Anda mungkin juga menyukai

- Problem Set 1 PDFDokumen3 halamanProblem Set 1 PDFrenjith0% (2)

- Over Heads Additional Sums PDFDokumen40 halamanOver Heads Additional Sums PDFShiva AP100% (1)

- Fly Ash Brick Project - Feasibility Study Using CVP AnalysisDokumen6 halamanFly Ash Brick Project - Feasibility Study Using CVP AnalysisAshish PatwardhanBelum ada peringkat

- Discussion Forum 4.4B SolutionsDokumen5 halamanDiscussion Forum 4.4B SolutionsSidra UmairBelum ada peringkat

- Mathematics and Statistics (Unit IV & V)Dokumen61 halamanMathematics and Statistics (Unit IV & V)denish gandhi75% (4)

- Mathematics and Statistics (Unit IV & V)Dokumen61 halamanMathematics and Statistics (Unit IV & V)denish gandhi75% (4)

- TOPIC 4a - EMPLOYMENT INCOME-derivation and Exemption PDFDokumen19 halamanTOPIC 4a - EMPLOYMENT INCOME-derivation and Exemption PDFSarannyaRajendraBelum ada peringkat

- PH SalaryReport Jan2022Dokumen71 halamanPH SalaryReport Jan2022welson marteBelum ada peringkat

- Tracing The Geographies of Inequality in IndiaDokumen8 halamanTracing The Geographies of Inequality in IndiaAditya RoyBelum ada peringkat

- OverheadsDokumen7 halamanOverheadsshobhit chaturvediBelum ada peringkat

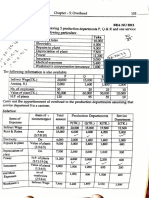

- Q1. Cadila Co. Has Three Production Departments A, B and C and Two ServiceDokumen5 halamanQ1. Cadila Co. Has Three Production Departments A, B and C and Two Servicemedha surBelum ada peringkat

- TYBCOM - Cost - OverheadsDokumen8 halamanTYBCOM - Cost - Overheadsmkbooks4uBelum ada peringkat

- Overheads - CW - Sums - Part 1Dokumen6 halamanOverheads - CW - Sums - Part 1kushgarg627Belum ada peringkat

- Overheads PracticalDokumen37 halamanOverheads PracticalSushant Maskey100% (1)

- Chapter 4 Overhead ProblemsDokumen5 halamanChapter 4 Overhead Problemsthiluvnddi100% (1)

- OverheadsDokumen11 halamanOverheadsCool BuddyBelum ada peringkat

- Seminar Week 2Dokumen2 halamanSeminar Week 2JaquinBelum ada peringkat

- Chapter 6 OverheadsDokumen3 halamanChapter 6 OverheadsDevender SinghBelum ada peringkat

- 4 Soln of OH Q1 To Q 4Dokumen20 halaman4 Soln of OH Q1 To Q 4medha surBelum ada peringkat

- Example Overheards Allocation 1Dokumen4 halamanExample Overheards Allocation 1Phomolo StoffelBelum ada peringkat

- 03 Overhead CostingDokumen9 halaman03 Overhead CostingPappu LalBelum ada peringkat

- Solution To The Problem Set On "Treatment of Overheads"Dokumen6 halamanSolution To The Problem Set On "Treatment of Overheads"Saloni MalhotraBelum ada peringkat

- ACMA Unit 6 Problems - Overheads PDFDokumen4 halamanACMA Unit 6 Problems - Overheads PDFPrabhat SinghBelum ada peringkat

- OverheadApportionment 7Dokumen5 halamanOverheadApportionment 7mitsob27Belum ada peringkat

- Cost Sheet Analysis: Aparna Parmar Damini Baijal Shambhawi SinhaDokumen7 halamanCost Sheet Analysis: Aparna Parmar Damini Baijal Shambhawi SinhaShambhawi SinhaBelum ada peringkat

- Acc 803Dokumen2 halamanAcc 803Tasfia NahiyanBelum ada peringkat

- 04 Overheads DistributionDokumen15 halaman04 Overheads DistributionDevesh BahetyBelum ada peringkat

