Anda mungkin juga menyukai

- EIB Investment Report 2021/2022 - Key findings: Recovery as a springboard for changeDari EverandEIB Investment Report 2021/2022 - Key findings: Recovery as a springboard for changeBelum ada peringkat

- Latvia Long-Term Rating Raised To 'A-' On Strong Growth and Fiscal Performance Outlook StableDokumen8 halamanLatvia Long-Term Rating Raised To 'A-' On Strong Growth and Fiscal Performance Outlook Stableapi-228714775Belum ada peringkat

- EIB Working Papers 2019/08 - Investment: What holds Romanian firms back?Dari EverandEIB Working Papers 2019/08 - Investment: What holds Romanian firms back?Belum ada peringkat

- Republic of Poland Ratings Affirmed Outlook Stable: Research UpdateDokumen8 halamanRepublic of Poland Ratings Affirmed Outlook Stable: Research Updateapi-228714775Belum ada peringkat

- Portugal 'BB/B' Ratings Affirmed Outlook Negative On Policy UncertaintyDokumen9 halamanPortugal 'BB/B' Ratings Affirmed Outlook Negative On Policy Uncertaintyapi-231665846Belum ada peringkat

- Outlook On Finland Revised To Negative On Subpar Growth Prospects 'AAA/A-1+' Ratings AffirmedDokumen8 halamanOutlook On Finland Revised To Negative On Subpar Growth Prospects 'AAA/A-1+' Ratings Affirmedapi-231665846Belum ada peringkat

- Polish Banking Sector Outlook 2014: Brighter Prospects Ahead As Economic and Operating Pressures RecedeDokumen16 halamanPolish Banking Sector Outlook 2014: Brighter Prospects Ahead As Economic and Operating Pressures Recedeapi-228714775Belum ada peringkat

- Greece Ratings Affirmed at 'B-/B' Outlook Stable: Research UpdateDokumen8 halamanGreece Ratings Affirmed at 'B-/B' Outlook Stable: Research Updateapi-228714775Belum ada peringkat

- Recovery For Central and Eastern European Banks Will Be Fragile in 2014Dokumen14 halamanRecovery For Central and Eastern European Banks Will Be Fragile in 2014api-228714775Belum ada peringkat

- Romania: Letter of Intent, Memorandum of Economic and FinancialDokumen36 halamanRomania: Letter of Intent, Memorandum of Economic and FinancialFlorin CituBelum ada peringkat

- Q&A: What Are The Risks Ahead For European Sovereign Ratings in 2014?Dokumen11 halamanQ&A: What Are The Risks Ahead For European Sovereign Ratings in 2014?api-228714775Belum ada peringkat

- Moodys Iceland July 2013 NewDokumen20 halamanMoodys Iceland July 2013 NewTeddy JainBelum ada peringkat

- Outlook On Portugal Revised To Stable From Negative On Economic and Fiscal Stabilization 'BB/B' Ratings AffirmedDokumen9 halamanOutlook On Portugal Revised To Stable From Negative On Economic and Fiscal Stabilization 'BB/B' Ratings Affirmedapi-228714775Belum ada peringkat

- Ratings On Spain Affirmed at 'BBB-/A-3' Outlook Negative: Research UpdateDokumen6 halamanRatings On Spain Affirmed at 'BBB-/A-3' Outlook Negative: Research Updateapi-227433089Belum ada peringkat

- Atvia Etter of NtentDokumen26 halamanAtvia Etter of NtentZerohedgeBelum ada peringkat

- STANDARD - PORTUGAL - 27april2010Dokumen5 halamanSTANDARD - PORTUGAL - 27april2010Maria Alvares RibeiroBelum ada peringkat

- Seb Merchant Banking - Country Risk Analysis 28 September 2016Dokumen6 halamanSeb Merchant Banking - Country Risk Analysis 28 September 2016Aylin PolatBelum ada peringkat

- Romania 'BBB - A-3' Ratings Affirmed - Outlook Stab - S&P Global Ratings - 12.04.2024Dokumen22 halamanRomania 'BBB - A-3' Ratings Affirmed - Outlook Stab - S&P Global Ratings - 12.04.2024Florin BudescuBelum ada peringkat

- Flash Comment: Latvia - February 11, 2013Dokumen1 halamanFlash Comment: Latvia - February 11, 2013Swedbank AB (publ)Belum ada peringkat

- Romania Upgraded To 'BBB-/A-3' On Pace of External Adjustments Outlook StableDokumen7 halamanRomania Upgraded To 'BBB-/A-3' On Pace of External Adjustments Outlook Stableapi-228714775Belum ada peringkat

- Policy Easing To Accelerate in H1: China Outlook 2012Dokumen21 halamanPolicy Easing To Accelerate in H1: China Outlook 2012valentinaivBelum ada peringkat

