Anda mungkin juga menyukai

- And Inflation The Role of The Monetary Sector : University of Michigan, AnnDokumen24 halamanAnd Inflation The Role of The Monetary Sector : University of Michigan, AnnShanza KhalidBelum ada peringkat

- Fama 1981Dokumen22 halamanFama 1981Marcelo BalzanaBelum ada peringkat

- (IMF Staff Papers) The Impact of Monetary and Fiscal Policy Under Flexible Exchange Rates and Alternative Expectations StructuresDokumen34 halaman(IMF Staff Papers) The Impact of Monetary and Fiscal Policy Under Flexible Exchange Rates and Alternative Expectations StructuresNida KaradenizBelum ada peringkat

- Stock Market Reaction To Good and Bad Inflation News: Johan Knif James Kolari Seppo PynnönenDokumen42 halamanStock Market Reaction To Good and Bad Inflation News: Johan Knif James Kolari Seppo Pynnönenadnaan_79Belum ada peringkat

- Did Money Cuase The Thing in The 30sDokumen37 halamanDid Money Cuase The Thing in The 30sAndrew XiangBelum ada peringkat

- Money Supply and Stock Prices RelationshipDokumen6 halamanMoney Supply and Stock Prices RelationshipTrinh VtnBelum ada peringkat

- Plakandaras Are 2023Dokumen15 halamanPlakandaras Are 2023Mathias ToulouzeBelum ada peringkat

- TORRECILLASANDJAREO2013Dokumen7 halamanTORRECILLASANDJAREO2013Amalia MegaBelum ada peringkat

- In Ation and Output Dynamics Under Fixed and Flexible Exchange RatesDokumen29 halamanIn Ation and Output Dynamics Under Fixed and Flexible Exchange RatesChi-Wa CWBelum ada peringkat

- A Century of Nominal History in Argentina: Monetary Instability and Non-NeutralitiesDokumen39 halamanA Century of Nominal History in Argentina: Monetary Instability and Non-NeutralitiesignacioBelum ada peringkat

- Modeling The Philips Curve: A Time-Varying Volatility ApproachDokumen18 halamanModeling The Philips Curve: A Time-Varying Volatility ApproachOladipupo Mayowa PaulBelum ada peringkat

- Rakesh%20paper 1Dokumen24 halamanRakesh%20paper 1rifatBelum ada peringkat

- Monetary Cycles, Financial Cycles, and The Business Cycle: AbstractDokumen18 halamanMonetary Cycles, Financial Cycles, and The Business Cycle: AbstractMichael MarlerBelum ada peringkat

- Comparative Economic ResearchDokumen26 halamanComparative Economic ResearchdanoshkenBelum ada peringkat

- Final Term Paper 3Dokumen21 halamanFinal Term Paper 3Stanley NgacheBelum ada peringkat

- 024 Article A005 enDokumen31 halaman024 Article A005 enLucca TorresBelum ada peringkat

- Inflation, Financial Markets and Long-Run Real Activity: Elisabeth Huybens, Bruce D. SmithDokumen33 halamanInflation, Financial Markets and Long-Run Real Activity: Elisabeth Huybens, Bruce D. SmithSamuel Mulu SahileBelum ada peringkat

- Cfmdp2013 01 PaperDokumen30 halamanCfmdp2013 01 PaperAdminAliBelum ada peringkat

- Are The Effects of Monetary Policy Asymmetric?Dokumen27 halamanAre The Effects of Monetary Policy Asymmetric?marhelunBelum ada peringkat

- Study of Impact of Mutual Fund Flow on Market VolatilityDokumen46 halamanStudy of Impact of Mutual Fund Flow on Market VolatilityBhavya_patibandlaBelum ada peringkat

- Bank STK RT Andmoney Supply US StdyDokumen36 halamanBank STK RT Andmoney Supply US Stdysagarg94gmailcomBelum ada peringkat

- The Impact of Inflation Uncertainty On Interest Rates in The UkDokumen12 halamanThe Impact of Inflation Uncertainty On Interest Rates in The UkLorence Dominic NarciseBelum ada peringkat

- Darby 1975Dokumen11 halamanDarby 1975Syed Aal-e RazaBelum ada peringkat

- Bis Financial VolDokumen15 halamanBis Financial VolmeetwithsanjayBelum ada peringkat

