Anda mungkin juga menyukai

- Notes On National IncomeDokumen9 halamanNotes On National IncomesaravananBelum ada peringkat

- Income Tax Calculator For F.Y 2020 21 A.Y 2021 22 ArthikDishaDokumen7 halamanIncome Tax Calculator For F.Y 2020 21 A.Y 2021 22 ArthikDishaSARAVANAN PBelum ada peringkat

- PRTC - TAX-Final PB - May 2022Dokumen16 halamanPRTC - TAX-Final PB - May 2022Luna VBelum ada peringkat

- Fast-Track Tax Reform: Lessons from the MaldivesDari EverandFast-Track Tax Reform: Lessons from the MaldivesBelum ada peringkat

- TEST BANK Cost Accounting 14E by Carter Ch08 TEST BANK Cost Accounting 14E by Carter Ch08Dokumen16 halamanTEST BANK Cost Accounting 14E by Carter Ch08 TEST BANK Cost Accounting 14E by Carter Ch08mEOW SBelum ada peringkat

- Trends in The 21st. Century Cosmetic IndustryDokumen9 halamanTrends in The 21st. Century Cosmetic IndustryBasil FletcherBelum ada peringkat

- Iligan City - Seminar On TRAIn Law For Students - 05 03 18Dokumen195 halamanIligan City - Seminar On TRAIn Law For Students - 05 03 18Lorainne AjocBelum ada peringkat

- Entrep10 Q4 Module1 Monitoring and Evaluating Business Operations Week 1 Week 4Dokumen45 halamanEntrep10 Q4 Module1 Monitoring and Evaluating Business Operations Week 1 Week 4claire jeannees inductivoBelum ada peringkat

- 35 Income Tax Chart 2009 2010Dokumen1 halaman35 Income Tax Chart 2009 2010Piyush MishraBelum ada peringkat

- Train Law PhilippinesDokumen64 halamanTrain Law PhilippinesThe BeatlessBelum ada peringkat

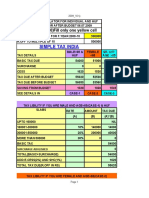

- Simple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellDokumen4 halamanSimple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellPradip ShawBelum ada peringkat

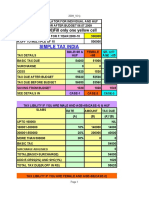

- Simple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellDokumen4 halamanSimple Tax India: (F.YEAR 2009-10) Fill Only One Yellow CellRaj PatilBelum ada peringkat

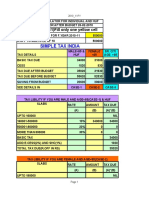

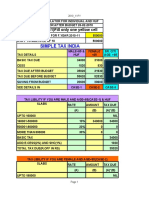

- Tax Calculator AY 09-10Dokumen4 halamanTax Calculator AY 09-10madhuamsBelum ada peringkat

- Amma Income TaxDokumen5 halamanAmma Income Taxraghuraman1511Belum ada peringkat

- Direct Tax Rates For Last 11 Assessment YearsDokumen4 halamanDirect Tax Rates For Last 11 Assessment YearsValera HardikBelum ada peringkat

- Ques. Defered TaxDokumen40 halamanQues. Defered TaxKALYANI JAYAKRISHNAN 2022155Belum ada peringkat

- Income Tax Ready Reckoner PDFDokumen15 halamanIncome Tax Ready Reckoner PDFtushar sharmaBelum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11subhodattBelum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11bablooraiBelum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11dhuvad.2004Belum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11Ravi ChandraBelum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11Priyanshu SharmaBelum ada peringkat

- Tax Calculator 2010-11Dokumen4 halamanTax Calculator 2010-11Syam ReddyBelum ada peringkat

- SGV Train LawDokumen149 halamanSGV Train LawEm-em CantosBelum ada peringkat

- 5 6170280447000445052 PDFDokumen358 halaman5 6170280447000445052 PDFmanoj mohanBelum ada peringkat

- DT May 23 in 50 PagesDokumen15 halamanDT May 23 in 50 PagesShivaji hariBelum ada peringkat

- (##-See Rebate) : 1st Year 2nd Year 3rd Year 4th Year 5th Year 6th YearDokumen1 halaman(##-See Rebate) : 1st Year 2nd Year 3rd Year 4th Year 5th Year 6th YearMita SethiBelum ada peringkat

- Double TaxationDokumen10 halamanDouble TaxationMintuBelum ada peringkat

- Income Tax Ready Reckoner - Budget 2023-1Dokumen14 halamanIncome Tax Ready Reckoner - Budget 2023-1ಸೊಹನ್ ಕಲಂಗುಟ್ಕರ್Belum ada peringkat