- Country Intelligence Report 2Dokumen34 halamanCountry Intelligence Report 2Li JieBelum ada peringkat

- Romania Long Term OutlookDokumen5 halamanRomania Long Term OutlooksmaneranBelum ada peringkat

- A I: M: L I: Ttachment Oldova Etter of NtentDokumen14 halamanA I: M: L I: Ttachment Oldova Etter of Ntentoctavs99Belum ada peringkat

- EN EN: European CommissionDokumen24 halamanEN EN: European Commissionapi-58353949Belum ada peringkat

- UK Research: How Long Can The UK Maintain Its AAA Rating?Dokumen15 halamanUK Research: How Long Can The UK Maintain Its AAA Rating?Daniel Archer-CoxBelum ada peringkat

- Nordea Bank, Global Update, Dec 18, 2013. "Happy New Year 2014"Dokumen7 halamanNordea Bank, Global Update, Dec 18, 2013. "Happy New Year 2014"Glenn ViklundBelum ada peringkat

- Studii Economice - CofaceDokumen2 halamanStudii Economice - CofaceVelicanu Bekk ZsuzsaBelum ada peringkat

- CIS Sovereign Debt Report 2014: Borrowing To Decrease To $51 BillionDokumen9 halamanCIS Sovereign Debt Report 2014: Borrowing To Decrease To $51 Billionapi-228714775Belum ada peringkat

- Macro Update: Slowdown, But Continued Good Resilience in BalticsDokumen2 halamanMacro Update: Slowdown, But Continued Good Resilience in BalticsSEB GroupBelum ada peringkat

- Flash Comment: Latvia - December 7, 2012Dokumen1 halamanFlash Comment: Latvia - December 7, 2012Swedbank AB (publ)Belum ada peringkat

- Country Intelligence: Report: TurkeyDokumen27 halamanCountry Intelligence: Report: TurkeyFlorian SarkisBelum ada peringkat

- Baltic Sea Report 2015Dokumen31 halamanBaltic Sea Report 2015Swedbank AB (publ)Belum ada peringkat

- Public Sector Budgeting Short Essay QuestionDokumen7 halamanPublic Sector Budgeting Short Essay QuestionBrilliant MycriBelum ada peringkat

- Flash Comment: Latvia - November 8, 2012Dokumen1 halamanFlash Comment: Latvia - November 8, 2012Swedbank AB (publ)Belum ada peringkat

- Country Reports - UkraineDokumen44 halamanCountry Reports - UkraineMarcusShusterBelum ada peringkat

- June 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Dokumen70 halamanJune 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Ilya MozyrskiyBelum ada peringkat

- Mozambique Long-Term Rating Lowered To 'B' On High Debt Accumulation 'B' Short-Term Rating Affirmed Outlook StableDokumen7 halamanMozambique Long-Term Rating Lowered To 'B' On High Debt Accumulation 'B' Short-Term Rating Affirmed Outlook Stableapi-228714775Belum ada peringkat

- Colliers International (2014) Bucharest Market Research and Forcast ReportDokumen28 halamanColliers International (2014) Bucharest Market Research and Forcast ReportSimonaGradinaruBelum ada peringkat

- Long-Term Ratings On Italy Lowered To 'BBB' Outlook NegativeDokumen7 halamanLong-Term Ratings On Italy Lowered To 'BBB' Outlook Negativeapi-227433089Belum ada peringkat

- Eurozone: Outlook For Financial ServicesDokumen20 halamanEurozone: Outlook For Financial ServicesEuglena VerdeBelum ada peringkat

- Russia Foreign Currency Ratings Lowered To 'BBB-/A-3' On Risk of Marked Deterioration in External Financing Outlook NegDokumen9 halamanRussia Foreign Currency Ratings Lowered To 'BBB-/A-3' On Risk of Marked Deterioration in External Financing Outlook Negapi-228714775Belum ada peringkat

- 2013 March Ernst & Yang Report German EconomyDokumen8 halaman2013 March Ernst & Yang Report German Economygpanagi1Belum ada peringkat

- Autumn Statement 2013Dokumen123 halamanAutumn Statement 2013Michael HicksBelum ada peringkat

- Autumn Statement 2013Dokumen130 halamanAutumn Statement 2013LukeNicholls07Belum ada peringkat

- Ratings Articles en Us ArticleDokumen4 halamanRatings Articles en Us ArticlemarcelluxBelum ada peringkat

- EU Budget in My Country SlovakiaDokumen12 halamanEU Budget in My Country Slovakiatjnevado1Belum ada peringkat

- Ukraine Downgraded To 'B-' On Government's Lack of Strategy To Secure Foreign Currency Funding Outlook Remains NegativeDokumen7 halamanUkraine Downgraded To 'B-' On Government's Lack of Strategy To Secure Foreign Currency Funding Outlook Remains Negativeapi-228714775Belum ada peringkat

