Anda mungkin juga menyukai

- Green's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Dari EverandGreen's Function Estimates for Lattice Schrödinger Operators and Applications. (AM-158)Belum ada peringkat

- BréhierEtal 2016Dokumen43 halamanBréhierEtal 2016ossama123456Belum ada peringkat

- Press (1972)Dokumen6 halamanPress (1972)cbisogninBelum ada peringkat

- Second-Order Nonlinear Least Squares Estimation: Liqun WangDokumen18 halamanSecond-Order Nonlinear Least Squares Estimation: Liqun WangJyoti GargBelum ada peringkat

- Averaging Oscillations With Small Fractional Damping and Delayed TermsDokumen20 halamanAveraging Oscillations With Small Fractional Damping and Delayed TermsYogesh DanekarBelum ada peringkat

- Stein 2011 DiffFilterDokumen20 halamanStein 2011 DiffFiltersadasdasdffBelum ada peringkat

- R SimDiffProcDokumen25 halamanR SimDiffProcschalteggerBelum ada peringkat

- Stable Marked Point ProcessesDokumen35 halamanStable Marked Point Processesravirajaa07Belum ada peringkat

- CDC18 1363 FiDokumen6 halamanCDC18 1363 FiKoerte FaBelum ada peringkat

- Path-Integral Evolution of Multivariate Systems With Moderate NoiseDokumen15 halamanPath-Integral Evolution of Multivariate Systems With Moderate NoiseLester IngberBelum ada peringkat

- Path Integral Methods For The Dynamics of Stochastic and Disordered SystemsDokumen37 halamanPath Integral Methods For The Dynamics of Stochastic and Disordered SystemsMati dell'ErbaBelum ada peringkat

- Schon WN 2010Dokumen14 halamanSchon WN 2010Shishir KumarBelum ada peringkat

- 1 Nonlinear RegressionDokumen9 halaman1 Nonlinear RegressioneerneeszstoBelum ada peringkat

- C I S 2011 International Press Vol. 11, No. 3, Pp. 197-224, 2011 001Dokumen28 halamanC I S 2011 International Press Vol. 11, No. 3, Pp. 197-224, 2011 001Anh ThanhBelum ada peringkat

- Seismic Source Inversion Using Discontinuous Galerkin Methods A Bayesian ApproachDokumen16 halamanSeismic Source Inversion Using Discontinuous Galerkin Methods A Bayesian ApproachJuan Pablo Madrigal CianciBelum ada peringkat

- 1 s2.0 S0304414918301418 MainDokumen44 halaman1 s2.0 S0304414918301418 MainMahendra PerdanaBelum ada peringkat

- American Statistical AssociationDokumen5 halamanAmerican Statistical AssociationyadaBelum ada peringkat

- Marginalized Adaptive Particle Filtering For Non-Linear Models With Unknown Time-Varying Noise ParametersDokumen13 halamanMarginalized Adaptive Particle Filtering For Non-Linear Models With Unknown Time-Varying Noise ParametersSanil JBelum ada peringkat

- Higham Siam Sde ReviewDokumen22 halamanHigham Siam Sde ReviewAlex ChenBelum ada peringkat

- Estimation For Multivariate Linear Mixed ModelsDokumen6 halamanEstimation For Multivariate Linear Mixed ModelsFir DausBelum ada peringkat

- Elly Aj NK Abc GradDokumen35 halamanElly Aj NK Abc GradGag PafBelum ada peringkat

- Torkamani 2014Dokumen11 halamanTorkamani 2014Jese MadridBelum ada peringkat

- Some Analysis of The Knockoff Filter and Its Variants: Jiajie Chen, Anthony Hou, Thomas Y. Hou June 6, 2017Dokumen25 halamanSome Analysis of The Knockoff Filter and Its Variants: Jiajie Chen, Anthony Hou, Thomas Y. Hou June 6, 2017Anthony HouBelum ada peringkat

- 08 Aos674Dokumen30 halaman08 Aos674siti hayatiBelum ada peringkat

- Discret HamzaouiDokumen19 halamanDiscret HamzaouiPRED ROOMBelum ada peringkat

- Projective Synchronization of Neural Networks With Mixed Time-Varying Delays and Parameter MismatchDokumen10 halamanProjective Synchronization of Neural Networks With Mixed Time-Varying Delays and Parameter MismatchsjstheesarBelum ada peringkat

