Anda mungkin juga menyukai

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- CDCS Study GuideDokumen68 halamanCDCS Study GuideRoshni Narayanan100% (7)

- Finacle UsermanualDokumen55 halamanFinacle UsermanualNareshaasatBelum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Merril Lynch Case StudyDokumen3 halamanMerril Lynch Case StudyElda VuciBelum ada peringkat

- Declaration PDFDokumen1 halamanDeclaration PDFNareshaasatBelum ada peringkat

- GST in BankingDokumen23 halamanGST in BankingNareshaasatBelum ada peringkat

- Chartered Secretary January 2015Dokumen124 halamanChartered Secretary January 2015NareshaasatBelum ada peringkat

- 1st Counseling Notice & Merit List 2014-15Dokumen20 halaman1st Counseling Notice & Merit List 2014-15NareshaasatBelum ada peringkat

- Non Performing Assets - Challenges To Public Sector Bank-1Dokumen96 halamanNon Performing Assets - Challenges To Public Sector Bank-1nimittpathak1989Belum ada peringkat

- Vikas July BillDokumen1 halamanVikas July Billvikas2354_268878339Belum ada peringkat

- Bank Assurance and Letter of CreditDokumen4 halamanBank Assurance and Letter of CreditRahul Kumar TantwarBelum ada peringkat

- 1mca Education Loan SchemeDokumen3 halaman1mca Education Loan SchemeSurendran NagiahBelum ada peringkat

- 'B' Annexures For Vehicle DealerDokumen14 halaman'B' Annexures For Vehicle DealerParth SarthiBelum ada peringkat

- E Banking FDokumen21 halamanE Banking FM Javaid Arif QureshiBelum ada peringkat

- Canara BankDokumen18 halamanCanara BankparkarmubinBelum ada peringkat

- Contractor's Plant and Machinery Insurance: Presented By: H.O. UnderwritingDokumen17 halamanContractor's Plant and Machinery Insurance: Presented By: H.O. Underwritingasd123gfgdBelum ada peringkat

- Internship Report Format For UIMSDokumen17 halamanInternship Report Format For UIMSasimkhan2014Belum ada peringkat

- Chapter 4-Completing The Accounting Cycle: True/FalseDokumen27 halamanChapter 4-Completing The Accounting Cycle: True/FalseJhopel Casagnap EmanBelum ada peringkat

- The HR Department,: Himalayan Bank Limited Kamaladi, KathmanduDokumen1 halamanThe HR Department,: Himalayan Bank Limited Kamaladi, KathmanduajayBelum ada peringkat

- LCCI Level 3 Certificate in Accounting ASE20104 Jun-2018 PDFDokumen20 halamanLCCI Level 3 Certificate in Accounting ASE20104 Jun-2018 PDFAung Zaw HtweBelum ada peringkat

- Transformation of E-Payment & It's Impact On BanksDokumen36 halamanTransformation of E-Payment & It's Impact On BanksPinky Gupta100% (3)

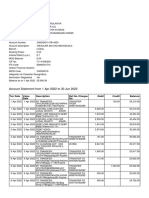

- Account Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen10 halamanAccount Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceParveen SainiBelum ada peringkat

- Methods and Procedures For Risk Profiling ofDokumen18 halamanMethods and Procedures For Risk Profiling ofRohith VijayanBelum ada peringkat

- Asian CurrencyDokumen62 halamanAsian CurrencyDemar DalisayBelum ada peringkat

- Acc Project 2021 22Dokumen14 halamanAcc Project 2021 22Piyush GoyalBelum ada peringkat

- North America Equity ResearchDokumen6 halamanNorth America Equity Researchapi-26007957100% (1)

- Forms of Registration Under Contract Labour Act 1970 PDFDokumen7 halamanForms of Registration Under Contract Labour Act 1970 PDFGlendaBelum ada peringkat

- Xtreme Dance January Newsletter 2012Dokumen1 halamanXtreme Dance January Newsletter 2012incontroltechBelum ada peringkat

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Dokumen3 halamanStatement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Shyam SunderBelum ada peringkat

- Universak BankingDokumen33 halamanUniversak BankingprashantgoruleBelum ada peringkat

- Tax Review QuestionsDokumen11 halamanTax Review QuestionsAbigail Regondola BonitaBelum ada peringkat

- Mike Vassiliou BSC SCV MRICS Ktimatiki Corfac International GreeceDokumen1 halamanMike Vassiliou BSC SCV MRICS Ktimatiki Corfac International GreeceKTIMATIKI CORFAC International Real Estate GreeceBelum ada peringkat

- Risky Ques On BANKINGDokumen64 halamanRisky Ques On BANKINGabhishek3012Belum ada peringkat

- Comparative Study of Sbop & Icici Bank On Car LoanDokumen12 halamanComparative Study of Sbop & Icici Bank On Car LoanSú JálBelum ada peringkat

- Hostel ManualDokumen30 halamanHostel ManualpupegufBelum ada peringkat

- Hsslive-Chapter 12 Not For Profit OrganisationsDokumen7 halamanHsslive-Chapter 12 Not For Profit OrganisationsChandreshBelum ada peringkat