- Train by SGV ColorDokumen32 halamanTrain by SGV ColorFlorenz AmbasBelum ada peringkat

- 1 BTAXREV Week 2 Income TaxationDokumen48 halaman1 BTAXREV Week 2 Income TaxationgatotkaBelum ada peringkat

- Train Final Ver A 1.25.2018Dokumen89 halamanTrain Final Ver A 1.25.2018Careyssa MaeBelum ada peringkat

- Manila Cavite Laguna Cebu Cagayan de Oro DavaoDokumen3 halamanManila Cavite Laguna Cebu Cagayan de Oro DavaoTatianaBelum ada peringkat

- .Apr 2022Dokumen10 halaman.Apr 2022SWAPNIL JADHAVBelum ada peringkat

- Sol 1Dokumen1 halamanSol 1alex breymannBelum ada peringkat

- Tax CalculatorDokumen2 halamanTax CalculatoramitBelum ada peringkat

- Finance&Accounts T3 SolutionDokumen4 halamanFinance&Accounts T3 Solutionkanika thakurBelum ada peringkat

- Group 6 Tax AssignmentDokumen14 halamanGroup 6 Tax Assignmentdianaowani2Belum ada peringkat

- Tax Audit Limit & Tax RatesDokumen6 halamanTax Audit Limit & Tax RatesPhani SankaraBelum ada peringkat

- Case Study 1 SolutionDokumen2 halamanCase Study 1 Solutiongaurilakhmani2003Belum ada peringkat

- 5652 20190806194323 Chart It 19Dokumen1 halaman5652 20190806194323 Chart It 19arti chowdhryBelum ada peringkat

- 5652 20190806194323 Chart It 19Dokumen1 halaman5652 20190806194323 Chart It 19arti chowdhryBelum ada peringkat

- IT Calculation New RegimeDokumen4 halamanIT Calculation New Regimeyelrihs23Belum ada peringkat

- CH 01 SMDokumen10 halamanCH 01 SMarm195148Belum ada peringkat

- Tax Final Exam Practice Material - CompressDokumen10 halamanTax Final Exam Practice Material - CompressNovemae CollamatBelum ada peringkat

- Tax CalculatorDokumen3 halamanTax CalculatorRohit KumarBelum ada peringkat

- (Train) : Taxchanges U Need To KnowDokumen27 halaman(Train) : Taxchanges U Need To KnowNoel DomingoBelum ada peringkat

- Model Solution: Page 1 of 6Dokumen6 halamanModel Solution: Page 1 of 6ShuvonathBelum ada peringkat

- MCQs All Sets F 1Dokumen46 halamanMCQs All Sets F 1PSK WRITINGSBelum ada peringkat

- India Budget Highlights Finance Bill, 2021Dokumen861 halamanIndia Budget Highlights Finance Bill, 2021vaishnavi aBelum ada peringkat

- V6 After Budget 2023 New Tax Regime Vs Old Tax RegimeDokumen20 halamanV6 After Budget 2023 New Tax Regime Vs Old Tax RegimegunagaliBelum ada peringkat

- Kotak PL One PagerDokumen1 halamanKotak PL One Pagerhetalahir149Belum ada peringkat

- 706 - Summary - of - CAPITAL - GAINS - Including PDFDokumen31 halaman706 - Summary - of - CAPITAL - GAINS - Including PDFSurekha BonagiriBelum ada peringkat

- Union Budget-2020-21 New Tax Rates Vs Existing Tax Rates For IndividualDokumen2 halamanUnion Budget-2020-21 New Tax Rates Vs Existing Tax Rates For IndividualCA Upendra Singh ThakurBelum ada peringkat

- Jorg R. MenesesDokumen3 halamanJorg R. MenesesKevin JugaoBelum ada peringkat

- Issues in Capital Budgeting: 9-1 Project Investment NPV PIDokumen6 halamanIssues in Capital Budgeting: 9-1 Project Investment NPV PILyam Cruz FernandezBelum ada peringkat

- Amendments DT 2016Dokumen70 halamanAmendments DT 2016dbp9050Belum ada peringkat

- Ernst & Young On How The Budget 2010 Will Affect Individuals and BusinessesDokumen6 halamanErnst & Young On How The Budget 2010 Will Affect Individuals and Businessesrainaz07Belum ada peringkat

- Tax Rates CompilationDokumen1 halamanTax Rates Compilationarunvaleraphotos2023Belum ada peringkat

- Tax Changes You Need To Know Under RA 10963Dokumen20 halamanTax Changes You Need To Know Under RA 10963Rosanno DavidBelum ada peringkat