- Frac Coeff MC RevDokumen25 halamanFrac Coeff MC Revأم الخير تافنيBelum ada peringkat

- Bacry-kozhemyak-muzy-2008-Log Normal Continuous Cascades Aggregation Properties and Estimation-Applications To Financial Time SeriesDokumen27 halamanBacry-kozhemyak-muzy-2008-Log Normal Continuous Cascades Aggregation Properties and Estimation-Applications To Financial Time SeriesReiner_089Belum ada peringkat

- On The Singular Values of The Hankel Matrix With Application in Singular Spectrum AnalysisDokumen15 halamanOn The Singular Values of The Hankel Matrix With Application in Singular Spectrum AnalysisHumbang PurbaBelum ada peringkat

- Segmented Tau Approximation For Test Neutral Functional Differential EquationsDokumen16 halamanSegmented Tau Approximation For Test Neutral Functional Differential Equationsantonio15Belum ada peringkat

- Qu ZhongjunDokumen41 halamanQu ZhongjunjuanivazquezBelum ada peringkat

- Christophe Andrieu - Arnaud Doucet Bristol, BS8 1TW, UK. Cambridge, CB2 1PZ, UK. EmailDokumen4 halamanChristophe Andrieu - Arnaud Doucet Bristol, BS8 1TW, UK. Cambridge, CB2 1PZ, UK. EmailNeil John AppsBelum ada peringkat

- Inverse Synchronization of Coupled Fractional-Order Systems Through Open-Plus-Closed-Loop ControlDokumen12 halamanInverse Synchronization of Coupled Fractional-Order Systems Through Open-Plus-Closed-Loop Controllanoke9980Belum ada peringkat

- Maximum Likelihood Estimation of Stationary Multivariate ARFIMA Processes TSayDokumen17 halamanMaximum Likelihood Estimation of Stationary Multivariate ARFIMA Processes TSayAdis SalkicBelum ada peringkat

- Fractional Parabolic PDEDokumen18 halamanFractional Parabolic PDEyhjfhwBelum ada peringkat

- Computation of The Risk FunctionDokumen29 halamanComputation of The Risk FunctionKim MellBelum ada peringkat

- Estimation For Multivariate Linear Mixed ModelsDokumen7 halamanEstimation For Multivariate Linear Mixed Modelsilkom12Belum ada peringkat

- Gharamani PcaDokumen8 halamanGharamani PcaLeonardo L. ImpettBelum ada peringkat

- Simulation of Square-Root ProcessesDokumen10 halamanSimulation of Square-Root ProcessesShuiyue CheBelum ada peringkat

- On Convergence Rates in The Central Limit Theorems For Combinatorial StructuresDokumen18 halamanOn Convergence Rates in The Central Limit Theorems For Combinatorial StructuresValerio CambareriBelum ada peringkat

- Research StatementDokumen5 halamanResearch StatementEmad AbdurasulBelum ada peringkat

- Pyrespect: A Computer Program To Extract Discrete and Continuous Spectra From Stress Relaxation ExperimentsDokumen24 halamanPyrespect: A Computer Program To Extract Discrete and Continuous Spectra From Stress Relaxation ExperimentsJavad RahmannezhadBelum ada peringkat

- Parameter Estimation of Switching SystemsDokumen11 halamanParameter Estimation of Switching SystemsJosé RagotBelum ada peringkat

- On Bias, Inconsistency, and Efficiency of Various Estimators in Dynamic Panel Data ModelsDokumen26 halamanOn Bias, Inconsistency, and Efficiency of Various Estimators in Dynamic Panel Data ModelsGilani UsmanBelum ada peringkat

- Module 3Dokumen78 halamanModule 3MEGHANA R 20BEC1042Belum ada peringkat

- Applied Mathematical Modelling: M. Hadizadeh, S. YazdaniDokumen9 halamanApplied Mathematical Modelling: M. Hadizadeh, S. YazdaniHo Nhat NamBelum ada peringkat