- Burundi: Second Review Under The Extended Credit Facility-Debt Sustainability AnalysisDokumen16 halamanBurundi: Second Review Under The Extended Credit Facility-Debt Sustainability AnalysisBharat SethBelum ada peringkat

- Vanuatu Article IV Consultation 2013Dokumen52 halamanVanuatu Article IV Consultation 2013Kyren GreiggBelum ada peringkat

- Autumn Statement 2012Dokumen4 halamanAutumn Statement 2012Martin ForsytheBelum ada peringkat

- EC Greece Forecast Autumn 13 PDFDokumen2 halamanEC Greece Forecast Autumn 13 PDFThePressProjectIntlBelum ada peringkat

- Romania'S Challenges For Joining The Eu: A Dream Too Far Away?Dokumen4 halamanRomania'S Challenges For Joining The Eu: A Dream Too Far Away?Larisa PîrvuBelum ada peringkat

- CW The Year Ahead 2015-2016Dokumen32 halamanCW The Year Ahead 2015-2016vdmaraBelum ada peringkat

- Govt Debt and DeficitDokumen4 halamanGovt Debt and DeficitSiddharth TiwariBelum ada peringkat

- Poland On Its Way To GreeceDokumen7 halamanPoland On Its Way To GreeceH5F CommunicationsBelum ada peringkat

- Economic Report 2007Dokumen55 halamanEconomic Report 2007Alexandra-Maria VargaBelum ada peringkat

- Alternative Lending Market Report 2016Dokumen18 halamanAlternative Lending Market Report 2016CrowdfundInsider100% (2)

- Nigeria Ratings Affirmed Outlook Negative On Increasing Political, Institutional, and Fiscal RisksDokumen8 halamanNigeria Ratings Affirmed Outlook Negative On Increasing Political, Institutional, and Fiscal Risksapi-228714775Belum ada peringkat

- Portugal: Letter of Intent, Memorandum of Economic and Financial Policies, and Technical Memorandum of UnderstandingDokumen25 halamanPortugal: Letter of Intent, Memorandum of Economic and Financial Policies, and Technical Memorandum of UnderstandingDuarte levyBelum ada peringkat

- UntitledDokumen19 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen3 halamanUntitledapi-231665846Belum ada peringkat

- Ratings On Senegal Affirmed at 'B+/B' Outlook Stable: Research UpdateDokumen7 halamanRatings On Senegal Affirmed at 'B+/B' Outlook Stable: Research Updateapi-231665846Belum ada peringkat

- Euro Money Market Funds Are Likely To Remain Resilient, Despite The ECB's Subzero Deposit RateDokumen7 halamanEuro Money Market Funds Are Likely To Remain Resilient, Despite The ECB's Subzero Deposit Rateapi-231665846Belum ada peringkat

- UntitledDokumen14 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen22 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen9 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen7 halamanUntitledapi-231665846Belum ada peringkat

- Kingdom of Bahrain Ratings Affirmed at 'BBB/A-2' On Stable Growth Prospects Outlook StableDokumen7 halamanKingdom of Bahrain Ratings Affirmed at 'BBB/A-2' On Stable Growth Prospects Outlook Stableapi-231665846Belum ada peringkat

- Ratings On Spain Raised To 'BBB/A-2' On Improved Economic Prospects Outlook StableDokumen8 halamanRatings On Spain Raised To 'BBB/A-2' On Improved Economic Prospects Outlook Stableapi-231665846Belum ada peringkat

- Outlook On The United Kingdom Revised To Stable On Broadening Economic Recovery Ratings Affirmed at 'AAA/A-1+'Dokumen9 halamanOutlook On The United Kingdom Revised To Stable On Broadening Economic Recovery Ratings Affirmed at 'AAA/A-1+'api-231665846Belum ada peringkat

- UntitledDokumen8 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen7 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen11 halamanUntitledapi-231665846Belum ada peringkat

- Which Emerging Market Banking Systems Could Suffer Most From Fed Tapering?Dokumen15 halamanWhich Emerging Market Banking Systems Could Suffer Most From Fed Tapering?api-231665846Belum ada peringkat

- Europe's Housing Market Recovery Is Not Yet On Solid Ground: Economic ResearchDokumen30 halamanEurope's Housing Market Recovery Is Not Yet On Solid Ground: Economic Researchapi-231665846Belum ada peringkat

- UntitledDokumen17 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen17 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen15 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen8 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen11 halamanUntitledapi-231665846Belum ada peringkat

- Key Considerations For Rating Banks in An Independent ScotlandDokumen9 halamanKey Considerations For Rating Banks in An Independent Scotlandapi-231665846Belum ada peringkat

- UntitledDokumen15 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen5 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen16 halamanUntitledapi-231665846Belum ada peringkat