- Ethiopian Tax SystemDokumen26 halamanEthiopian Tax SystemAsfaw WossenBelum ada peringkat

- Tax Calculations1246345Dokumen22 halamanTax Calculations1246345AkshayBelum ada peringkat

- CS Executive Tax Laws Amendments by Vipul ShahDokumen41 halamanCS Executive Tax Laws Amendments by Vipul ShahCloxan India Pvt LtdBelum ada peringkat

- Chapter 14: Financial Ratios and Firm PerformanceDokumen43 halamanChapter 14: Financial Ratios and Firm Performancebano0otaBelum ada peringkat

- Gesco Kabab: Worksheet For The Month Ended in December 31, 2021Dokumen20 halamanGesco Kabab: Worksheet For The Month Ended in December 31, 2021TanjinBelum ada peringkat

- Chap 5 Prob 1 3Dokumen10 halamanChap 5 Prob 1 3Nyster Ann RebenitoBelum ada peringkat

- NIIR List of DatabasesDokumen61 halamanNIIR List of DatabasesRITESH RATHODBelum ada peringkat

- GGCADokumen2 halamanGGCAPrakash BaldaniyaBelum ada peringkat

- Toaz - Info Prelim Midterm PRDokumen98 halamanToaz - Info Prelim Midterm PRClandestine SoulBelum ada peringkat

- Intermediate Course Study Material: TaxationDokumen31 halamanIntermediate Course Study Material: Taxationtauseefalam917Belum ada peringkat

- Business Statistics Project:: TiruchirappalliDokumen21 halamanBusiness Statistics Project:: TiruchirappalliGunjan ChandavatBelum ada peringkat

- Trial Balance - Trial Balance Year End of 2020Dokumen2 halamanTrial Balance - Trial Balance Year End of 2020Zoe Vera S. AcainBelum ada peringkat

- F7 SMART Notes ACCADokumen41 halamanF7 SMART Notes ACCAzemy jacksonBelum ada peringkat

- SM Chap013Dokumen6 halamanSM Chap013Nicky 'Zing' NguyenBelum ada peringkat

- Kidusan Amha Mbao-6074-15A FMA Assignment-11111Dokumen13 halamanKidusan Amha Mbao-6074-15A FMA Assignment-11111Kidusan AmhaBelum ada peringkat

- Macro Environment Factor of Business in BangladeshDokumen6 halamanMacro Environment Factor of Business in BangladeshRasel RazBelum ada peringkat

- NIM: 2440007043 Nama: Ni Putu Young Yenyuo A Mata Kuliah: Accounting For Business Dosen: Herlin Tundjung SetijaningsihDokumen5 halamanNIM: 2440007043 Nama: Ni Putu Young Yenyuo A Mata Kuliah: Accounting For Business Dosen: Herlin Tundjung SetijaningsihiyeBelum ada peringkat

- Chapter 5 Income Tax On CorporationsDokumen96 halamanChapter 5 Income Tax On Corporationschavezcelvia18Belum ada peringkat

- Walmart Financial AnalysisDokumen187 halamanWalmart Financial AnalysisKareem L SayidBelum ada peringkat

- CMKTQT HGDokumen32 halamanCMKTQT HGGiang Thái HươngBelum ada peringkat

- Payroll Period of August 2022Dokumen1 halamanPayroll Period of August 2022ImranBelum ada peringkat

- Transaction Analysis-Ch-1 Session 2, 3 4Dokumen17 halamanTransaction Analysis-Ch-1 Session 2, 3 4rj OpuBelum ada peringkat

- VF L10 Eng 2021Dokumen24 halamanVF L10 Eng 2021SindyBelum ada peringkat

- DD-2043 (SE) : Roll No. .Dokumen6 halamanDD-2043 (SE) : Roll No. .Manohar SumathiBelum ada peringkat

- Antonio MolinaDokumen11 halamanAntonio MolinaJacob Bataqueg100% (1)

- Cs Executive Tax Question Bank Dec 23 & 2024 CA Saumil ManglaniDokumen282 halamanCs Executive Tax Question Bank Dec 23 & 2024 CA Saumil ManglaniPoonam SINGHBelum ada peringkat

- EAE 313 AEC 307 PUBLIC FINANCE fINAL (2) - 1-1-2Dokumen150 halamanEAE 313 AEC 307 PUBLIC FINANCE fINAL (2) - 1-1-2Teddy jeremyBelum ada peringkat

- Acronyms, Abbreviations and Notations Used in EconomicsDokumen8 halamanAcronyms, Abbreviations and Notations Used in EconomicsSylvainBelum ada peringkat

- Taylor NZ CaseDokumen60 halamanTaylor NZ CaseSarthak ChaturvediBelum ada peringkat