Anda mungkin juga menyukai

- The Obligation of Attending Jamaah in The Masjid in The Absence of A Valid ExcuseDokumen25 halamanThe Obligation of Attending Jamaah in The Masjid in The Absence of A Valid ExcuseAyeshaJangdaBelum ada peringkat

- Pakistan Strategy - CPEC A Big Impetus For Growth and InvestmentDokumen9 halamanPakistan Strategy - CPEC A Big Impetus For Growth and InvestmentAyeshaJangdaBelum ada peringkat

- IslamicExpo 21 Apr 16Dokumen4 halamanIslamicExpo 21 Apr 16AyeshaJangdaBelum ada peringkat

- The Rise of The Digital BankDokumen4 halamanThe Rise of The Digital BankAyeshaJangdaBelum ada peringkat

- McKinsey-Human Factor in Service DesignDokumen6 halamanMcKinsey-Human Factor in Service DesignXalu XalManBelum ada peringkat

- In Need of A Retail Turnaround - How To Know and What To DoDokumen8 halamanIn Need of A Retail Turnaround - How To Know and What To DoAAJANGDABelum ada peringkat

- Digitizing The Consumer Decision JourneyDokumen8 halamanDigitizing The Consumer Decision JourneyMuhammad SohaibBelum ada peringkat

- Taking The Bias Out of MeetingsDokumen2 halamanTaking The Bias Out of MeetingsAyeshaJangdaBelum ada peringkat

- MCK On Defense FINALDokumen92 halamanMCK On Defense FINALAyeshaJangdaBelum ada peringkat

- Islamic Banking Strategy Paper-FinalDokumen25 halamanIslamic Banking Strategy Paper-FinalAyeshaJangdaBelum ada peringkat

- MGI Urban World Rise of The Consuming Class Full Report PDFDokumen92 halamanMGI Urban World Rise of The Consuming Class Full Report PDFbbaa12312342Belum ada peringkat

- Think Regionally Act Locally Four Steps To Reaching The Asian ConsumerDokumen10 halamanThink Regionally Act Locally Four Steps To Reaching The Asian ConsumerAyeshaJangdaBelum ada peringkat

- Beating The Odds in Market EntryDokumen12 halamanBeating The Odds in Market EntryAyeshaJangdaBelum ada peringkat

- IBB Mar 2014Dokumen28 halamanIBB Mar 2014AyeshaJangdaBelum ada peringkat

- Distortions and Deceptions in Strategic DecisionsDokumen12 halamanDistortions and Deceptions in Strategic DecisionsAyeshaJangdaBelum ada peringkat

- Teaching For The New Millennium: Salman KhanDokumen4 halamanTeaching For The New Millennium: Salman KhanAyeshaJangdaBelum ada peringkat

- جدول المواريث بالانجليزيةDokumen1 halamanجدول المواريث بالانجليزيةAyeshaJangda100% (2)

- A Lighter Touch For Postmerger IntegrationDokumen6 halamanA Lighter Touch For Postmerger IntegrationAyeshaJangdaBelum ada peringkat

- MCK On Defense FINALDokumen92 halamanMCK On Defense FINALAyeshaJangdaBelum ada peringkat

- Pakistans PostReforms Banking SectorDokumen5 halamanPakistans PostReforms Banking SectorAyeshaJangdaBelum ada peringkat

- Teaching For The New Millennium: Salman KhanDokumen4 halamanTeaching For The New Millennium: Salman KhanAyeshaJangdaBelum ada peringkat

- World Retail Banking Report 2012 PDFDokumen44 halamanWorld Retail Banking Report 2012 PDFMarcos LeiteBelum ada peringkat

- How We Do It Three Executives Reflect On Strategic Decision MakingDokumen12 halamanHow We Do It Three Executives Reflect On Strategic Decision MakingAyeshaJangdaBelum ada peringkat

- Why Marketers Should Keep Sending You EmailsDokumen3 halamanWhy Marketers Should Keep Sending You EmailsAyeshaJangdaBelum ada peringkat

- CS Banks - 28 Nov 2013Dokumen35 halamanCS Banks - 28 Nov 2013AyeshaJangdaBelum ada peringkat

- Is Your Budget Process Stuck On Last Years NumbersDokumen3 halamanIs Your Budget Process Stuck On Last Years NumbersAyeshaJangdaBelum ada peringkat

- The Rediscovery of India PDFDokumen5 halamanThe Rediscovery of India PDFAyeshaJangdaBelum ada peringkat

- The Case For Behavioral StrategyDokumen16 halamanThe Case For Behavioral StrategyAyeshaJangdaBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Ola CabsDokumen5 halamanOla CabsvimalBelum ada peringkat