- 3 Cycles Fedny 2010 Sr421Dokumen20 halaman3 Cycles Fedny 2010 Sr421Jayanthi KandhaadaiBelum ada peringkat

- Why Does The Yield Curve Predict Output and Inflation?Dokumen47 halamanWhy Does The Yield Curve Predict Output and Inflation?indrakuBelum ada peringkat

- Contagio Markt GDPDokumen55 halamanContagio Markt GDPrrrrBelum ada peringkat

- Wages, Prices and EmploymentDokumen9 halamanWages, Prices and Employmenttalha hasibBelum ada peringkat

- Bayou Mi 1996Dokumen28 halamanBayou Mi 1996Serban CristiBelum ada peringkat

- Does Stock Returns Protect Investors Against Inflation in NigeriaDokumen10 halamanDoes Stock Returns Protect Investors Against Inflation in NigeriaAlexander DeckerBelum ada peringkat

- NeutralDokumen55 halamanNeutralГанболд БЯМБАДАЛАЙBelum ada peringkat

- Relationship Between A Components of Money Demand Function and General Index of A Stock MarketDokumen2 halamanRelationship Between A Components of Money Demand Function and General Index of A Stock MarketNabeel Mahdi AljanabiBelum ada peringkat

- The Journal of Finance - December 1993 - GLOSTEN - On The Relation Between The Expected Value and The Volatility of TheDokumen23 halamanThe Journal of Finance - December 1993 - GLOSTEN - On The Relation Between The Expected Value and The Volatility of Theisabella oliveiraBelum ada peringkat

- Money, Prices, Interest Rates and The Business CycleDokumen88 halamanMoney, Prices, Interest Rates and The Business CycleerererehgjdsassdfBelum ada peringkat

- Global Finance and MacroeconomyDokumen10 halamanGlobal Finance and MacroeconomyAdison BrilleBelum ada peringkat

- The Relationship Between Stock Market Volatility and Macro Economic VolatilityDokumen12 halamanThe Relationship Between Stock Market Volatility and Macro Economic VolatilitygodotwhocomesBelum ada peringkat

- Asymmetries in Monetary PolicyDokumen31 halamanAsymmetries in Monetary PolicyAndré Cordeiro ValérioBelum ada peringkat

- Uncertainty in Financial Markets and Business CyclesDokumen30 halamanUncertainty in Financial Markets and Business CyclesOre.ABelum ada peringkat

- Interest Rates and Inflation: Federal Reserve Bank of Minneapolis Research DepartmentDokumen19 halamanInterest Rates and Inflation: Federal Reserve Bank of Minneapolis Research DepartmentHarshit JainBelum ada peringkat

- The Mckinnon-Shaw Hypothesis: Thirty Years On: A Review of Recent Developments in Financial Liberalization Theory by DR Firdu Gemech and Professor John StruthersDokumen25 halamanThe Mckinnon-Shaw Hypothesis: Thirty Years On: A Review of Recent Developments in Financial Liberalization Theory by DR Firdu Gemech and Professor John Struthersbabstar999Belum ada peringkat

- NathanDokumen10 halamanNathanzht00374Belum ada peringkat

- Milton FDokumen26 halamanMilton Fjd1754Belum ada peringkat

- A Cointegrated Structural VAR Model of The Canadian Economy: William J. Crowder Mark E. WoharDokumen38 halamanA Cointegrated Structural VAR Model of The Canadian Economy: William J. Crowder Mark E. WoharRodrigoBelum ada peringkat

- Literature Review On Inflation and Stock ReturnsDokumen6 halamanLiterature Review On Inflation and Stock Returnsafdtvuzih100% (1)

- The Effects of Monetary Policy On Stock Market Bubbles: Some EvidenceDokumen25 halamanThe Effects of Monetary Policy On Stock Market Bubbles: Some Evidencemaria ianBelum ada peringkat

- QR1232Dokumen12 halamanQR1232postscriptBelum ada peringkat

- Danielsson ValenzuelaDokumen42 halamanDanielsson ValenzuelakabbalahhBelum ada peringkat

- Monetory Ploicy Stock Return and InflationDokumen19 halamanMonetory Ploicy Stock Return and InflationJohnBelum ada peringkat

- Inflation and The Size of GovernmentDokumen44 halamanInflation and The Size of GovernmentTBP_Think_TankBelum ada peringkat

- The Impact of Inflation On Capital Budgeting and Working CapitalDokumen9 halamanThe Impact of Inflation On Capital Budgeting and Working CapitalNaga SreenivasBelum ada peringkat

