Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Compensation of General Partners of Private Equity FundsDokumen6 halamanCompensation of General Partners of Private Equity FundsManu Midha100% (1)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Finance Module 1 Intro To FinanceDokumen8 halamanFinance Module 1 Intro To FinanceJOHN PAUL LAGAOBelum ada peringkat

- Historical Volatility - The Holy Grail Found PDFDokumen5 halamanHistorical Volatility - The Holy Grail Found PDFAndrey Yablonskiy100% (5)

- Audit of Banks With The Help of FinacleDokumen8 halamanAudit of Banks With The Help of FinacleKartikey RanaBelum ada peringkat

- State Audit Code of The Philippines (P.D. 1445)Dokumen37 halamanState Audit Code of The Philippines (P.D. 1445)Monique del Rosario100% (3)

- CIR v. Suyoc MinesDokumen1 halamanCIR v. Suyoc MinesPatricia SulitBelum ada peringkat

- Reliance Industries Financial Report AnalysisDokumen52 halamanReliance Industries Financial Report Analysissagar029Belum ada peringkat

- OffentliggorelseDokumen59 halamanOffentliggorelsenot youBelum ada peringkat

- Journal On FACTORS AFFECTING VOLUNTARY COMPLIANCE PDFDokumen16 halamanJournal On FACTORS AFFECTING VOLUNTARY COMPLIANCE PDFFasika AbedomBelum ada peringkat

- RBI Master Circular On RestructuringDokumen120 halamanRBI Master Circular On RestructuringHarish PuriBelum ada peringkat

- Chapter 1+3+4 AhtDokumen25 halamanChapter 1+3+4 AhtAn Hoài ThuBelum ada peringkat

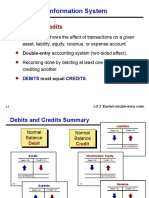

- Accounting Information System Debits and CreditsDokumen84 halamanAccounting Information System Debits and CreditsDavid Bradley BeckBelum ada peringkat

- Company Research Highlights: Plug Power IncDokumen4 halamanCompany Research Highlights: Plug Power Incapi-109061352Belum ada peringkat

- CA Final DT Q MTP 2 Nov23 Castudynotes ComDokumen10 halamanCA Final DT Q MTP 2 Nov23 Castudynotes ComRajdeep GuptaBelum ada peringkat

- 2281 w05 QP 1Dokumen12 halaman2281 w05 QP 1mstudy123456Belum ada peringkat

- Walmart Financial Ratio Analysis 2002-2003Dokumen1 halamanWalmart Financial Ratio Analysis 2002-2003Pamela WilliamsBelum ada peringkat

- Working Capital Project Report 2Dokumen48 halamanWorking Capital Project Report 2Evelyn KeaneBelum ada peringkat

- Economics Chapter 2 14Dokumen84 halamanEconomics Chapter 2 14Jarren BasilanBelum ada peringkat

- FSA On Infy With InterpretationDokumen22 halamanFSA On Infy With InterpretationayushBelum ada peringkat

- Income Taxation Chapter 14 SolutionsDokumen2 halamanIncome Taxation Chapter 14 SolutionsEBelum ada peringkat

- Cost Benefit AnalysisDokumen11 halamanCost Benefit AnalysisTnek OrarrefBelum ada peringkat

- John Case WorksheetDokumen10 halamanJohn Case Worksheetzeeshan33% (3)

- Intermediate Accounting I IntangiblesDokumen7 halamanIntermediate Accounting I IntangiblesGiny BenavidezBelum ada peringkat

- Cre8 Corp's Organizational StructureDokumen5 halamanCre8 Corp's Organizational StructureJhobelle JovellanoBelum ada peringkat

- Financial Management - Formula SheetDokumen8 halamanFinancial Management - Formula SheetHassleBustBelum ada peringkat

- Learning ObjectivesDokumen10 halamanLearning ObjectivesShraddha MalandkarBelum ada peringkat

- Audit Points Treasury Bills SystemDokumen37 halamanAudit Points Treasury Bills SystemRajaniseer SrinivasanBelum ada peringkat

- Actual Costing enDokumen8 halamanActual Costing enRajanBelum ada peringkat

- Individual Income Tax NOTESDokumen1 halamanIndividual Income Tax NOTESNavsBelum ada peringkat