Anda mungkin juga menyukai

- The Great Recession: The burst of the property bubble and the excesses of speculationDari EverandThe Great Recession: The burst of the property bubble and the excesses of speculationBelum ada peringkat

- Shelter from the Storm: How a COVID Mortgage Meltdown Was AvertedDari EverandShelter from the Storm: How a COVID Mortgage Meltdown Was AvertedBelum ada peringkat

- Decoding the New Mortgage Market: Insider Secrets for Getting the Best Loan Without Getting Ripped OffDari EverandDecoding the New Mortgage Market: Insider Secrets for Getting the Best Loan Without Getting Ripped OffBelum ada peringkat

- Michael Burry and Mark BaumDokumen13 halamanMichael Burry and Mark BaumMario Nakhleh0% (1)

- Macro PaperDokumen8 halamanMacro Paperapi-284111637Belum ada peringkat

- NINJA Loans To Blame For Financial CrisisDokumen25 halamanNINJA Loans To Blame For Financial Crisischapy86Belum ada peringkat

- Crisis FinancieraDokumen4 halamanCrisis Financierahawk91Belum ada peringkat

- What Is A Subprime Mortgage?Dokumen5 halamanWhat Is A Subprime Mortgage?Chigo RamosBelum ada peringkat

- Summary and Analysis of The Big Short: Inside the Doomsday Machine: Based on the Book by Michael LewisDari EverandSummary and Analysis of The Big Short: Inside the Doomsday Machine: Based on the Book by Michael LewisBelum ada peringkat

- Case Study On Subprime CrisisDokumen24 halamanCase Study On Subprime CrisisNakul SainiBelum ada peringkat

- The Anatomy of A Crisis: Speculative BubbleDokumen3 halamanThe Anatomy of A Crisis: Speculative BubbleVbiidbdiaan ExistimeBelum ada peringkat

- The Big Short Movie AnalysisDokumen8 halamanThe Big Short Movie AnalysisMoses MachariaBelum ada peringkat

- U.S. Subprime Mortgage Crisis (A & B)Dokumen8 halamanU.S. Subprime Mortgage Crisis (A & B)prabhat kumarBelum ada peringkat

- The Financial Crisis of 2008: What Happened in Simple TermsDokumen2 halamanThe Financial Crisis of 2008: What Happened in Simple TermsBig ALBelum ada peringkat

- US Subprime MortgageDokumen9 halamanUS Subprime MortgageN MBelum ada peringkat

- This Content Downloaded From 141.211.4.224 On Wed, 05 Aug 2020 17:16:17 UTCDokumen28 halamanThis Content Downloaded From 141.211.4.224 On Wed, 05 Aug 2020 17:16:17 UTCRaymond Behnke [STUDENT]Belum ada peringkat

- Guaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinanceDari EverandGuaranteed to Fail: Fannie Mae, Freddie Mac, and the Debacle of Mortgage FinancePenilaian: 2 dari 5 bintang2/5 (1)

- Summary of Bethany McLean & Joe Nocera's All the Devils Are HereDari EverandSummary of Bethany McLean & Joe Nocera's All the Devils Are HereBelum ada peringkat

- Explanation and Overview of The Loan Securitization Process GenericDokumen8 halamanExplanation and Overview of The Loan Securitization Process GenericChemtrails Equals Treason100% (2)

- Why Procedural Requirements Are Necessary To Prevent Further Loss To HomeownersDokumen34 halamanWhy Procedural Requirements Are Necessary To Prevent Further Loss To HomeownersForeclosure Fraud100% (3)

- Factors That Led To Global Financial CrisisDokumen3 halamanFactors That Led To Global Financial CrisisCharles GarrettBelum ada peringkat

- Term Paper FinalDokumen5 halamanTerm Paper Finalapi-301896412Belum ada peringkat

- Financial Service: Project On: Economic MeltdownDokumen40 halamanFinancial Service: Project On: Economic MeltdownJas777Belum ada peringkat

- Other People's Houses: How Decades of Bailouts, Captive Regulators, and Toxic Bankers Made Home Mortgages a Thrilling BusinessDari EverandOther People's Houses: How Decades of Bailouts, Captive Regulators, and Toxic Bankers Made Home Mortgages a Thrilling BusinessPenilaian: 4 dari 5 bintang4/5 (2)

- Asymmetric Information and Financial Crises: By: Tayyaba Rehman Arishma Khurram Sufyan Khan Aniqa JavedDokumen12 halamanAsymmetric Information and Financial Crises: By: Tayyaba Rehman Arishma Khurram Sufyan Khan Aniqa JavedTayyaba RehmanBelum ada peringkat

