Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Profits&gains From B/PDokumen16 halamanProfits&gains From B/PCA Rama Krishna E VBelum ada peringkat

- Facts of Human BodyDokumen2 halamanFacts of Human BodyCA Rama Krishna E VBelum ada peringkat

- Super Summary AuditinigDokumen43 halamanSuper Summary AuditinigCA Rama Krishna E V100% (3)

- NotificationDokumen3 halamanNotificationSweety JainBelum ada peringkat

- Income Certificate Application FormDokumen2 halamanIncome Certificate Application FormRatish PillaiBelum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Sales Representative QueriesDokumen2 halamanSales Representative Queriesqasim shafiqBelum ada peringkat

- The Sales Handbook by IntercomDokumen89 halamanThe Sales Handbook by IntercomAndrew Richard Thompson67% (3)

- Vendor Opportunity Bill MemoDokumen7 halamanVendor Opportunity Bill MemoStreet Vendor ProjectBelum ada peringkat

- Impact of Online Shopping On Consumer BehaviourDokumen9 halamanImpact of Online Shopping On Consumer BehaviourMichael GregoryBelum ada peringkat

- Bci Bale Tracking SystemDokumen36 halamanBci Bale Tracking Systemdev_31Belum ada peringkat

- Jerry Manko CVDokumen2 halamanJerry Manko CVapi-262492593Belum ada peringkat

- Navneet Education Ltd. Research Report Prateek - SalampuriaDokumen24 halamanNavneet Education Ltd. Research Report Prateek - SalampuriaPrateek Salampuria100% (1)

- Angel PresentationDokumen22 halamanAngel PresentationDharamveer Jairam Sahu100% (1)

- ACCT3610 - Week 4 Case Study - LucentDokumen2 halamanACCT3610 - Week 4 Case Study - LucentMonica TrieuBelum ada peringkat

- Micro EnvironmentDokumen1 halamanMicro EnvironmentBernadeth NoayBelum ada peringkat

- Export - Import Documentation ProceduresDokumen58 halamanExport - Import Documentation ProceduresJebin James75% (4)

- Usenespresso C190 Capsule Espresso Machine Titanium With Case - Ebay PDFDokumen3 halamanUsenespresso C190 Capsule Espresso Machine Titanium With Case - Ebay PDFAnonymous 0QL95CBelum ada peringkat

- Islamic Banking Situational Mcqs PDFDokumen24 halamanIslamic Banking Situational Mcqs PDFNajeeb Magsi100% (1)

- Gasbill 7849961000 202307 20230726135704Dokumen1 halamanGasbill 7849961000 202307 20230726135704AaFi SoomroBelum ada peringkat

- Passion: ProduceDokumen108 halamanPassion: ProduceThanh NguyenBelum ada peringkat

- Homework #2: Due: February 1Dokumen6 halamanHomework #2: Due: February 1cvofoxBelum ada peringkat

- Chapter - 1 Marketing ManagementDokumen25 halamanChapter - 1 Marketing Managementciara WhiteBelum ada peringkat

- Online Stock & Inventory Management System Project in PythonDokumen5 halamanOnline Stock & Inventory Management System Project in PythonRajesh Kumar100% (1)

- Strategic Analysis of TescoDokumen23 halamanStrategic Analysis of TescolokeshBelum ada peringkat

- Property Derivatives PresentationDokumen30 halamanProperty Derivatives Presentationjstamp02100% (1)

- Cta 3D CV 08259 D 2015may27 RefDokumen50 halamanCta 3D CV 08259 D 2015may27 Refanorith88Belum ada peringkat

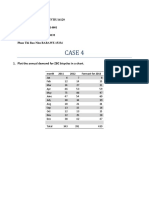

- Case 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334Dokumen4 halamanCase 4: Luyen Ngoc Do Quyen BTFTIU14129 Ngo Khanh Duy BTARIU14601 Pham Gia Huy BTFTIU14132 Phan Thi Bao Nhu BABAWE 15334HuynhGiangBelum ada peringkat

- VAT On Sale of Goods and PropertiesDokumen55 halamanVAT On Sale of Goods and PropertiesNEstanda100% (1)

- Questions On Competition Act 2002Dokumen2 halamanQuestions On Competition Act 2002Harsh Gupta50% (2)

- Business 1 Marketing 1168933Dokumen10 halamanBusiness 1 Marketing 1168933Ravi KumawatBelum ada peringkat

- Measuring The Performance of Investment Centers Using RoiDokumen9 halamanMeasuring The Performance of Investment Centers Using RoiIndah SetyoriniBelum ada peringkat

- Portfolio ManagementDokumen81 halamanPortfolio ManagementPrakash ReddyBelum ada peringkat

- International Trade FinanceDokumen33 halamanInternational Trade Financemesba_17Belum ada peringkat

- Besleri Project ReportDokumen81 halamanBesleri Project ReportTanuj SinghBelum ada peringkat

- Pasta Restaurant Marketing PlanDokumen15 halamanPasta Restaurant Marketing PlanHamad Arif100% (1)