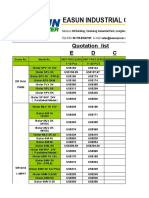

- Quotation List E D C: Series No. Model No. Unit Price (Usd) Unit Price (Usd) Unit Price (Usd)Dokumen4 halamanQuotation List E D C: Series No. Model No. Unit Price (Usd) Unit Price (Usd) Unit Price (Usd)Lucian StroeBelum ada peringkat

- Small Hydro Power Plant: Scenario in India - A Comparative StudyDokumen7 halamanSmall Hydro Power Plant: Scenario in India - A Comparative StudySantosh KumarBelum ada peringkat

- Facts About FASBDokumen8 halamanFacts About FASBvssvaraprasadBelum ada peringkat

- Chapter OneDokumen2 halamanChapter OnebundeBelum ada peringkat

- Admission To Undergraduate Programmes NtuDokumen2 halamanAdmission To Undergraduate Programmes Ntuyen_3580Belum ada peringkat

- Iloilo Bus GuideDokumen2 halamanIloilo Bus GuideMarielle PilapilBelum ada peringkat

- Managerial. EcoDokumen15 halamanManagerial. EcomohitharlaniBelum ada peringkat

- Klyde Warren Park, Dallas, TX: Urban Design Literature Study by Suren Mahant 10008Dokumen24 halamanKlyde Warren Park, Dallas, TX: Urban Design Literature Study by Suren Mahant 10008coolBelum ada peringkat

- Republic Act No. 4726 The Condominium Act: What Is A Condominium?Dokumen4 halamanRepublic Act No. 4726 The Condominium Act: What Is A Condominium?Vic CajuraoBelum ada peringkat

- Smurfit Kappa Sustainable Development Report 2013Dokumen104 halamanSmurfit Kappa Sustainable Development Report 2013edienewsBelum ada peringkat

- Rohit's Investigatory Project - Docx PhysicsDokumen22 halamanRohit's Investigatory Project - Docx PhysicsSaurav Soni100% (1)

- Details of Principal Inputs/ Capital Goods Sr. No. Input Materials/ Capital Goods HSN Exemption Notification Rate of GST CT ST Igst CessDokumen3 halamanDetails of Principal Inputs/ Capital Goods Sr. No. Input Materials/ Capital Goods HSN Exemption Notification Rate of GST CT ST Igst Cessgroup3 cgstauditBelum ada peringkat

- The Truth About EtawahDokumen4 halamanThe Truth About EtawahPoojaDasgupta100% (1)

- Four Steps To Writing A Position Paper You Can Be Proud ofDokumen6 halamanFour Steps To Writing A Position Paper You Can Be Proud ofsilentreaderBelum ada peringkat

- Irma Irsyad - Southwest Case StudyDokumen27 halamanIrma Irsyad - Southwest Case StudyIrma IrsyadBelum ada peringkat

- Transport and LocationDokumen16 halamanTransport and LocationAjay BhasiBelum ada peringkat

- Money Matters VocabularyDokumen16 halamanMoney Matters VocabularySvetlana TselishchevaBelum ada peringkat

- SLS Geotechnical Design PDFDokumen10 halamanSLS Geotechnical Design PDFStelios PetridisBelum ada peringkat

- Canara Bank Deposit RatesDokumen3 halamanCanara Bank Deposit RatesvigyaniBelum ada peringkat

- Royal Dairy: Strategic ManagementDokumen34 halamanRoyal Dairy: Strategic ManagementBassem Safwat BoushraBelum ada peringkat

- Legal Issues in RetailDokumen17 halamanLegal Issues in RetailArunoday Singh100% (5)

- ACP List PDFDokumen35 halamanACP List PDFMohammed ShadabBelum ada peringkat

- Hirofumi UzawaDokumen6 halamanHirofumi UzawaCHINGZU212Belum ada peringkat

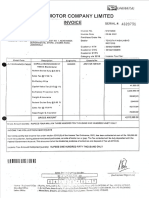

- Toyota InvoiceDokumen1 halamanToyota InvoiceRita SJBelum ada peringkat

- TOFELDokumen18 halamanTOFELNata SchönBelum ada peringkat

- Women in Late Imperial China: A Review of Recent English-Language ScholarshipDokumen38 halamanWomen in Late Imperial China: A Review of Recent English-Language ScholarshipPolina RysakovaBelum ada peringkat

- Nghe HSG 4Dokumen3 halamanNghe HSG 4GiangBelum ada peringkat

- BR100 Accounts Receivable ReferenceDokumen127 halamanBR100 Accounts Receivable ReferenceVenkat Subramanian RBelum ada peringkat

- Integrated Guide PDFDokumen71 halamanIntegrated Guide PDFJha NizBelum ada peringkat