- Nu Taro ContinuousDokumen23 halamanNu Taro ContinuousRavi KumarBelum ada peringkat

- 09 Ba402Dokumen22 halaman09 Ba402shabaazkurmally.um1Belum ada peringkat

- Method of Moments Using Monte Carlo SimulationDokumen27 halamanMethod of Moments Using Monte Carlo SimulationosmargarnicaBelum ada peringkat

- 1 s2.0 S0377042714002775 MainDokumen13 halaman1 s2.0 S0377042714002775 MainFaria RahimBelum ada peringkat

- Autoregressive Models With Sample Selectivity For Panel DataDokumen45 halamanAutoregressive Models With Sample Selectivity For Panel DatarcsatoBelum ada peringkat

- Tensor Decompositions For Learning Latent Variable Models: Mtelgars@cs - Ucsd.eduDokumen54 halamanTensor Decompositions For Learning Latent Variable Models: Mtelgars@cs - Ucsd.eduJohn KirkBelum ada peringkat

- Cross-Sectional DependenceDokumen5 halamanCross-Sectional DependenceIrfan UllahBelum ada peringkat

- Maquin STA 09Dokumen28 halamanMaquin STA 09p26q8p8xvrBelum ada peringkat

- Monte Carlo Techniques For Bayesian Statistical Inference - A Comparative ReviewDokumen15 halamanMonte Carlo Techniques For Bayesian Statistical Inference - A Comparative Reviewasdfgh132Belum ada peringkat

- Constraining Approaches in Seismic TomographyDokumen16 halamanConstraining Approaches in Seismic Tomographyecce12Belum ada peringkat

- Generalized Real Analysis and Its Applications: Endre PapDokumen19 halamanGeneralized Real Analysis and Its Applications: Endre Papjibabhai9Belum ada peringkat

- Prony Method For ExponentialDokumen21 halamanProny Method For ExponentialsoumyaBelum ada peringkat

- Dispersion TradesDokumen41 halamanDispersion TradesLameune100% (1)

- Commodity Hybrids Trading: James Groves, Barclays CapitalDokumen21 halamanCommodity Hybrids Trading: James Groves, Barclays CapitalLameuneBelum ada peringkat

- Brief Therapy - A Problem Solving Model of ChangeDokumen4 halamanBrief Therapy - A Problem Solving Model of ChangeLameuneBelum ada peringkat

- A Course On Asymptotic Methods, Choice of Model in Regression and CausalityDokumen1 halamanA Course On Asymptotic Methods, Choice of Model in Regression and CausalityLameuneBelum ada peringkat

- Butterfly EconomicsDokumen5 halamanButterfly EconomicsLameuneBelum ada peringkat

- Andrea RoncoroniDokumen27 halamanAndrea RoncoroniLameuneBelum ada peringkat

- Tristam ScottDokumen24 halamanTristam ScottLameuneBelum ada peringkat

- Eyde LandDokumen54 halamanEyde LandLameuneBelum ada peringkat

- Network of Options For International Coal & Freight BusinessesDokumen20 halamanNetwork of Options For International Coal & Freight BusinessesLameuneBelum ada peringkat

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDokumen44 halamanReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneBelum ada peringkat

- Prmia 20111103 NyholmDokumen24 halamanPrmia 20111103 NyholmLameuneBelum ada peringkat

- Reducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalDokumen44 halamanReducing Monte-Carlo Noise in Complex Path-Dependent Trades: Francesco Chiminello Barclays CapitalLameuneBelum ada peringkat

- Pricing Storable Commodities and Associated Derivatives: Dorje C. BrodyDokumen32 halamanPricing Storable Commodities and Associated Derivatives: Dorje C. BrodyLameuneBelum ada peringkat

- Jacob BeharallDokumen19 halamanJacob BeharallLameuneBelum ada peringkat

- Tristam ScottDokumen24 halamanTristam ScottLameuneBelum ada peringkat

- Marcel ProkopczukDokumen28 halamanMarcel ProkopczukLameuneBelum ada peringkat

- Valuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingDokumen25 halamanValuation Challenges For Real World Energy Assets: DR John Putney RWE Supply and TradingLameuneBelum ada peringkat