- The Mortgage Crisis, MERS, and Chapter 13Dokumen16 halamanThe Mortgage Crisis, MERS, and Chapter 13DinSFLA100% (1)

- The Financial Crisis of 2007 - Roles of CDOs, CDSs and Subprime MortgagesDokumen25 halamanThe Financial Crisis of 2007 - Roles of CDOs, CDSs and Subprime MortgagesSertaç Yay100% (1)

- Objection To Settlement of Predatory Mortgage Lending Class ActionDokumen31 halamanObjection To Settlement of Predatory Mortgage Lending Class ActionCharlton ButlerBelum ada peringkat

- Name: Syed Sikander Hussain Shah Course: Eco 607 Topic: Mortgage Crisis STUDENT ID: 024003260Dokumen7 halamanName: Syed Sikander Hussain Shah Course: Eco 607 Topic: Mortgage Crisis STUDENT ID: 024003260Sam GitongaBelum ada peringkat

- The Big ShortDokumen4 halamanThe Big ShortHads LunaBelum ada peringkat

- How Subprime Mortgages Fueled the Housing CrisisDokumen5 halamanHow Subprime Mortgages Fueled the Housing CrisisRoentgen Djon Kaiser IgnacioBelum ada peringkat

- 1.11.10 5:00 P.M.Dokumen13 halaman1.11.10 5:00 P.M.ga082003Belum ada peringkat

- Subprime Crisis FeiDokumen13 halamanSubprime Crisis FeiDavuluri SasiBelum ada peringkat

- US Housing BubbleDokumen6 halamanUS Housing BubbleAnil NandyalaBelum ada peringkat

- For Closure Note Supreme Court DecisionDokumen3 halamanFor Closure Note Supreme Court DecisionJulio Cesar NavasBelum ada peringkat

- Enforcement Issues For A Creditor Holding Multiple Deeds of Trust On The Same Property (2009)Dokumen12 halamanEnforcement Issues For A Creditor Holding Multiple Deeds of Trust On The Same Property (2009)mtandrewBelum ada peringkat

- Anatomy of the Subprime CrisisDokumen49 halamanAnatomy of the Subprime CrisisAbhay ManeBelum ada peringkat

- Foreclosure Fraud in A NutshellDokumen8 halamanForeclosure Fraud in A NutshellMichael Kovach100% (7)

- Global Recession PresentationDokumen23 halamanGlobal Recession PresentationkeshatBelum ada peringkat

- Mortgage Credit CrisisDokumen5 halamanMortgage Credit Crisisasfand yar waliBelum ada peringkat

- Cashing in Chapter 7Dokumen19 halamanCashing in Chapter 7cismercBelum ada peringkat

- NAACP Remarks - Understanding The Foreclosure CrisisDokumen10 halamanNAACP Remarks - Understanding The Foreclosure CrisisJH_CarrBelum ada peringkat

- Case Study 1 - What Was The Financial Crisis of 2007-2008Dokumen4 halamanCase Study 1 - What Was The Financial Crisis of 2007-2008Anh NguyenBelum ada peringkat

- Subprime Mortgage CrisisDokumen18 halamanSubprime Mortgage Crisisredheattauras0% (1)

- Credit Derivatives Not InsuranceDokumen59 halamanCredit Derivatives Not InsuranceGlobalMacroForumBelum ada peringkat

- Global RecessionDokumen15 halamanGlobal RecessionsureshsusiBelum ada peringkat

- Gods at War: Shotgun Takeovers, Government by Deal, and the Private Equity ImplosionDari EverandGods at War: Shotgun Takeovers, Government by Deal, and the Private Equity ImplosionPenilaian: 4 dari 5 bintang4/5 (2)

- Assignment Subprime MortgageDokumen6 halamanAssignment Subprime MortgagemypinkladyBelum ada peringkat

- Landmark Decision ArticleDokumen3 halamanLandmark Decision ArticleEaton GoodeBelum ada peringkat

- Where to Put Your Money NOW: How to Make Super-Safe Investments and Secure Your FutureDari EverandWhere to Put Your Money NOW: How to Make Super-Safe Investments and Secure Your FutureBelum ada peringkat

- Goldman Sachs Abacus 2007 Ac1 An Outline of The Financial CrisisDokumen14 halamanGoldman Sachs Abacus 2007 Ac1 An Outline of The Financial CrisisAkanksha BehlBelum ada peringkat

- Congressional Foreclosure ReportDokumen26 halamanCongressional Foreclosure ReportNetClarity100% (1)

- Assignment 3 FINMARDokumen2 halamanAssignment 3 FINMARKimberly Mae DuetesBelum ada peringkat