- Final Accounts-1Dokumen9 halamanFinal Accounts-1Dharma RajBelum ada peringkat

- Tutorial OverheadDokumen6 halamanTutorial OverheadImran FarhanBelum ada peringkat

- Budgetary ControlDokumen14 halamanBudgetary ControlCool BuddyBelum ada peringkat

- Chaithanya Info SystemsDokumen5 halamanChaithanya Info SystemsMichael WellsBelum ada peringkat

- 21st - OCTOBER - 2022-TODAY CLASS - DotDokumen23 halaman21st - OCTOBER - 2022-TODAY CLASS - DotPalesaBelum ada peringkat

- NirmalaDokumen3 halamanNirmalaswamilpatniBelum ada peringkat

- Activity 1 PDFDokumen2 halamanActivity 1 PDFnimeshaBelum ada peringkat

- Overhead ApportionmentDokumen3 halamanOverhead ApportionmentHassanAbsarQaimkhaniBelum ada peringkat

- Tutorial Lesson 3 (Q)Dokumen5 halamanTutorial Lesson 3 (Q)SHERWINA REBECCA GEORGEBelum ada peringkat

- Chapter 5 ExercisesDokumen12 halamanChapter 5 ExercisesIsaiah BatucanBelum ada peringkat

- Problems New TeacherDokumen12 halamanProblems New TeacherAAKASH BAIDBelum ada peringkat

- SYbcom Ac Sem3Dokumen56 halamanSYbcom Ac Sem3Anandkumar Gupta56% (9)

- Bag Financial 1Dokumen3 halamanBag Financial 1mehrunisa ramzanBelum ada peringkat

- Mumbai University - TYBCOM - Sem 5 - Cost AccountingDokumen19 halamanMumbai University - TYBCOM - Sem 5 - Cost Accountingpritika mishraBelum ada peringkat

- Cost Sheet Exercise 1Dokumen3 halamanCost Sheet Exercise 1Phaniraj LenkalapallyBelum ada peringkat

- QB 305E Cost Work AccountingDokumen34 halamanQB 305E Cost Work Accountingshubham singhBelum ada peringkat

- Cost AccountingDokumen53 halamanCost Accountingpritika mishraBelum ada peringkat

- Occupied 500: Area FT.) Light PointsDokumen10 halamanOccupied 500: Area FT.) Light PointsAbhijit HoroBelum ada peringkat

- Manufacturing AccountsDokumen2 halamanManufacturing AccountsMohamed IrshaBelum ada peringkat

- PROBLEM 2-45:: Particulars Case A Case B Case CDokumen6 halamanPROBLEM 2-45:: Particulars Case A Case B Case CSrihari KumarBelum ada peringkat

- Job Costing ADMDokumen18 halamanJob Costing ADMSiddhanta MishraBelum ada peringkat

- Soalan2 Quiz Chapter 3Dokumen8 halamanSoalan2 Quiz Chapter 3biarrahsiaBelum ada peringkat

- DOW Exam Practise DEC 28 2020Dokumen4 halamanDOW Exam Practise DEC 28 2020Hira SialBelum ada peringkat

- Project ACRDokumen30 halamanProject ACRMuneeb KhalidBelum ada peringkat

- Budget of Mini BranchDokumen8 halamanBudget of Mini BranchumenarunaBelum ada peringkat

- 13 OhDokumen12 halaman13 OhLakshay SharmaBelum ada peringkat

- Cost Sheet AnalysisDokumen7 halamanCost Sheet AnalysisShambhawi SinhaBelum ada peringkat

- Overhead Question Bank B.com - (H) Sem IV Paper Bch4.1 Cost Accounting Module 8Dokumen6 halamanOverhead Question Bank B.com - (H) Sem IV Paper Bch4.1 Cost Accounting Module 8Utkarsh VermaBelum ada peringkat