- Inside Credit: Private-Equity Owners Lead The European IPO Resurgence As Company Valuations ImproveDokumen11 halamanInside Credit: Private-Equity Owners Lead The European IPO Resurgence As Company Valuations Improveapi-231665846Belum ada peringkat

- UntitledDokumen10 halamanUntitledapi-231665846Belum ada peringkat

- UntitledDokumen15 halamanUntitledapi-231665846Belum ada peringkat

- A KariozenDokumen4 halamanA Kariozenjoseyamil77Belum ada peringkat

- SAP InvoiceDokumen86 halamanSAP InvoicefatherBelum ada peringkat

- Menu EngineeringDokumen9 halamanMenu Engineeringfirstman31Belum ada peringkat

- NokiaDokumen88 halamanNokiaAkshay Gunecha50% (4)

- Aplicatie Practica Catapulta TUVDokumen26 halamanAplicatie Practica Catapulta TUVwalaBelum ada peringkat

- Companies in UAEDokumen1 halamanCompanies in UAEChelle Sujetado De Guzman50% (2)

- ACCT1501 MC Bank QuestionsDokumen33 halamanACCT1501 MC Bank QuestionsHad0% (2)

- Online Shopping PDFDokumen4 halamanOnline Shopping PDFkeerthanasubramaniBelum ada peringkat

- Project Analysis Report Optus StadiumDokumen14 halamanProject Analysis Report Optus StadiumRida ZainebBelum ada peringkat

- T&S Commercial Invoice Dlrvary Channal Packing ListDokumen3 halamanT&S Commercial Invoice Dlrvary Channal Packing ListkksgmailBelum ada peringkat

- Sample CH 01Dokumen29 halamanSample CH 01Ali Akbar0% (1)

- Ble Assignment 2019 21 BatchDokumen2 halamanBle Assignment 2019 21 BatchRidwan MohsinBelum ada peringkat

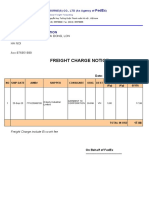

- Freight Charge Notice: To: Garment 10 CorporationDokumen4 halamanFreight Charge Notice: To: Garment 10 CorporationThuy HoangBelum ada peringkat

- Coca Cola Porter S Five Forces Analysis and Diverse Value Chain Activities in Different Areas PDFDokumen33 halamanCoca Cola Porter S Five Forces Analysis and Diverse Value Chain Activities in Different Areas PDFLouise AncianoBelum ada peringkat

- Cash ReceiptDokumen1 halamanCash ReceiptShellinaBelum ada peringkat

- One Point LessonsDokumen27 halamanOne Point LessonsgcldesignBelum ada peringkat

- Ecoborder Brown L Shaped Landscape Edging (6-Pack) - The Home Depot CanadaDokumen4 halamanEcoborder Brown L Shaped Landscape Edging (6-Pack) - The Home Depot Canadaming_zhu10Belum ada peringkat

- Obayomi & Sons Farms: Business PlanDokumen5 halamanObayomi & Sons Farms: Business PlankissiBelum ada peringkat

- The Implications of Globalisation For Consumer AttitudesDokumen2 halamanThe Implications of Globalisation For Consumer AttitudesIvan Luis100% (1)

- Leadership and Strategic Management - GonoDokumen47 halamanLeadership and Strategic Management - GonoDat Nguyen Huy100% (1)

- "Now 6000 Real-Time Screen Shots With Ten Country Payrolls With Real-Time SAP Blueprint" For Demo Click HereDokumen98 halaman"Now 6000 Real-Time Screen Shots With Ten Country Payrolls With Real-Time SAP Blueprint" For Demo Click Herevj_aeroBelum ada peringkat

- F23 - OEE DashboardDokumen10 halamanF23 - OEE DashboardAnand RBelum ada peringkat

- G12 ABM Marketing Lesson 1 (Part 1)Dokumen10 halamanG12 ABM Marketing Lesson 1 (Part 1)Leo SuingBelum ada peringkat

- Progress Test 4 KeyDokumen2 halamanProgress Test 4 Keyalesenan100% (1)

- Leadership & Innovation BrochureDokumen10 halamanLeadership & Innovation BrochureFiona LiemBelum ada peringkat

- Problems in Bureaucratic SupplyDokumen4 halamanProblems in Bureaucratic Supplyatt_doz86100% (1)

- Financial Accounting AssignmentDokumen11 halamanFinancial Accounting AssignmentMadhawa RanawakeBelum ada peringkat

- Coin Sort ReportDokumen40 halamanCoin Sort ReportvishnuBelum ada peringkat

- Revionics - White.paper. (Software As A Service A Retailers)Dokumen7 halamanRevionics - White.paper. (Software As A Service A Retailers)Souvik_DasBelum ada peringkat