Anda mungkin juga menyukai

- International Trade Finance: A NOVICE'S GUIDE TO GLOBAL COMMERCEDari EverandInternational Trade Finance: A NOVICE'S GUIDE TO GLOBAL COMMERCEBelum ada peringkat

- Understand Banks & Financial Markets: An Introduction to the International World of Money & FinanceDari EverandUnderstand Banks & Financial Markets: An Introduction to the International World of Money & FinancePenilaian: 4 dari 5 bintang4/5 (9)

- International Banking and FinanceDokumen7 halamanInternational Banking and FinanceravikungwaniBelum ada peringkat

- International BankingDokumen50 halamanInternational Bankingkevalcool250100% (1)

- Financial system overview and key componentsDokumen20 halamanFinancial system overview and key componentsMad GirlBelum ada peringkat

- Merchant Banking and Financial Services Semester III UNITDokumen13 halamanMerchant Banking and Financial Services Semester III UNITNishantChaturvediBelum ada peringkat

- Fdocuments - in Sanjay Final Project of Mahindra FinanceDokumen74 halamanFdocuments - in Sanjay Final Project of Mahindra FinanceSayesha SheikhBelum ada peringkat

- Chapter - 1Dokumen73 halamanChapter - 1Adv AravindBelum ada peringkat

- LeasingDokumen126 halamanLeasingRajjan PrasadBelum ada peringkat

- CH 01Dokumen24 halamanCH 01তৌহিদুর রহমান শাওনBelum ada peringkat

- Mahindra FinanceDokumen75 halamanMahindra FinanceRAHULBelum ada peringkat

- Role of Financial Systems in Economic GrowthDokumen7 halamanRole of Financial Systems in Economic GrowthRVBelum ada peringkat

- Fsbi NotesDokumen74 halamanFsbi Notessanthoshkalpavally5164100% (11)

- NBFC Full NotesDokumen69 halamanNBFC Full NotesJumana haseena SBelum ada peringkat

- BanksDokumen5 halamanBanksparvezbub_490779093Belum ada peringkat

- Banking Law PYQDokumen11 halamanBanking Law PYQxakij19914Belum ada peringkat

- Financial Services - Unit 1Dokumen20 halamanFinancial Services - Unit 1Mahesh Kumar N SBelum ada peringkat

- Introduction to Financial Institutions: An OverviewDokumen16 halamanIntroduction to Financial Institutions: An OverviewsleshiBelum ada peringkat

- Landscape of Financial Services: Section - ADokumen12 halamanLandscape of Financial Services: Section - Aanjney050592Belum ada peringkat

- Raja ProjectDokumen108 halamanRaja ProjectDeepak AkojuBelum ada peringkat

- Chapter 1 - Structure of Financial SystemDokumen18 halamanChapter 1 - Structure of Financial SystemNur HazirahBelum ada peringkat

- India Financial System 2018 PDFDokumen41 halamanIndia Financial System 2018 PDFPiyush ChaturvediBelum ada peringkat

- Factors and Functions of International BankingDokumen36 halamanFactors and Functions of International Bankinganilpeddamalli0% (1)

- 2) Main Role and Functions of RBI Monetary Authority: Formulates Implements and Monitors The Monetary Policy For A)Dokumen12 halaman2) Main Role and Functions of RBI Monetary Authority: Formulates Implements and Monitors The Monetary Policy For A)Tony JoseBelum ada peringkat

- 02 Financial SystemDokumen19 halaman02 Financial SystemGhulam HassanBelum ada peringkat

- Unit I: Importance of Banking SystemDokumen19 halamanUnit I: Importance of Banking SystemdollyBelum ada peringkat

- Banking Finanacial Services Management Unit I: Two Mark QuestionsDokumen10 halamanBanking Finanacial Services Management Unit I: Two Mark QuestionsBose GRBelum ada peringkat

- Banking Finanacial Services Management Unit I: Two Mark QuestionsDokumen21 halamanBanking Finanacial Services Management Unit I: Two Mark QuestionsIndhuja MBelum ada peringkat

- Issue ManagementDokumen194 halamanIssue ManagementBubune KofiBelum ada peringkat

- H.R. Machiraju-Modern Commercial Banking-New Age International (2008) - EDITDokumen10 halamanH.R. Machiraju-Modern Commercial Banking-New Age International (2008) - EDITsahatrenold96Belum ada peringkat

- Unit 1 Structure of Banking in IndiaDokumen31 halamanUnit 1 Structure of Banking in IndiaArjun NayakBelum ada peringkat

- Financial Markets and InstitutionssDokumen30 halamanFinancial Markets and InstitutionssEntityHOPEBelum ada peringkat

- FM&SDokumen18 halamanFM&SVinay Gowda D MBelum ada peringkat

- Riks Modeling of Banking IndustryDokumen18 halamanRiks Modeling of Banking IndustrySumra KhanBelum ada peringkat

