Anda mungkin juga menyukai

- Paper1 1questions2004Dokumen14 halamanPaper1 1questions2004ThịnhĐẹpThầnThánhBelum ada peringkat

- Preparing Financial StatementsDokumen15 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen14 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen14 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen15 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen14 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- 7j-Intix Paper 1.1intDokumen8 halaman7j-Intix Paper 1.1intAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen14 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen15 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen6 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Preparing Financial StatementsDokumen18 halamanPreparing Financial StatementsAUDITOR97Belum ada peringkat

- Part 1 Examination Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen7 halamanPart 1 Examination Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen9 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- Que 01 12Dokumen13 halamanQue 01 12Cosovliu RamonaBelum ada peringkat

- Ans 03 06Dokumen8 halamanAns 03 06samnan123Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen7 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- Bilal AccaDokumen10 halamanBilal Accaanon-147801Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial StatementsDokumen9 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial StatementsAUDITOR97Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial StatementsDokumen7 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial StatementsAUDITOR97Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen9 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen7 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- Preparing Financial Statements: (International Stream)Dokumen13 halamanPreparing Financial Statements: (International Stream)Jerahmeel JalalBelum ada peringkat

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDokumen8 halamanPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97Belum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (120)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Three Largest Stock Market Indexes in The US-A4Dokumen3 halamanThree Largest Stock Market Indexes in The US-A4鄭茗秋Belum ada peringkat

- Accounts Assignment Class 11 CandE 20220111131012374Dokumen5 halamanAccounts Assignment Class 11 CandE 20220111131012374Jithu EmmanuelBelum ada peringkat

- CIBC - 9th Annual Easter Insitutional Investor ConferenceDokumen120 halamanCIBC - 9th Annual Easter Insitutional Investor Conferencegr33ngi4ntBelum ada peringkat

- Multiple Choice Answers and Solutions: Aquino Locsin David HizonDokumen26 halamanMultiple Choice Answers and Solutions: Aquino Locsin David HizonclaudettegasendoBelum ada peringkat

- Financial Ratio AnalysisDokumen6 halamanFinancial Ratio AnalysisKandaroliBelum ada peringkat

- Project On Dividend PolicyDokumen50 halamanProject On Dividend PolicyMukesh Manwani100% (3)

- Foundations of Financial Management Homework Solutions For Chapter 3Dokumen7 halamanFoundations of Financial Management Homework Solutions For Chapter 3GrnEyz7967% (3)

- Financial Statement Analysis: AnDokumen36 halamanFinancial Statement Analysis: AnjanuarBelum ada peringkat

- American Life Insurance CompanyDokumen13 halamanAmerican Life Insurance CompanyPatrick NokrekBelum ada peringkat

- Home Office Books Mandaue Books Date Account Title Debit Credit DateDokumen27 halamanHome Office Books Mandaue Books Date Account Title Debit Credit DateVon Andrei MedinaBelum ada peringkat

- Common Size Income StatementDokumen7 halamanCommon Size Income StatementUSD 654Belum ada peringkat

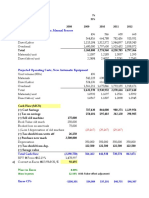

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Dokumen4 halamanProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyBelum ada peringkat

- The Shareholders' Equity Section of Dawson Corporation's Statement of Financial Position As of December 31, 2019, Is As FollowsDokumen4 halamanThe Shareholders' Equity Section of Dawson Corporation's Statement of Financial Position As of December 31, 2019, Is As FollowsAnn louBelum ada peringkat

- CH 05Dokumen92 halamanCH 05Indah LestariBelum ada peringkat

- Problems and Solutions Chapter 1 Advanced Accounting PDFDokumen6 halamanProblems and Solutions Chapter 1 Advanced Accounting PDFMeera Khalil44% (9)

- Latihan Soal Pertemuan Ke-6Dokumen15 halamanLatihan Soal Pertemuan Ke-6gloria rachelBelum ada peringkat

- Accounting For Special Transactions First Grading ExaminationDokumen22 halamanAccounting For Special Transactions First Grading Examinationaccounts 3 life94% (18)

- Test Bank For Fundamentals of Corporate Finance 7th Canadian Edition RossDokumen24 halamanTest Bank For Fundamentals of Corporate Finance 7th Canadian Edition RossJacobJohnsonfipx100% (44)

- BBA VI TH Sem Financial Institution & MarketsDokumen2 halamanBBA VI TH Sem Financial Institution & MarketsJordan ThapaBelum ada peringkat

- RTP June 2017 AnsDokumen23 halamanRTP June 2017 AnsbinuBelum ada peringkat

- Accounting Assignment Document Final DraftDokumen14 halamanAccounting Assignment Document Final DraftSarang BatraBelum ada peringkat

- Blu Containers Worksheet - IntermediateDokumen13 halamanBlu Containers Worksheet - Intermediateahmedmostafaibrahim22Belum ada peringkat

- Tutorial SolutionsDokumen31 halamanTutorial SolutionsBukhari HarBelum ada peringkat

- Name of Business Projected Income Statement For The Years Ended December 31,2017-2021Dokumen10 halamanName of Business Projected Income Statement For The Years Ended December 31,2017-2021Aries Gonzales CaraganBelum ada peringkat

- Coursera Online Course Corporate Finance Essentials Quiz All AnswersDokumen4 halamanCoursera Online Course Corporate Finance Essentials Quiz All AnswersMD GOLAM SARWER100% (5)

- Finanicial AccountingDokumen147 halamanFinanicial AccountingShailesh RathiBelum ada peringkat

- Chapter 10 Part A and Part B ReviewDokumen9 halamanChapter 10 Part A and Part B ReviewNhi HoBelum ada peringkat

- Assignment 3 - SolutionsDokumen4 halamanAssignment 3 - SolutionsEsther LiuBelum ada peringkat

- Latihan 3 PA1Dokumen3 halamanLatihan 3 PA1Diko Rifki DelpieroBelum ada peringkat

- Business FinanceDokumen2 halamanBusiness FinanceApril GarciaBelum ada peringkat