- K Iguel 1989Dokumen11 halamanK Iguel 1989Ramiro ManiniBelum ada peringkat

- Conflict Inflation, Distribution, Cyclical Accumaulation and CrisesDokumen19 halamanConflict Inflation, Distribution, Cyclical Accumaulation and CrisesRicardo CaffeBelum ada peringkat

- Interest Rates and The Commodity PricesDokumen54 halamanInterest Rates and The Commodity Prices1aqualeoBelum ada peringkat

- The Fed and Stock Market: A Proxy and Instrumental Variable IdentificationDokumen34 halamanThe Fed and Stock Market: A Proxy and Instrumental Variable IdentificationcastjamBelum ada peringkat

- Monetary policy's long-run effects on output and productivityDokumen57 halamanMonetary policy's long-run effects on output and productivityPland SpringBelum ada peringkat

- NBER Macroeconomics Annual 2013: Volume 28Dari EverandNBER Macroeconomics Annual 2013: Volume 28Jonathan A. ParkerBelum ada peringkat

- NBER Macroeconomics Annual 2016Dari EverandNBER Macroeconomics Annual 2016Martin EichenbaumBelum ada peringkat

- An Interesting Theory -Why Interest Rates are Important but not for the Reasons Commonly AssumedDari EverandAn Interesting Theory -Why Interest Rates are Important but not for the Reasons Commonly AssumedBelum ada peringkat

- NBER Macroeconomics Annual 2014: Volume 29Dari EverandNBER Macroeconomics Annual 2014: Volume 29Jonathan A. ParkerBelum ada peringkat

- Reliance Press Release-JuneDokumen9 halamanReliance Press Release-Junenakarani39Belum ada peringkat

- Printed Textile XII - 778Dokumen140 halamanPrinted Textile XII - 778nakarani39Belum ada peringkat

- Modern Baby NamesDokumen226 halamanModern Baby Namesnakarani39Belum ada peringkat

- NamesDokumen245 halamanNamesnakarani39Belum ada peringkat

- Treasure Island TDokumen330 halamanTreasure Island TpenolBelum ada peringkat

- GNI Per Capita, PPP (Current International $) Population (Total) GDP (Current US$) GDP Growth (Annual %) Life Expectancy at Birth, Total (Years)Dokumen1 halamanGNI Per Capita, PPP (Current International $) Population (Total) GDP (Current US$) GDP Growth (Annual %) Life Expectancy at Birth, Total (Years)nakarani39Belum ada peringkat

- Historicname tcm77-254032Dokumen8 halamanHistoricname tcm77-254032nakarani39Belum ada peringkat

- Uncovering The Risk-Return Relation in The Stock Market: Working Paper SeriesDokumen43 halamanUncovering The Risk-Return Relation in The Stock Market: Working Paper Seriesnakarani39Belum ada peringkat

- Effects of Crude Oil Price Changes On Sector Indices of Istanbul Stock ExchangeDokumen16 halamanEffects of Crude Oil Price Changes On Sector Indices of Istanbul Stock Exchangenakarani39Belum ada peringkat

- Pepsico Human Rights Workplace Policy: DefinitionsDokumen1 halamanPepsico Human Rights Workplace Policy: Definitionsnakarani39Belum ada peringkat

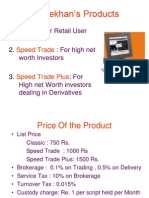

- Sharekhan Products GuideDokumen19 halamanSharekhan Products Guidenakarani39Belum ada peringkat

- Pepsico Environmental Policy: Sustainability VisionDokumen1 halamanPepsico Environmental Policy: Sustainability Visionnakarani39Belum ada peringkat

- Multiple Regression AnalysisDokumen75 halamanMultiple Regression AnalysisMira100% (1)

- AMOS - Analysis of Moment Structures: HIV Prevention Center University of KentuckyDokumen83 halamanAMOS - Analysis of Moment Structures: HIV Prevention Center University of KentuckynprakashmbaBelum ada peringkat

- Statistics Beginners GuideDokumen42 halamanStatistics Beginners GuideAhmad MakhloufBelum ada peringkat

- Problem Set 1: Introduction To R - Solutions With R Output: 1 Install PackagesDokumen24 halamanProblem Set 1: Introduction To R - Solutions With R Output: 1 Install PackagesDarnell LarsenBelum ada peringkat