- Emmanuel GincbergDokumen37 halamanEmmanuel GincbergLameuneBelum ada peringkat

- Day3 Session 1BSternberg PresentationforWebDokumen11 halamanDay3 Session 1BSternberg PresentationforWebLameuneBelum ada peringkat

- Day3 Session2B StoneDokumen11 halamanDay3 Session2B StoneLameuneBelum ada peringkat

- Day3 Session 2APaulDokumen11 halamanDay3 Session 2APaulLameuneBelum ada peringkat

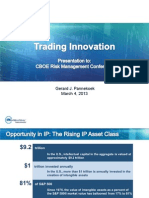

- Gerard J. Pannekoek March 4, 2013Dokumen12 halamanGerard J. Pannekoek March 4, 2013LameuneBelum ada peringkat

- Day1 Session3 ColeDokumen36 halamanDay1 Session3 ColeLameuneBelum ada peringkat

- Machine Learning Cheat SheetDokumen1 halamanMachine Learning Cheat SheetAntony FelixBelum ada peringkat

- EBU Tech Review 2019 Lombardo Cost Analysis of Orchestrated 5G Networks For BroadcastingDokumen33 halamanEBU Tech Review 2019 Lombardo Cost Analysis of Orchestrated 5G Networks For BroadcastingPhilipp A IslaBelum ada peringkat

- Process Validation FDADokumen12 halamanProcess Validation FDAkamran alamBelum ada peringkat

- Regression Analysis (1722021)Dokumen279 halamanRegression Analysis (1722021)Osan ThorpeBelum ada peringkat

- Mastering Scientifi C Computing With RDokumen55 halamanMastering Scientifi C Computing With RPackt PublishingBelum ada peringkat

- Amitha Prasad Senthilvel Vasudevan: BackgroundDokumen5 halamanAmitha Prasad Senthilvel Vasudevan: BackgroundInt J of Med Sci and Nurs ResBelum ada peringkat

- Stats QuizDokumen6 halamanStats QuizMikomi SylvieBelum ada peringkat

- CSU - HM Coconut MuffinDokumen20 halamanCSU - HM Coconut MuffinJohanz PacrisBelum ada peringkat

- Assignment Ch3Dokumen2 halamanAssignment Ch3Andy LeungBelum ada peringkat

- Stat and Prob Q1 M12Dokumen17 halamanStat and Prob Q1 M12Isabel RamosBelum ada peringkat

- WK 11-Session 11 Notes-Hypothesis Testing (Two Samples) - UploadDokumen12 halamanWK 11-Session 11 Notes-Hypothesis Testing (Two Samples) - UploadLIAW ANN YIBelum ada peringkat

- DefinitionDokumen39 halamanDefinitionAloc MavicBelum ada peringkat

- Xpectation Aximization: Grading An Exam Without An Answer KeyDokumen9 halamanXpectation Aximization: Grading An Exam Without An Answer KeyJiahong HeBelum ada peringkat

- Example of Article ReviewDokumen8 halamanExample of Article ReviewNurun Nadia MasromBelum ada peringkat

- Module 5 NotesDokumen17 halamanModule 5 NotesDurga BudhathokiBelum ada peringkat

- The Influence of Customer Perception On Buying Decisions of Apple IphoneDokumen10 halamanThe Influence of Customer Perception On Buying Decisions of Apple IphoneKhushbu kanwarBelum ada peringkat

- Bumastics QP Final1Dokumen16 halamanBumastics QP Final1Ravindra BabuBelum ada peringkat

- Pengaruh Reward, Keselamatan Dan Kesehatan Kerja, Dan Lingkungan Kerja Terhadap Kepuasan KerjaDokumen20 halamanPengaruh Reward, Keselamatan Dan Kesehatan Kerja, Dan Lingkungan Kerja Terhadap Kepuasan Kerjadepi sri rahmawatiBelum ada peringkat

- TSI Alnor EBT720 ManualDokumen64 halamanTSI Alnor EBT720 ManualpalindapcBelum ada peringkat

- UntitledDokumen9 halamanUntitledkihembo pamelahBelum ada peringkat

- Group 8: Grade 7 Mathematics Fourth QuarterDokumen17 halamanGroup 8: Grade 7 Mathematics Fourth QuarterChang CarelBelum ada peringkat