- JobDokumen4 halamanJobNeha SmritiBelum ada peringkat

- Trial BalanceDokumen1 halamanTrial BalanceNurul InsyirahBelum ada peringkat

- Overhead Q 9Dokumen1 halamanOverhead Q 9LOLBelum ada peringkat

- Cost Sheet SumsDokumen2 halamanCost Sheet SumsRoshni MoryeBelum ada peringkat

- Overheard Accounting MathDokumen18 halamanOverheard Accounting Mathfaraaz360Belum ada peringkat

- Cost Sheet Questions - AssignmentDokumen5 halamanCost Sheet Questions - AssignmentDiptee ShettyBelum ada peringkat

- SodapdfDokumen9 halamanSodapdfSARANYABelum ada peringkat

- Budet ExerciseDokumen5 halamanBudet ExerciseVarun yashuBelum ada peringkat

- 03 Overhead CostingDokumen16 halaman03 Overhead CostingBharatbhusan RoutBelum ada peringkat

- British Commercial Computer Digest: Pergamon Computer Data SeriesDari EverandBritish Commercial Computer Digest: Pergamon Computer Data SeriesBelum ada peringkat

- Chapter 13 ...Dokumen24 halamanChapter 13 ...denish gandhiBelum ada peringkat

- Principles of Management (1st Internal) Q 1 Define The FollowingDokumen1 halamanPrinciples of Management (1st Internal) Q 1 Define The Followingdenish gandhiBelum ada peringkat

- Chapter 14Dokumen10 halamanChapter 14denish gandhiBelum ada peringkat

- Fw23-The Decision Making ProcessDokumen19 halamanFw23-The Decision Making Processdenish gandhiBelum ada peringkat

- Chapter - 12: Design of Organisation StructureDokumen16 halamanChapter - 12: Design of Organisation Structuredenish gandhiBelum ada peringkat

- Chapter 10Dokumen6 halamanChapter 10denish gandhiBelum ada peringkat

- Forms of Organisation StructureDokumen24 halamanForms of Organisation Structuredenish gandhiBelum ada peringkat

- Chapter 16Dokumen1 halamanChapter 16denish gandhiBelum ada peringkat

- Chapter 27Dokumen9 halamanChapter 27denish gandhiBelum ada peringkat

- Authority RelationshipDokumen7 halamanAuthority Relationshipdenish gandhiBelum ada peringkat

- Chapter 10Dokumen6 halamanChapter 10denish gandhiBelum ada peringkat

- Chapter 16Dokumen5 halamanChapter 16denish gandhiBelum ada peringkat

- Chapter 13Dokumen24 halamanChapter 13denish gandhiBelum ada peringkat

- Chapter 27Dokumen9 halamanChapter 27denish gandhiBelum ada peringkat

- Chapter 27Dokumen9 halamanChapter 27denish gandhiBelum ada peringkat

- Chapter 14Dokumen10 halamanChapter 14denish gandhiBelum ada peringkat

- Authority RelationshipDokumen7 halamanAuthority Relationshipdenish gandhiBelum ada peringkat

- Authority RelationshipDokumen7 halamanAuthority Relationshipdenish gandhiBelum ada peringkat

- Forms of Organisation StructureDokumen24 halamanForms of Organisation Structuredenish gandhiBelum ada peringkat

- Chapter 13 ...Dokumen24 halamanChapter 13 ...denish gandhiBelum ada peringkat

- Chapter 10Dokumen6 halamanChapter 10denish gandhiBelum ada peringkat

- Chapter 16Dokumen5 halamanChapter 16denish gandhiBelum ada peringkat

- Chapter 14Dokumen9 halamanChapter 14denish gandhi100% (1)

- Chapter :: 7 Chapter 7Dokumen19 halamanChapter :: 7 Chapter 7denish gandhiBelum ada peringkat

- Organization StructureDokumen16 halamanOrganization Structuredenish gandhiBelum ada peringkat

- Chapter 10Dokumen6 halamanChapter 10denish gandhiBelum ada peringkat

- MGT ThoughtsDokumen3 halamanMGT Thoughtsdenish gandhiBelum ada peringkat

- Management Means What Managers Do - Management Is TheDokumen46 halamanManagement Means What Managers Do - Management Is Thedenish gandhi0% (1)

- Academic Year 2022Dokumen41 halamanAcademic Year 2022Skylar RingtonesBelum ada peringkat

