Anda mungkin juga menyukai

- China - Price IndicesDokumen1 halamanChina - Price IndicesEduardo PetazzeBelum ada peringkat

- WTI Spot PriceDokumen4 halamanWTI Spot PriceEduardo Petazze100% (1)

- México, PBI 2015Dokumen1 halamanMéxico, PBI 2015Eduardo PetazzeBelum ada peringkat

- Retail Sales in The UKDokumen1 halamanRetail Sales in The UKEduardo PetazzeBelum ada peringkat

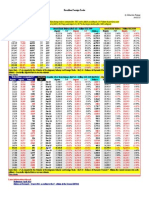

- Brazilian Foreign TradeDokumen1 halamanBrazilian Foreign TradeEduardo PetazzeBelum ada peringkat

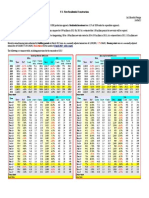

- U.S. New Residential ConstructionDokumen1 halamanU.S. New Residential ConstructionEduardo PetazzeBelum ada peringkat

- Euro Area - Industrial Production IndexDokumen1 halamanEuro Area - Industrial Production IndexEduardo PetazzeBelum ada peringkat

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- JAZEL Resume-2-1-2-1-3-1Dokumen2 halamanJAZEL Resume-2-1-2-1-3-1GirlieJoyGayoBelum ada peringkat

- Guide For Overseas Applicants IRELAND PDFDokumen29 halamanGuide For Overseas Applicants IRELAND PDFJasonLeeBelum ada peringkat

- Loading N Unloading of Tanker PDFDokumen36 halamanLoading N Unloading of Tanker PDFKirtishbose ChowdhuryBelum ada peringkat

- State Immunity Cases With Case DigestsDokumen37 halamanState Immunity Cases With Case DigestsStephanie Dawn Sibi Gok-ong100% (4)

- Ajp Project (1) MergedDokumen22 halamanAjp Project (1) MergedRohit GhoshtekarBelum ada peringkat

- Expense Tracking - How Do I Spend My MoneyDokumen2 halamanExpense Tracking - How Do I Spend My MoneyRenata SánchezBelum ada peringkat

- Selvan CVDokumen4 halamanSelvan CVsuman_civilBelum ada peringkat

- 2021S-EPM 1163 - Day-11-Unit-8 ProcMgmt-AODADokumen13 halaman2021S-EPM 1163 - Day-11-Unit-8 ProcMgmt-AODAehsan ershadBelum ada peringkat

- Check Fraud Running Rampant in 2023 Insights ArticleDokumen4 halamanCheck Fraud Running Rampant in 2023 Insights ArticleJames Brown bitchBelum ada peringkat

- CSEC Jan 2011 Paper 1Dokumen8 halamanCSEC Jan 2011 Paper 1R.D. KhanBelum ada peringkat

- Ces Presentation 08 23 23Dokumen13 halamanCes Presentation 08 23 23api-317062486Belum ada peringkat

- Allan ToddDokumen28 halamanAllan ToddBilly SorianoBelum ada peringkat

- D - MMDA vs. Concerned Residents of Manila BayDokumen13 halamanD - MMDA vs. Concerned Residents of Manila BayMia VinuyaBelum ada peringkat

- A320 Basic Edition Flight TutorialDokumen50 halamanA320 Basic Edition Flight TutorialOrlando CuestaBelum ada peringkat

- 6 V 6 PlexiDokumen8 halaman6 V 6 PlexiFlyinGaitBelum ada peringkat

- SND Kod Dt2Dokumen12 halamanSND Kod Dt2arturshenikBelum ada peringkat

- Government of West Bengal Finance (Audit) Department: NABANNA', HOWRAH-711102 No. Dated, The 13 May, 2020Dokumen2 halamanGovernment of West Bengal Finance (Audit) Department: NABANNA', HOWRAH-711102 No. Dated, The 13 May, 2020Satyaki Prasad MaitiBelum ada peringkat

- A Novel Adoption of LSTM in Customer Touchpoint Prediction Problems Presentation 1Dokumen73 halamanA Novel Adoption of LSTM in Customer Touchpoint Prediction Problems Presentation 1Os MBelum ada peringkat

- Extent of The Use of Instructional Materials in The Effective Teaching and Learning of Home Home EconomicsDokumen47 halamanExtent of The Use of Instructional Materials in The Effective Teaching and Learning of Home Home Economicschukwu solomon75% (4)

- Tivoli Performance ViewerDokumen4 halamanTivoli Performance ViewernaveedshakurBelum ada peringkat

- EnerconDokumen7 halamanEnerconAlex MarquezBelum ada peringkat

- HSBC in A Nut ShellDokumen190 halamanHSBC in A Nut Shelllanpham19842003Belum ada peringkat

- Forecasting of Nonlinear Time Series Using Artificial Neural NetworkDokumen9 halamanForecasting of Nonlinear Time Series Using Artificial Neural NetworkranaBelum ada peringkat

- Oem Functional Specifications For DVAS-2810 (810MB) 2.5-Inch Hard Disk Drive With SCSI Interface Rev. (1.0)Dokumen43 halamanOem Functional Specifications For DVAS-2810 (810MB) 2.5-Inch Hard Disk Drive With SCSI Interface Rev. (1.0)Farhad FarajyanBelum ada peringkat

- HealthInsuranceCertificate-Group CPGDHAB303500662021Dokumen2 halamanHealthInsuranceCertificate-Group CPGDHAB303500662021Ruban JebaduraiBelum ada peringkat

- TSB 120Dokumen7 halamanTSB 120patelpiyushbBelum ada peringkat

- ESG NotesDokumen16 halamanESG Notesdhairya.h22Belum ada peringkat

- Research Article: Finite Element Simulation of Medium-Range Blast Loading Using LS-DYNADokumen10 halamanResearch Article: Finite Element Simulation of Medium-Range Blast Loading Using LS-DYNAAnonymous cgcKzFtXBelum ada peringkat

- Dr. Eduardo M. Rivera: This Is A Riveranewsletter Which Is Sent As Part of Your Ongoing Education ServiceDokumen31 halamanDr. Eduardo M. Rivera: This Is A Riveranewsletter Which Is Sent As Part of Your Ongoing Education ServiceNick FurlanoBelum ada peringkat

- 5 Deming Principles That Help Healthcare Process ImprovementDokumen8 halaman5 Deming Principles That Help Healthcare Process Improvementdewi estariBelum ada peringkat