- The Commercial Letter of Credit Final NA TALAGADokumen27 halamanThe Commercial Letter of Credit Final NA TALAGAMaricar SalameñaBelum ada peringkat

- Chapter 1 - Overview of Indian Financial SystemDokumen36 halamanChapter 1 - Overview of Indian Financial SystemMukunda VBelum ada peringkat

- BFI 317 Lesson 1 An Overview of Banks and The Financial - Services SectorDokumen16 halamanBFI 317 Lesson 1 An Overview of Banks and The Financial - Services Sectorjusper wendoBelum ada peringkat

- Important Questions BankingDokumen21 halamanImportant Questions BankingAshutosh AgalBelum ada peringkat

- 2024 Module GFEBDokumen57 halaman2024 Module GFEBJesalie BatacBelum ada peringkat

- Chapter 1Dokumen9 halamanChapter 1AliansBelum ada peringkat

- Major Functions of International BankingDokumen7 halamanMajor Functions of International BankingSandra Clem SandyBelum ada peringkat

- Indian financial system, markets and institutionsDokumen23 halamanIndian financial system, markets and institutionsRam MohanreddyBelum ada peringkat

- Unit Iii (International Business Environment)Dokumen22 halamanUnit Iii (International Business Environment)RAMESH KUMARBelum ada peringkat

- Financial Markets and IntermediariesDokumen40 halamanFinancial Markets and IntermediariesFarapple24Belum ada peringkat

- Management For Financial Institutions PDFDokumen25 halamanManagement For Financial Institutions PDFEkhlas Jami100% (2)

- LIQUIDITY RISK ISSUES FACED BY BANKING SECTORDokumen15 halamanLIQUIDITY RISK ISSUES FACED BY BANKING SECTORDeepa GoenkaBelum ada peringkat

- Cia - 1 Risk in Financial Services - Com643CDokumen9 halamanCia - 1 Risk in Financial Services - Com643CGoutham ShineBelum ada peringkat

- Universal Banking LatestDokumen189 halamanUniversal Banking LatestSony Bhagchandani50% (2)

- Nurul Fatehah Binti Ahmad (2018637822)Dokumen5 halamanNurul Fatehah Binti Ahmad (2018637822)Cekelat UdangBelum ada peringkat

- Module IDokumen36 halamanModule IKrishna GuptaBelum ada peringkat

- International BankingDokumen20 halamanInternational Bankingamit098765432150% (6)

- A Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsDokumen143 halamanA Manual On Non Banking Financial Institutions: 9. Anti Money Laundering StandardsRahul JagwaniBelum ada peringkat

- Project SynopsisDokumen7 halamanProject Synopsisdevarakonda shruthiBelum ada peringkat

- Risk Management in BanksDokumen47 halamanRisk Management in BankshitkarkhannaBelum ada peringkat

- Credit Risk Management in BanksDokumen53 halamanCredit Risk Management in Banksrahulhaldankar100% (1)

- PobDokumen24 halamanPobgillyhicksBelum ada peringkat

- Overview On The Banking, Financial Services and Insurance (BFSI) SectorDokumen24 halamanOverview On The Banking, Financial Services and Insurance (BFSI) SectorsaktipadhiBelum ada peringkat

- Bank Fundamentals: An Introduction to the World of Finance and BankingDari EverandBank Fundamentals: An Introduction to the World of Finance and BankingPenilaian: 4.5 dari 5 bintang4.5/5 (4)

- Wealth Global Navigating the International Financial MarketsDari EverandWealth Global Navigating the International Financial MarketsBelum ada peringkat

- Yes Bank Corp Govn.Dokumen24 halamanYes Bank Corp Govn.choco_pie_952Belum ada peringkat

- Turnaround Main ProjectDokumen13 halamanTurnaround Main Projectchoco_pie_952Belum ada peringkat

- International Business TybbiDokumen7 halamanInternational Business Tybbichoco_pie_952Belum ada peringkat

- What is KYC? Understanding Know Your Customer requirementsDokumen2 halamanWhat is KYC? Understanding Know Your Customer requirementschoco_pie_952Belum ada peringkat

- Marketing Group 3 PPT PresentationDokumen29 halamanMarketing Group 3 PPT Presentationchoco_pie_952Belum ada peringkat

- Marketing Book ReportDokumen9 halamanMarketing Book Reportchoco_pie_952Belum ada peringkat

- Tender DocumentsDokumen198 halamanTender DocumentsŞükrüBelum ada peringkat

- Project Feasibility Report For Automobile RepairDokumen7 halamanProject Feasibility Report For Automobile RepairFaisal Maqsood83% (6)