- Improving Global Seismic Event Locations Using Source-Receiver ReciprocityDokumen10 halamanImproving Global Seismic Event Locations Using Source-Receiver Reciprocitymanuelflorez1102Belum ada peringkat

- Econometric Analysis of Panel DataDokumen14 halamanEconometric Analysis of Panel Data1111111111111-859751Belum ada peringkat

- Impact of Green Marketing On Consumer Buying Behaviour: VOL: 13, January, 2016Dokumen7 halamanImpact of Green Marketing On Consumer Buying Behaviour: VOL: 13, January, 2016DEVINA GURRIAHBelum ada peringkat

- 2421 9648 1 PBDokumen10 halaman2421 9648 1 PBAndres Josia AgadivaBelum ada peringkat

- The Importance of University Facilities For Student Satisfaction at A Norwegian UniversityDokumen18 halamanThe Importance of University Facilities For Student Satisfaction at A Norwegian UniversityMinh TrangBelum ada peringkat

- Spatial Regression Analysis of Poverty DataDokumen27 halamanSpatial Regression Analysis of Poverty DataUp ToyouBelum ada peringkat

- Asme PTC 4 - 2008Dokumen4 halamanAsme PTC 4 - 2008KristianBelum ada peringkat

- Impact of Social Media On Self EsteemDokumen14 halamanImpact of Social Media On Self EsteemCedrik Pardillo MaageBelum ada peringkat

- MPH SyllabusDokumen79 halamanMPH SyllabusMuhammad AsifBelum ada peringkat

- Kayitesi Claudine Final ThesisDokumen90 halamanKayitesi Claudine Final ThesisAlfonso Joel GonzalesBelum ada peringkat

- Ncaa ML CompetitionDokumen24 halamanNcaa ML Competitionapi-462457883Belum ada peringkat

- Statisitics Project 3Dokumen22 halamanStatisitics Project 3AMAN PRAKASHBelum ada peringkat

- Journal of The American Statistical AssociationDokumen28 halamanJournal of The American Statistical AssociationjfverhelstBelum ada peringkat

- Jeffrey M. Wooldridge-Introductory Econometrics - A Modern Approach-South-Western College Pub (2016) - 113-115Dokumen3 halamanJeffrey M. Wooldridge-Introductory Econometrics - A Modern Approach-South-Western College Pub (2016) - 113-115Putri Windya DewiBelum ada peringkat

- Tutorial On Multivariate Logistic Regression: Javier R. Movellan July 23, 2006Dokumen9 halamanTutorial On Multivariate Logistic Regression: Javier R. Movellan July 23, 2006Vu Duc Hoang VoBelum ada peringkat

- Comparison of Rainfall Interpolation Methods in ADokumen14 halamanComparison of Rainfall Interpolation Methods in AAnteneh W. LemmaBelum ada peringkat

- Paper TQC PDFDokumen23 halamanPaper TQC PDFNgọc LiễuBelum ada peringkat

- MBA Business Statistics 2021Dokumen9 halamanMBA Business Statistics 2021seyon sithamparanathanBelum ada peringkat

- Six Sigma Tools in A Excel SheetDokumen23 halamanSix Sigma Tools in A Excel SheetjohnavramBelum ada peringkat

- Advanced statistical methods in medicineDokumen63 halamanAdvanced statistical methods in medicinerakeshnandiymailBelum ada peringkat

- Statistics Project Report PGDM FinalDokumen45 halamanStatistics Project Report PGDM FinalSoham KhannaBelum ada peringkat

- Impact of Training and Development On Employee Performance: A Comparative Study On Select Banks in Sultanate of OmanDokumen6 halamanImpact of Training and Development On Employee Performance: A Comparative Study On Select Banks in Sultanate of OmanTanveer ImdadBelum ada peringkat

- Week 4 - Cont. Week 3 Slides - UpdatedDokumen43 halamanWeek 4 - Cont. Week 3 Slides - UpdatedSin TungBelum ada peringkat

- What is EconometricsDokumen26 halamanWhat is EconometricsMunnah BhaiBelum ada peringkat

- Research Methods For EngineeringDokumen89 halamanResearch Methods For EngineeringadBelum ada peringkat

- Final Exam Analysis ANLY 502Dokumen8 halamanFinal Exam Analysis ANLY 502Vatsal PatelBelum ada peringkat