- Financial Instruments Responsible For Global Financial CrisisDokumen15 halamanFinancial Instruments Responsible For Global Financial Crisisabhishek gupte100% (4)

- Toxic Document Fallout 10-12-10Dokumen14 halamanToxic Document Fallout 10-12-10Richard Franklin KesslerBelum ada peringkat

- Custom and PracticeDokumen5 halamanCustom and PracticeRichard Franklin KesslerBelum ada peringkat

- MERS® - Good Strawman or Bad Strawman?: by Phillip C. Querin, QUERIN LAW, LLC Contact InfoDokumen8 halamanMERS® - Good Strawman or Bad Strawman?: by Phillip C. Querin, QUERIN LAW, LLC Contact InfoQuerpBelum ada peringkat

- Analysis of Merger Control Under Indian Competition Law by Tejas K. MotwanDokumen29 halamanAnalysis of Merger Control Under Indian Competition Law by Tejas K. MotwanPrashant MauryaBelum ada peringkat

- The Shift From FERA To FEMADokumen3 halamanThe Shift From FERA To FEMAPrashant MauryaBelum ada peringkat

- Environment TopicsDokumen4 halamanEnvironment TopicsPrashant MauryaBelum ada peringkat

- Filth) : Omic Times. 20 DecemberDokumen1 halamanFilth) : Omic Times. 20 DecemberPrashant MauryaBelum ada peringkat

- Abul F.M. Maniruzzaman Lex Mer & Intl Contracts (80 P) PDFDokumen79 halamanAbul F.M. Maniruzzaman Lex Mer & Intl Contracts (80 P) PDFPrashant MauryaBelum ada peringkat

- Attly ArbitrationDokumen11 halamanAttly ArbitrationPrashant MauryaBelum ada peringkat

- Wto CasesDokumen84 halamanWto CasesPrashant MauryaBelum ada peringkat

- Promise of International Commercial MediationDokumen31 halamanPromise of International Commercial MediationPrashant MauryaBelum ada peringkat

- AttlyDokumen2 halamanAttlyPrashant MauryaBelum ada peringkat

- Surya - Law & LitDokumen7 halamanSurya - Law & LitPrashant MauryaBelum ada peringkat

- Globalization in Aviation Sector: India's ExperienceDokumen22 halamanGlobalization in Aviation Sector: India's ExperiencePrashant Maurya100% (1)

- M A Due Diligence PDFDokumen7 halamanM A Due Diligence PDFPrashant MauryaBelum ada peringkat

- Modes of Entering International Business GuideDokumen32 halamanModes of Entering International Business GuidePrashant MauryaBelum ada peringkat

- 36smriti PPTDokumen48 halaman36smriti PPTPrashant MauryaBelum ada peringkat

- BankingDokumen19 halamanBankingPrashant MauryaBelum ada peringkat

- Lex Mercatoria and Aviation PDFDokumen19 halamanLex Mercatoria and Aviation PDFPrashant MauryaBelum ada peringkat

- White Collar Crime - Cases, Materials, and ProblemsDokumen72 halamanWhite Collar Crime - Cases, Materials, and ProblemsS. Bala DahiyaBelum ada peringkat

- CISG Vs UCC PDFDokumen13 halamanCISG Vs UCC PDFPrashant MauryaBelum ada peringkat

- Singapore International Arbitration Centre: Ratifying The CISG - India's OptionsDokumen8 halamanSingapore International Arbitration Centre: Ratifying The CISG - India's OptionsPrashant Maurya100% (1)

- Project M&ADokumen59 halamanProject M&APrashant MauryaBelum ada peringkat

- Insurance ProjectDokumen22 halamanInsurance ProjectPrashant Maurya100% (1)

- Cisg and inDokumen4 halamanCisg and inPrashant MauryaBelum ada peringkat

- IMp. Cases of ICAO PDFDokumen75 halamanIMp. Cases of ICAO PDFPrashant MauryaBelum ada peringkat

- Fdi in Retail SecDokumen9 halamanFdi in Retail SecPrashant MauryaBelum ada peringkat

- Fdi in Multi-Brand RetailingDokumen21 halamanFdi in Multi-Brand RetailingHitesh GoyalBelum ada peringkat

- Globalization in Aviation Sector: India's ExperienceDokumen22 halamanGlobalization in Aviation Sector: India's ExperiencePrashant Maurya100% (1)

- LLPDokumen24 halamanLLPPrashant MauryaBelum ada peringkat

- Euthanasia in IndiaDokumen3 halamanEuthanasia in IndiaPrashant MauryaBelum ada peringkat

