Anda mungkin juga menyukai

- Workingpaper 34 NelsonDokumen0 halamanWorkingpaper 34 Nelsonwibisono0323Belum ada peringkat

- Working Paper 3 - The Political Economy of Aceh's Post-Helsinki ReconstructionDokumen34 halamanWorking Paper 3 - The Political Economy of Aceh's Post-Helsinki ReconstructionINFID JAKARTABelum ada peringkat

- Ebook Creative EconomyDokumen266 halamanEbook Creative Economywibisono0323Belum ada peringkat

- Serials Protected FolderDokumen1 halamanSerials Protected Folderwibisono0323Belum ada peringkat

- The Political Economy of Avian Influenza in IndonesiaDokumen67 halamanThe Political Economy of Avian Influenza in Indonesiawibisono0323Belum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- PowerTradeCopier SettingsDokumen13 halamanPowerTradeCopier SettingsEmily MillsBelum ada peringkat

- Mkt501 Final Term Paper 2011 Solved by AfaaqDokumen14 halamanMkt501 Final Term Paper 2011 Solved by AfaaqgreatusamaBelum ada peringkat

- A Beginners Guide To Creating A Digital Marketing StrategyDokumen32 halamanA Beginners Guide To Creating A Digital Marketing StrategyPravin KumarBelum ada peringkat

- Various Types of Mutual Fund Schemes ExplainedDokumen10 halamanVarious Types of Mutual Fund Schemes ExplainedKeyur ShahBelum ada peringkat

- Remodeling Contractor Standard Marketing PlanDokumen39 halamanRemodeling Contractor Standard Marketing PlanPalo Alto Software100% (6)

- Economics Class X Chapter 4 (MBOSE)Dokumen4 halamanEconomics Class X Chapter 4 (MBOSE)M. Amebari NongsiejBelum ada peringkat

- Alternative Investments and StrategiesDokumen414 halamanAlternative Investments and StrategiesJeremiahOmwoyoBelum ada peringkat

- DuPont's DPC Division SaleDokumen8 halamanDuPont's DPC Division SaleTony LuBelum ada peringkat

- Addressing Competition and Driving GrowthDokumen26 halamanAddressing Competition and Driving GrowthNicholas AyeBelum ada peringkat

- IGCSE Edexcel Business Studies NotesDokumen17 halamanIGCSE Edexcel Business Studies NotesEllie Housen0% (1)

- A Project On Dealers Perception On Kajaria Ceramics CoimbatoreDokumen47 halamanA Project On Dealers Perception On Kajaria Ceramics CoimbatoreMohamed SanferBelum ada peringkat

- Financial Management:: Stock ValuationDokumen57 halamanFinancial Management:: Stock ValuationSarah SaluquenBelum ada peringkat

- (Case 10) Walmart and AmazonDokumen7 halaman(Case 10) Walmart and Amazonberliana setyawatiBelum ada peringkat

- Acs 01Dokumen23 halamanAcs 01Astha Srivastava100% (1)

- Predictive MarketsDokumen20 halamanPredictive MarketsAnubhav AggarwalBelum ada peringkat

- Understanding Key Factors in Mango Contractual ArrangementsDokumen13 halamanUnderstanding Key Factors in Mango Contractual ArrangementsAtul sharmaBelum ada peringkat

- Chapter 20 - Options Markets: IntroductionDokumen20 halamanChapter 20 - Options Markets: IntroductionminibodBelum ada peringkat

- Description of Securities and Risks Related To Securities EngDokumen7 halamanDescription of Securities and Risks Related To Securities EngNikhilparakhBelum ada peringkat

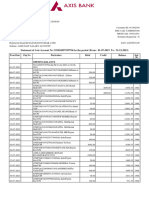

- Account STMT XX9794 31122023Dokumen16 halamanAccount STMT XX9794 31122023shubhamkasyap443Belum ada peringkat

- Management Fundamentals AssignmentDokumen18 halamanManagement Fundamentals Assignmentst57143100% (1)

- CB Insights Tech IPO Pipeline 2019Dokumen38 halamanCB Insights Tech IPO Pipeline 2019Tung NgoBelum ada peringkat

- Investment Analysis and Portfolio Management: Pre-Requisite: None Course ObjectivesDokumen3 halamanInvestment Analysis and Portfolio Management: Pre-Requisite: None Course ObjectivesAmit SrivastavaBelum ada peringkat

- Acc 115 - P2Dokumen9 halamanAcc 115 - P2Riezel PepitoBelum ada peringkat

- Williamson TCE How It Works Where It Is HeadedDokumen36 halamanWilliamson TCE How It Works Where It Is HeadedrevaluerBelum ada peringkat

- Poverty and Reforms - A Case Study For India by Tarun DasDokumen39 halamanPoverty and Reforms - A Case Study For India by Tarun DasProfessor Tarun DasBelum ada peringkat

- The Market: Ubiquitous - EverywhereDokumen1 halamanThe Market: Ubiquitous - EverywhereQueen ValleBelum ada peringkat

- Compound Financial InstrumentDokumen6 halamanCompound Financial InstrumentBeverlene BatiBelum ada peringkat

- How Loyalty Programs Differ Across Top Indian RetailersDokumen29 halamanHow Loyalty Programs Differ Across Top Indian Retailersnitesh kumarBelum ada peringkat

- 300 - Prachet PrakashDokumen3 halaman300 - Prachet PrakashSAURABH RANGARIBelum ada peringkat