- Chapter 2-Simple Regression ModelDokumen25 halamanChapter 2-Simple Regression ModelMuliana SamsiBelum ada peringkat

- Package KFAS': R Topics DocumentedDokumen21 halamanPackage KFAS': R Topics DocumentedshishirkashyapBelum ada peringkat

- q2 Shs Eapp Module 1 1Dokumen21 halamanq2 Shs Eapp Module 1 1Sandler AndalesBelum ada peringkat

- Risk and Return Practice QuestionsDokumen6 halamanRisk and Return Practice QuestionsPavanBelum ada peringkat

- Understanding Regression Analysis: by Amy GalloDokumen16 halamanUnderstanding Regression Analysis: by Amy GalloDavid Guzman MartinezBelum ada peringkat

- Mohaghegh Validation Aircraft StructuresDokumen18 halamanMohaghegh Validation Aircraft Structuresfalconsaftey43Belum ada peringkat

- Data Analysis - INCOMPLETE - 2Dokumen40 halamanData Analysis - INCOMPLETE - 2vivekBelum ada peringkat

- Service Quality Dimensions and Student Satisfaction During The Covid - 19 PandemicDokumen9 halamanService Quality Dimensions and Student Satisfaction During The Covid - 19 PandemicIOER International Multidisciplinary Research Journal ( IIMRJ)Belum ada peringkat

- Puh 641 Regular Exam 2017Dokumen4 halamanPuh 641 Regular Exam 2017Ayo AlabiBelum ada peringkat

- Love Life: How to Raise Your Standards, Find Your Person, and Live Happily (No Matter What)Dari EverandLove Life: How to Raise Your Standards, Find Your Person, and Live Happily (No Matter What)Penilaian: 3 dari 5 bintang3/5 (1)

- ADHD is Awesome: A Guide to (Mostly) Thriving with ADHDDari EverandADHD is Awesome: A Guide to (Mostly) Thriving with ADHDPenilaian: 5 dari 5 bintang5/5 (4)

- LIT: Life Ignition Tools: Use Nature's Playbook to Energize Your Brain, Spark Ideas, and Ignite ActionDari EverandLIT: Life Ignition Tools: Use Nature's Playbook to Energize Your Brain, Spark Ideas, and Ignite ActionPenilaian: 4 dari 5 bintang4/5 (404)

- The Comfort of Crows: A Backyard YearDari EverandThe Comfort of Crows: A Backyard YearPenilaian: 4.5 dari 5 bintang4.5/5 (23)

- The Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsDari EverandThe Ritual Effect: From Habit to Ritual, Harness the Surprising Power of Everyday ActionsPenilaian: 4 dari 5 bintang4/5 (5)

- Summary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedDari EverandSummary: The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel: Key Takeaways, Summary & Analysis IncludedPenilaian: 4.5 dari 5 bintang4.5/5 (82)

- The Age of Magical Overthinking: Notes on Modern IrrationalityDari EverandThe Age of Magical Overthinking: Notes on Modern IrrationalityPenilaian: 4 dari 5 bintang4/5 (35)

- Cult, A Love Story: Ten Years Inside a Canadian Cult and the Subsequent Long Road of RecoveryDari EverandCult, A Love Story: Ten Years Inside a Canadian Cult and the Subsequent Long Road of RecoveryPenilaian: 4 dari 5 bintang4/5 (46)

- The Obesity Code: Unlocking the Secrets of Weight LossDari EverandThe Obesity Code: Unlocking the Secrets of Weight LossPenilaian: 4 dari 5 bintang4/5 (6)

- By the Time You Read This: The Space between Cheslie's Smile and Mental Illness—Her Story in Her Own WordsDari EverandBy the Time You Read This: The Space between Cheslie's Smile and Mental Illness—Her Story in Her Own WordsBelum ada peringkat

- Think This, Not That: 12 Mindshifts to Breakthrough Limiting Beliefs and Become Who You Were Born to BeDari EverandThink This, Not That: 12 Mindshifts to Breakthrough Limiting Beliefs and Become Who You Were Born to BePenilaian: 2 dari 5 bintang2/5 (1)