- DTaa AGREEMETDokumen13 halamanDTaa AGREEMETPrashant MauryaBelum ada peringkat

- Lukas Foutz - w6 Personal Finance Project - 5375624Dokumen12 halamanLukas Foutz - w6 Personal Finance Project - 5375624api-393000194Belum ada peringkat

- Berar Finance LimitedDokumen9 halamanBerar Finance LimitedKamlakar AvhadBelum ada peringkat

- Business Law TeacherDokumen3 halamanBusiness Law TeacherAMIN BUHARI ABDUL KHADER100% (1)

- Chronology of Data Breaches - Privacy Rights Clearinghouse - June 4, 2014Dokumen558 halamanChronology of Data Breaches - Privacy Rights Clearinghouse - June 4, 2014St. Louis Public RadioBelum ada peringkat

- Introduction AstralDokumen12 halamanIntroduction AstralMbavhalelo100% (1)

- A Project Report On BajajDokumen17 halamanA Project Report On BajajSandeep Tripathi71% (7)

- Bajaj Finance Fixed Deposit ReviewDokumen35 halamanBajaj Finance Fixed Deposit ReviewAlok ShuklaBelum ada peringkat

- How Open Banking Can Support SME FinanceDokumen13 halamanHow Open Banking Can Support SME FinanceADBI EventsBelum ada peringkat

- Week 2 Practice SolutionDokumen1 halamanWeek 2 Practice SolutionalexandraBelum ada peringkat

- Working Capital ReportDokumen22 halamanWorking Capital Reportdivyansh khandujaBelum ada peringkat

- Bureau of Internal RevenueDokumen5 halamanBureau of Internal RevenuegelskBelum ada peringkat

- Chapter 2 Governance and ManagementDokumen32 halamanChapter 2 Governance and Managementlmmh100% (2)

- Bill Gross Investment Outlook May - 07Dokumen9 halamanBill Gross Investment Outlook May - 07Brian McMorrisBelum ada peringkat

- Export Credit Agencies - The Unsung Giants of International Trade and FinanceDokumen207 halamanExport Credit Agencies - The Unsung Giants of International Trade and Financeace187Belum ada peringkat

- Phil. Sugar Estates Dev. Co. v. PoizatDokumen3 halamanPhil. Sugar Estates Dev. Co. v. PoizatElle Mich100% (1)

- The Credit Anstalt Crisis of 1931 Studies in Macroeconomic HistoryDokumen222 halamanThe Credit Anstalt Crisis of 1931 Studies in Macroeconomic HistoryKristoferson BadeaBelum ada peringkat

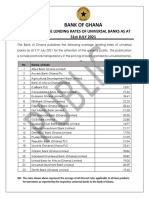

- Average Lending Rates As at July 2021Dokumen1 halamanAverage Lending Rates As at July 2021Fuaad DodooBelum ada peringkat

- 7 Milan V NLRC DigestDokumen2 halaman7 Milan V NLRC DigestJM Ragaza0% (1)

- Business Plan ALGOJODokumen65 halamanBusiness Plan ALGOJOMuhd AmirulBelum ada peringkat

- Summary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFDokumen143 halamanSummary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFJohn StephensBelum ada peringkat

- Assignment On IASDokumen6 halamanAssignment On IASAsif AzadBelum ada peringkat

- SEC V Laigo DigestDokumen3 halamanSEC V Laigo DigestClarence ProtacioBelum ada peringkat

- Model Paper: D (KK D (KK D (KK D (KK D (KK - Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKLDokumen39 halamanModel Paper: D (KK D (KK D (KK D (KK D (KK - Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKL Ys (KK'KKLTezendra SinghBelum ada peringkat

- AccA P4/3.7 - 2002 - Dec - QDokumen12 halamanAccA P4/3.7 - 2002 - Dec - Qroker_m3Belum ada peringkat

- 1-5 To Do An Audit, There Must Be Information in A Verifiable Form and SomeDokumen18 halaman1-5 To Do An Audit, There Must Be Information in A Verifiable Form and Somejulivio mewohBelum ada peringkat

- Project Appraisal - Stages FlowchartDokumen6 halamanProject Appraisal - Stages FlowchartAshokBelum ada peringkat

- Accounting For LeaseDokumen75 halamanAccounting For LeaseRonnie Salazar53% (15)

- Case Dismissals For Lack of Standing To ForecloseDokumen28 halamanCase Dismissals For Lack of Standing To Foreclosejacque zidane100% (1)

- Arceo, Jr. Vs People of The PHDokumen2 halamanArceo, Jr. Vs People of The PHToni CalsadoBelum ada peringkat