Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Art of Selling by Chris MayerDokumen2 halamanArt of Selling by Chris MayerjesprileBelum ada peringkat

- Merger and AcquisitionsDokumen126 halamanMerger and AcquisitionsFaye Lyn Alvezo ValdezBelum ada peringkat

- Capital-Structure-and-Long-term-Financing-Decisions Quick NotesDokumen6 halamanCapital-Structure-and-Long-term-Financing-Decisions Quick NotesAlliah Mae ArbastoBelum ada peringkat

- 200 Practice Questions Solari PDFDokumen206 halaman200 Practice Questions Solari PDFMarek WojtynaBelum ada peringkat

- Tradingview ScriptsDokumen3 halamanTradingview ScriptsAlex LeongBelum ada peringkat

- CH 9-The Cost of Capital by IM PandeyDokumen36 halamanCH 9-The Cost of Capital by IM PandeyJyoti Bansal89% (9)

- BCG Report - Grwoth Thru AcquisitionsDokumen28 halamanBCG Report - Grwoth Thru AcquisitionschengadBelum ada peringkat

- Afar 1stpb Exam-5.21Dokumen7 halamanAfar 1stpb Exam-5.21NananananaBelum ada peringkat

- Ex Ch.17Dokumen3 halamanEx Ch.17kenny 322016048Belum ada peringkat

- Venture CapitalDokumen51 halamanVenture Capitaljravish100% (6)

- Riverhead Town Proposed Battery Energy Storage CodeDokumen10 halamanRiverhead Town Proposed Battery Energy Storage CodeRiverheadLOCALBelum ada peringkat

- 5-10-2022 Budget Hearing Presentation UpdatedDokumen12 halaman5-10-2022 Budget Hearing Presentation UpdatedRiverheadLOCALBelum ada peringkat

- 2022 - 03 - 16 - EPCAL Resolution & Letter AgreementDokumen9 halaman2022 - 03 - 16 - EPCAL Resolution & Letter AgreementRiverheadLOCALBelum ada peringkat

- Riverhead Budget Presentation March 22, 2022Dokumen14 halamanRiverhead Budget Presentation March 22, 2022RiverheadLOCALBelum ada peringkat

- N.Y. Downtown Revitalization Initiative Round Five GuidebookDokumen38 halamanN.Y. Downtown Revitalization Initiative Round Five GuidebookRiverheadLOCALBelum ada peringkat

- Draft Scope Riverhead Logistics CenterDokumen20 halamanDraft Scope Riverhead Logistics CenterRiverheadLOCALBelum ada peringkat

- RXR/GGV Qualified & Eligible Documents (Final 09.26.22)Dokumen23 halamanRXR/GGV Qualified & Eligible Documents (Final 09.26.22)RiverheadLOCALBelum ada peringkat

- AKRF Public Outreach Report AttachmentsDokumen126 halamanAKRF Public Outreach Report AttachmentsRiverheadLOCALBelum ada peringkat

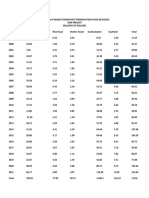

- Peconic Bay Region Community Preservation Fund Revenues 1999-2021Dokumen1 halamanPeconic Bay Region Community Preservation Fund Revenues 1999-2021RiverheadLOCALBelum ada peringkat

- Yvette AguiarDokumen10 halamanYvette AguiarRiverheadLOCALBelum ada peringkat

- Riverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022Dokumen7 halamanRiverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022RiverheadLOCALBelum ada peringkat

- Pediatric Covid-19 Hospitalization ReportDokumen15 halamanPediatric Covid-19 Hospitalization ReportKevin TamponeBelum ada peringkat

- Riverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022Dokumen30 halamanRiverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022RiverheadLOCALBelum ada peringkat

- Kenneth RothwellDokumen5 halamanKenneth RothwellRiverheadLOCALBelum ada peringkat

- Riverhead Town Police Monthly Report July 2021Dokumen6 halamanRiverhead Town Police Monthly Report July 2021RiverheadLOCALBelum ada peringkat

- Catherine KentDokumen7 halamanCatherine KentRiverheadLOCALBelum ada peringkat

- Juan Micieli-MartinezDokumen3 halamanJuan Micieli-MartinezRiverheadLOCALBelum ada peringkat

- Evelyn Hobson-Womack Campaign Finance DisclosureDokumen3 halamanEvelyn Hobson-Womack Campaign Finance DisclosureRiverheadLOCALBelum ada peringkat

- Riverhead Town Police Report, January 2021Dokumen6 halamanRiverhead Town Police Report, January 2021RiverheadLOCALBelum ada peringkat

- Robert E. KernDokumen3 halamanRobert E. KernRiverheadLOCALBelum ada peringkat

- 2021 General Election - Suffolk County Sample Ballot BookletDokumen154 halaman2021 General Election - Suffolk County Sample Ballot BookletRiverheadLOCALBelum ada peringkat