- Raising Good Humans: A Mindful Guide to Breaking the Cycle of Reactive Parenting and Raising Kind, Confident KidsDari EverandRaising Good Humans: A Mindful Guide to Breaking the Cycle of Reactive Parenting and Raising Kind, Confident KidsPenilaian: 4.5 dari 5 bintang4.5/5 (170)

- The Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaDari EverandThe Body Keeps the Score by Bessel Van der Kolk, M.D. - Book Summary: Brain, Mind, and Body in the Healing of TraumaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Raising Mentally Strong Kids: How to Combine the Power of Neuroscience with Love and Logic to Grow Confident, Kind, Responsible, and Resilient Children and Young AdultsDari EverandRaising Mentally Strong Kids: How to Combine the Power of Neuroscience with Love and Logic to Grow Confident, Kind, Responsible, and Resilient Children and Young AdultsPenilaian: 5 dari 5 bintang5/5 (1)

- The Twentysomething Treatment: A Revolutionary Remedy for an Uncertain AgeDari EverandThe Twentysomething Treatment: A Revolutionary Remedy for an Uncertain AgePenilaian: 4.5 dari 5 bintang4.5/5 (2)

- Manipulation: The Ultimate Guide To Influence People with Persuasion, Mind Control and NLP With Highly Effective Manipulation TechniquesDari EverandManipulation: The Ultimate Guide To Influence People with Persuasion, Mind Control and NLP With Highly Effective Manipulation TechniquesPenilaian: 4.5 dari 5 bintang4.5/5 (1412)

- Summary: Outlive: The Science and Art of Longevity by Peter Attia MD, With Bill Gifford: Key Takeaways, Summary & AnalysisDari EverandSummary: Outlive: The Science and Art of Longevity by Peter Attia MD, With Bill Gifford: Key Takeaways, Summary & AnalysisPenilaian: 4.5 dari 5 bintang4.5/5 (44)

- Summary: Limitless: Upgrade Your Brain, Learn Anything Faster, and Unlock Your Exceptional Life By Jim Kwik: Key Takeaways, Summary and AnalysisDari EverandSummary: Limitless: Upgrade Your Brain, Learn Anything Faster, and Unlock Your Exceptional Life By Jim Kwik: Key Takeaways, Summary and AnalysisPenilaian: 5 dari 5 bintang5/5 (8)

- Dark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.Dari EverandDark Psychology & Manipulation: Discover How To Analyze People and Master Human Behaviour Using Emotional Influence Techniques, Body Language Secrets, Covert NLP, Speed Reading, and Hypnosis.Penilaian: 4.5 dari 5 bintang4.5/5 (110)

- How to ADHD: The Ultimate Guide and Strategies for Productivity and Well-BeingDari EverandHow to ADHD: The Ultimate Guide and Strategies for Productivity and Well-BeingPenilaian: 1 dari 5 bintang1/5 (2)

- To Explain the World: The Discovery of Modern ScienceDari EverandTo Explain the World: The Discovery of Modern SciencePenilaian: 3.5 dari 5 bintang3.5/5 (51)

- Self-Care for Autistic People: 100+ Ways to Recharge, De-Stress, and Unmask!Dari EverandSelf-Care for Autistic People: 100+ Ways to Recharge, De-Stress, and Unmask!Penilaian: 5 dari 5 bintang5/5 (1)

- The Garden Within: Where the War with Your Emotions Ends and Your Most Powerful Life BeginsDari EverandThe Garden Within: Where the War with Your Emotions Ends and Your Most Powerful Life BeginsBelum ada peringkat

- Critical Thinking: How to Effectively Reason, Understand Irrationality, and Make Better DecisionsDari EverandCritical Thinking: How to Effectively Reason, Understand Irrationality, and Make Better DecisionsPenilaian: 4.5 dari 5 bintang4.5/5 (39)

- The Courage Habit: How to Accept Your Fears, Release the Past, and Live Your Courageous LifeDari EverandThe Courage Habit: How to Accept Your Fears, Release the Past, and Live Your Courageous LifePenilaian: 4.5 dari 5 bintang4.5/5 (254)