada peringkat

- Objectives of The Project: QuestionnaireDokumen3 halamanObjectives of The Project: QuestionnaireNavin PadsalaBelum ada peringkat

- Research MethodologyDokumen1 halamanResearch MethodologyNavin PadsalaBelum ada peringkat

- Litrature ReviwDokumen6 halamanLitrature ReviwNavin PadsalaBelum ada peringkat

- Colgate SensodyneDokumen11 halamanColgate SensodynePrateek AshatkarBelum ada peringkat

- Chapter 16, Online Banking and Investing: OutlineDokumen42 halamanChapter 16, Online Banking and Investing: OutlineJennifer Gabrielle IrawanBelum ada peringkat

- StockTwits 50: Breadth, Trends, and TradesDokumen5 halamanStockTwits 50: Breadth, Trends, and TradesDanny JassyBelum ada peringkat

- Tour Report On Chittagong Stock ExchangeDokumen5 halamanTour Report On Chittagong Stock ExchangeRajuRahmotulAlamBelum ada peringkat

- Merchant Banking SyllabusDokumen4 halamanMerchant Banking SyllabusjeganrajrajBelum ada peringkat

- Chapter 20 Corporate FinanceDokumen37 halamanChapter 20 Corporate FinancediaBelum ada peringkat

- BNR Norm No. 3/2005Dokumen3 halamanBNR Norm No. 3/2005BaiatuCuBulanBelum ada peringkat

- Basic FinanceDokumen6 halamanBasic FinanceApril Joy A. Peralta75% (4)

- Demand, Supply & Equilibrium PricesDokumen21 halamanDemand, Supply & Equilibrium PricesKathrina DoriaBelum ada peringkat

- Emotion Drives Investor DecisionsDokumen1 halamanEmotion Drives Investor DecisionsTori PatrickBelum ada peringkat

- TATADokumen27 halamanTATASrideb SahaBelum ada peringkat

- Export Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, GandhinagarDokumen19 halamanExport Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, Gandhinagartamanna88Belum ada peringkat

- OLIGOPSONYDokumen3 halamanOLIGOPSONYBernard Okpe100% (1)

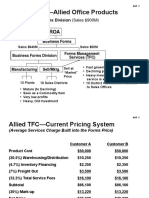

- ABC Costing Allied Office ProductsDokumen13 halamanABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Bank For International SettlementDokumen31 halamanBank For International SettlementGagan Bathla100% (1)

- SWOT Analysis of PRAN Food LimitedDokumen2 halamanSWOT Analysis of PRAN Food Limitedreza006475% (4)

- Customer Value, Types and CLTVDokumen15 halamanCustomer Value, Types and CLTVSp Sps0% (1)

- Resumen Distribution SystemsDokumen7 halamanResumen Distribution SystemswalterBelum ada peringkat

- Depository Institutions: Activities and CharacteristicsDokumen15 halamanDepository Institutions: Activities and Characteristicschhassan7Belum ada peringkat

- ACI Study TextDokumen168 halamanACI Study TextHangoba ZuluBelum ada peringkat

- Nism Questions-26 GDokumen14 halamanNism Questions-26 GabhishekBelum ada peringkat

- Competitive DynamicsDokumen13 halamanCompetitive DynamicsAneesh VargheseBelum ada peringkat

- Microeconomics III (Information Economics) : Master in Industrial Economics. Spring 2012Dokumen4 halamanMicroeconomics III (Information Economics) : Master in Industrial Economics. Spring 2012apoyouniversitarioBelum ada peringkat

- American Depository ReceiptDokumen2 halamanAmerican Depository ReceiptKrishna Prasad GaddeBelum ada peringkat