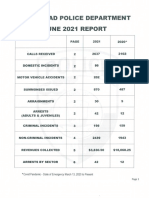

- Riverhead Town Police Monthly Report, June 2021Dokumen6 halamanRiverhead Town Police Monthly Report, June 2021RiverheadLOCALBelum ada peringkat

- League of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsDokumen2 halamanLeague of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsRiverheadLOCAL67% (3)

- Riverhead Town Police Report, March 2021Dokumen6 halamanRiverhead Town Police Report, March 2021RiverheadLOCALBelum ada peringkat

- Old Steeple Church Time CapsuleDokumen4 halamanOld Steeple Church Time CapsuleRiverheadLOCALBelum ada peringkat

- "The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PEDokumen10 halaman"The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PERiverheadLOCALBelum ada peringkat

- Aguiar-Kent Campaign Finance Report 32-Day Pre GeneralDokumen2 halamanAguiar-Kent Campaign Finance Report 32-Day Pre GeneralRiverheadLOCALBelum ada peringkat

- Riverhead Town Police Report, August 2021Dokumen6 halamanRiverhead Town Police Report, August 2021RiverheadLOCALBelum ada peringkat

- NYSED Health and Safety Guide For The 2021 2022 School YearDokumen21 halamanNYSED Health and Safety Guide For The 2021 2022 School YearNewsChannel 9100% (2)

- Navy Environmental Concerns Survey For CalvertonDokumen3 halamanNavy Environmental Concerns Survey For CalvertonRiverheadLOCALBelum ada peringkat

- Oman Cenemnt - March2010Dokumen4 halamanOman Cenemnt - March2010Abhineet JoshiBelum ada peringkat

- Study Material of Capital Markets...Dokumen221 halamanStudy Material of Capital Markets...srikwaits4u91% (22)

- Auditing 2: Review Exercises - OLDokumen7 halamanAuditing 2: Review Exercises - OLVip BigbangBelum ada peringkat

- Diagnostic Quiz On Accounting 2Dokumen9 halamanDiagnostic Quiz On Accounting 2Anne Ford67% (3)

- Birla CableDokumen4 halamanBirla Cablejanam shahBelum ada peringkat

- Financial Reporting and Analysis 6th Edition Revsine Test BankDokumen55 halamanFinancial Reporting and Analysis 6th Edition Revsine Test Bankmrsbrianajonesmdkgzxyiatoq100% (28)

- TCZB 165 1412Dokumen9 halamanTCZB 165 1412ahmet aslanBelum ada peringkat

- Assignment1 SolutionDokumen6 halamanAssignment1 SolutionAnonymous dpWU6H5Lx2Belum ada peringkat

- Unit 1Dokumen48 halamanUnit 1DeshikBelum ada peringkat

- UGBA 183 Berkeley Midterm Spring 2018Dokumen7 halamanUGBA 183 Berkeley Midterm Spring 2018summerhousing2019100% (1)

- HK-Listed Heng Fai Enterprises Sells Singapore Properties For S$53.9 Million (HK$328.8 Million) To SGX Catalist-Listed OELDokumen2 halamanHK-Listed Heng Fai Enterprises Sells Singapore Properties For S$53.9 Million (HK$328.8 Million) To SGX Catalist-Listed OELWeR1 Consultants Pte LtdBelum ada peringkat

- Name: Rooma Ejaz Class: Bs A&F (8A) Date of Submission: 2/jan/2021 ENROLL NO: 02-112171-024 Topic: Mangment Buy-Out Course: Corporate RestructuringDokumen3 halamanName: Rooma Ejaz Class: Bs A&F (8A) Date of Submission: 2/jan/2021 ENROLL NO: 02-112171-024 Topic: Mangment Buy-Out Course: Corporate RestructuringRooma EjazBelum ada peringkat

- Worksheet For FM Chap 2Dokumen3 halamanWorksheet For FM Chap 2Gemechis Lema0% (2)

- Management of Financial ServicesDokumen309 halamanManagement of Financial ServicesSeena AlexanderBelum ada peringkat

- Basket Wonders' Balance Sheet (Asset Side)Dokumen32 halamanBasket Wonders' Balance Sheet (Asset Side)OSAMA0% (1)

- Fmue 2015-16Dokumen4 halamanFmue 2015-16Divya AhujaBelum ada peringkat

- ATS - Daily Trading Plan 27agustus2018Dokumen1 halamanATS - Daily Trading Plan 27agustus2018wahidBelum ada peringkat

- Clarkson Lumber Case QuestionsDokumen2 halamanClarkson Lumber Case QuestionsJeffery KaoBelum ada peringkat

- Maple Leaf Cement: Horizontal Analysis: Balance SheetDokumen9 halamanMaple Leaf Cement: Horizontal Analysis: Balance SheetkilleroffBelum ada peringkat

- Exchange Rate Policy of IndiaDokumen35 halamanExchange Rate Policy of Indiasangeetaangel88% (16)