- 34 - The Pension System and Retirement Planning in Nigeria PDFDokumen10 halaman34 - The Pension System and Retirement Planning in Nigeria PDFAmmi JulianBelum ada peringkat

- HUD Salary DataDokumen5 halamanHUD Salary DataDennis YuskoBelum ada peringkat

- UNIT 1 Career Business English PathfinderDokumen19 halamanUNIT 1 Career Business English PathfindervaleryBelum ada peringkat

- Assesment 2. Bob Van Diks EarningsDokumen2 halamanAssesment 2. Bob Van Diks EarningsMasixole BokweBelum ada peringkat

- Chapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IDokumen68 halamanChapter 1 - Accounting For Partnership Firms - Fundamentals - Volume IVISHNUKUMAR S VBelum ada peringkat

- The Motivation Toolkit by David KrepsDokumen225 halamanThe Motivation Toolkit by David Krepsposta inutileBelum ada peringkat

- MAX1 CONTRATA 1 NewDokumen6 halamanMAX1 CONTRATA 1 Newregie castilloBelum ada peringkat

- Local Budget Circular No 143Dokumen19 halamanLocal Budget Circular No 143Romnick DoloresBelum ada peringkat

- Current LiabilitiesDokumen94 halamanCurrent LiabilitiesDawit TilahunBelum ada peringkat

- Fundamental Principles of Administrationand SupervisionDokumen7 halamanFundamental Principles of Administrationand SupervisionKathyrine BalacaocBelum ada peringkat

- Case Title: Esalyn Chavez Vs Hon. Edna Bonto-Perez Et. Al (GR 109808)Dokumen4 halamanCase Title: Esalyn Chavez Vs Hon. Edna Bonto-Perez Et. Al (GR 109808)ladyvickyBelum ada peringkat

- Bounce FitnessDokumen4 halamanBounce FitnessCarolina DuqueBelum ada peringkat

- Philippine: Six Sigma Salary SurveyDokumen67 halamanPhilippine: Six Sigma Salary Surveydarwin tacubanzaBelum ada peringkat

- Reward and Recognition at TescoDokumen5 halamanReward and Recognition at TescosameertawfiqBelum ada peringkat

- 2021/2022 Benchmark Select Compensation Reports HR and Benefits Design Policies and PracticesDokumen4 halaman2021/2022 Benchmark Select Compensation Reports HR and Benefits Design Policies and PracticesGloriya DominicBelum ada peringkat

- Employment ContractDokumen6 halamanEmployment ContractIan CeladaBelum ada peringkat

- IELTS SPEAKING - WorkDokumen3 halamanIELTS SPEAKING - WorkQuỳnh Anh Nguyễn HồBelum ada peringkat

- FilipinolohiyaDokumen77 halamanFilipinolohiyaKaren Mae T RemolloBelum ada peringkat

- Prepare Budgets: Submission DetailsDokumen22 halamanPrepare Budgets: Submission DetailsTanushree JawariyaBelum ada peringkat

- Oro Enterprises v. NLRCDokumen13 halamanOro Enterprises v. NLRCKhian JamerBelum ada peringkat

- Employees Satisfaction Regarding Payroll System Dhampur Sugar Mills Ltd. PayrollDokumen91 halamanEmployees Satisfaction Regarding Payroll System Dhampur Sugar Mills Ltd. PayrollUmang Dixit100% (2)

- Module 8 Sss Acd Pacturan CjaDokumen7 halamanModule 8 Sss Acd Pacturan CjaCzarina JaneBelum ada peringkat

- Computation of Income Tax LiabilityDokumen6 halamanComputation of Income Tax LiabilityAbdullah QureshiBelum ada peringkat

- Taxtion Law Unit IIDokumen44 halamanTaxtion Law Unit IIMathew KanichayBelum ada peringkat

- 68346764-Anjali Offer LetterDokumen12 halaman68346764-Anjali Offer Letterthink moveBelum ada peringkat

- Average Golf Course Worker SalaryDokumen6 halamanAverage Golf Course Worker Salaryafiwierot100% (2)