- TechnotronicsDokumen1 halamanTechnotronicsviral patelBelum ada peringkat

- KCCLDokumen18 halamanKCCLAnonymous v6pZ9s9MNBelum ada peringkat

- Fanijo Poultry-Fesibility Study and Posible OutcomeDokumen51 halamanFanijo Poultry-Fesibility Study and Posible OutcomeSamuel Fanijo100% (2)

- U) HZFT CF - SM8"DF// 0 F.JZ sJU"v#f VG (58Fjf/F LCTGL Ju"V$Gl Vgi Huifvmgl EztlDokumen22 halamanU) HZFT CF - SM8"DF// 0 F.JZ sJU"v#f VG (58Fjf/F LCTGL Ju"V$Gl Vgi Huifvmgl Eztlparesh4trivediBelum ada peringkat

- Name: Kuna Satya Srinivasa Raju ROLL NO:200914006 (CEM) Project Management Lab-2 Assignment No - 6Dokumen14 halamanName: Kuna Satya Srinivasa Raju ROLL NO:200914006 (CEM) Project Management Lab-2 Assignment No - 6Srinivasa RajuBelum ada peringkat

- General Terms Conditions For Goods Purchase-Sale ContractDokumen3 halamanGeneral Terms Conditions For Goods Purchase-Sale ContractBelal AhmadBelum ada peringkat

- Relief From Property AccountabilityDokumen1 halamanRelief From Property AccountabilityLorelynCenteno100% (1)

- RBC CaseAnswers Group13Dokumen4 halamanRBC CaseAnswers Group13Shikha Gupta100% (1)

- Rwanda Public Procurement Law Covers Tenders, Bids and Procurement MethodsDokumen179 halamanRwanda Public Procurement Law Covers Tenders, Bids and Procurement MethodsThéotime HabinezaBelum ada peringkat

- MarketingDokumen3 halamanMarketingN.MUTHUKUMARANBelum ada peringkat

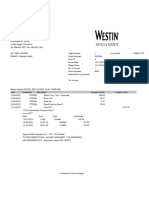

- Westin Hotels & Resorts - 2023-12-10 - 257.78Dokumen2 halamanWestin Hotels & Resorts - 2023-12-10 - 257.78rahul.transcountsBelum ada peringkat

- HVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Dokumen18 halamanHVS - HVS-Anarock-India-Hospitality-Industry-Review-2018Vinod PatelBelum ada peringkat

- CAME Certification GuideDokumen12 halamanCAME Certification GuideManikanta SatishBelum ada peringkat

- Competition Policy 2Dokumen64 halamanCompetition Policy 2goyal_khushbu88Belum ada peringkat

- Pealoza Seeks Specific Performance or Damages for Purchase of Property FloorDokumen22 halamanPealoza Seeks Specific Performance or Damages for Purchase of Property Floorshirlyn cuyongBelum ada peringkat

- STEEPLE Analysis of Argentina's Environment, Society and EconomyDokumen10 halamanSTEEPLE Analysis of Argentina's Environment, Society and EconomyDisha0309Belum ada peringkat

- Bank Comfort Letter SampleDokumen1 halamanBank Comfort Letter SampleSunar Anom Arya Ganda100% (1)

- Research Paper 2.6.1Dokumen26 halamanResearch Paper 2.6.1Rianne Oosting0% (1)

- Unit Trust of India: Prepared By: Supervised byDokumen41 halamanUnit Trust of India: Prepared By: Supervised byGaurav Goel100% (2)

- Loan Application FormDokumen2 halamanLoan Application FormAntonique HeadmanBelum ada peringkat

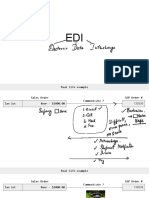

- EDI: The Foundation of Digital Business IntegrationDokumen61 halamanEDI: The Foundation of Digital Business IntegrationYasmine ArabBelum ada peringkat

- Press Release (Company Update)Dokumen3 halamanPress Release (Company Update)Shyam SunderBelum ada peringkat

- Sss vs. CA and Quality Tobacco CorporationDokumen3 halamanSss vs. CA and Quality Tobacco CorporationOlan Dave LachicaBelum ada peringkat

- Financial Rehabilitation and Insolvency ActDokumen6 halamanFinancial Rehabilitation and Insolvency ActEliyah JhonsonBelum ada peringkat

- CSE4DSS Lecture 1 Decision Support and Business IntelligenceDokumen53 halamanCSE4DSS Lecture 1 Decision Support and Business IntelligenceAbdulaziz AlaliBelum ada peringkat

- Horngrens Accounting 12th Edition Nobles Solutions ManualDokumen109 halamanHorngrens Accounting 12th Edition Nobles Solutions ManualAnnGregoryDDSytidk100% (16)

- Pure Logic GroupDokumen28 halamanPure Logic GroupPure Logic GroupBelum ada peringkat

- Accounting For ReceivablesDokumen4 halamanAccounting For ReceivablesKenya LevyBelum ada peringkat