Anda mungkin juga menyukai

- India's Per Capita Food Grain For 2014Dokumen3 halamanIndia's Per Capita Food Grain For 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- #IndiaStockExchange #BSE Update On 24th June 2015Dokumen2 halaman#IndiaStockExchange #BSE Update On 24th June 2015Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Foreign Direct Investment in Equity Market in IndiaDokumen4 halamanForeign Direct Investment in Equity Market in IndiaJhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- MSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Dokumen4 halamanMSMEs or Micro Small and Medium Enterprses Share in India Exports 2013-2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India Coir Trade From April To October 2014Dokumen4 halamanIndia Coir Trade From April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

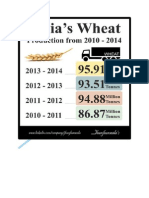

- India's Wheat Production From 2010 To 2014Dokumen4 halamanIndia's Wheat Production From 2010 To 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Commercially Operating Nuclear Reactors in The World at The End of 2013Dokumen4 halamanCommercially Operating Nuclear Reactors in The World at The End of 2013Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Rice Trade For 2014Dokumen5 halamanIndia's Rice Trade For 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Dokumen3 halamanIndia's UREA Trade On 2013-14 and 2014-15 Up To November 2014.Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Diamond Reserves With Diamond Trade Update For 2014Dokumen6 halamanIndia's Diamond Reserves With Diamond Trade Update For 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

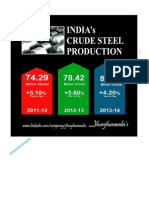

- India Crude Steel Production From 2011-2014Dokumen4 halamanIndia Crude Steel Production From 2011-2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Index of Eight Core Industries From June To November 2014Dokumen57 halamanIndia's Index of Eight Core Industries From June To November 2014Jhunjhunwalas Digital Finance & Business Info Library100% (1)

- Foreign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Dokumen3 halamanForeign Institutional Investors Investment in India During 2014-15 Until 27th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Coal Production For Last 5 Years Upto October 2014Dokumen2 halamanIndia's Coal Production For Last 5 Years Upto October 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Import and Export Update For September and December 2014Dokumen16 halamanIndia's Import and Export Update For September and December 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Coal Reserves To Last 100 YearsDokumen3 halamanIndia's Coal Reserves To Last 100 YearsJhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Methane Hydrates Reserves 25th November 2014Dokumen3 halamanIndia's Methane Hydrates Reserves 25th November 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Foreign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Dokumen27 halamanForeign Investment Promotion Board Approves 12 Proposals of Foreign Direct Investment in India As On 19th December 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Kharif and Rabi Crops Area Coverage For October and January 2014Dokumen10 halamanIndia's Kharif and Rabi Crops Area Coverage For October and January 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

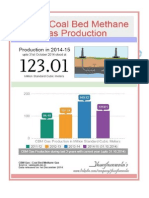

- India's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Dokumen3 halamanIndia's Coal Bed Methane Production For Last 3 Years With Current Year 2014-15 (Upto 31 Oct 2014)Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Global Central Banks Highlights For Monetary Policy Rates For October 2014Dokumen31 halamanGlobal Central Banks Highlights For Monetary Policy Rates For October 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Indians Railways Revenue Earnings With Freight Traffic During April To October 2014Dokumen18 halamanIndians Railways Revenue Earnings With Freight Traffic During April To October 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Fuel Price Change For Petrol, Diesel, and JetFuel in IndiaDokumen11 halamanFuel Price Change For Petrol, Diesel, and JetFuel in IndiaJhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Crude Steel Production Estimate For 2014 To 2017Dokumen3 halamanIndia's Crude Steel Production Estimate For 2014 To 2017Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Mineral Production in Month of August 2014Dokumen3 halamanIndia's Mineral Production in Month of August 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India Tax Collection From April To November 2014Dokumen11 halamanIndia Tax Collection From April To November 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India's Tourism Sector Performance For January and October 2014Dokumen15 halamanIndia's Tourism Sector Performance For January and October 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- Indian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Dokumen5 halamanIndian Currency Rupee Exchange Rate of 19 Foreign Currencies Relating To Import and Export Goods From July To September 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

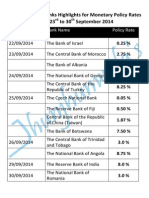

- Global Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Dokumen11 halamanGlobal Central Banks Highlights For Monetary Policy Rates From 23rd To 30th September 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- India 'S Total Kharif Crop Sowing Area As On July and August 2014Dokumen6 halamanIndia 'S Total Kharif Crop Sowing Area As On July and August 2014Jhunjhunwalas Digital Finance & Business Info LibraryBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (120)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Worksheet 2Dokumen3 halamanWorksheet 2kevin nagacBelum ada peringkat

- NCERT Solutions For Class 11 Economics Chapter 2Dokumen8 halamanNCERT Solutions For Class 11 Economics Chapter 2raghu8215Belum ada peringkat

- Mishkin 6ce TB Ch13Dokumen32 halamanMishkin 6ce TB Ch13JaeDukAndrewSeo50% (2)

- I. 1. Read The Text Below and Complete The Following Tasks. Write All Your Answers On The Answer SheetDokumen3 halamanI. 1. Read The Text Below and Complete The Following Tasks. Write All Your Answers On The Answer SheetDiana-Paula MihaiBelum ada peringkat

- Finacc 3Dokumen6 halamanFinacc 3Tong WilsonBelum ada peringkat

- 2011 03 14 Palm Oil Sector ReportDokumen72 halaman2011 03 14 Palm Oil Sector ReportSrujitha Reddy LingaBelum ada peringkat

- Principles of Finance Practice QuestionsDokumen18 halamanPrinciples of Finance Practice QuestionsResa NgBelum ada peringkat

- 21 Financial Instruments s22 - FINALDokumen95 halaman21 Financial Instruments s22 - FINALAphelele GqadaBelum ada peringkat

- Nism Series V C Mutual Fund Distributors Level 2 Workbook in PDFDokumen246 halamanNism Series V C Mutual Fund Distributors Level 2 Workbook in PDFanmolBelum ada peringkat

- PDICDokumen16 halamanPDICBrian Jonathan ParaanBelum ada peringkat

- Research PMDokumen11 halamanResearch PMapi-233810148Belum ada peringkat

- The Tussle Between Adamjee and Mansha GroupDokumen4 halamanThe Tussle Between Adamjee and Mansha Groupahsahito12Belum ada peringkat

- Astrodome FINAL Report 5-23-12Dokumen354 halamanAstrodome FINAL Report 5-23-12Mike MorrisBelum ada peringkat

- Profile On The Production of Shock Absorber (Spring)Dokumen26 halamanProfile On The Production of Shock Absorber (Spring)ak123456Belum ada peringkat

- Feasibility Research On Rice Production For Zamboanga CooperativeDokumen40 halamanFeasibility Research On Rice Production For Zamboanga Cooperativejeffrey ordonezBelum ada peringkat

- Aditya Shukla Home Made Food App IdeaDokumen37 halamanAditya Shukla Home Made Food App IdeaChandan SrivastavaBelum ada peringkat

- Nism 8Dokumen235 halamanNism 8Sohail Shaikh100% (3)

- Shift The Focus From The Super-Poor To The Super-Rich (Otto, 2019)Dokumen3 halamanShift The Focus From The Super-Poor To The Super-Rich (Otto, 2019)CliffhangerBelum ada peringkat

- Chapter 3 - Cash Flow Analysis - SVDokumen26 halamanChapter 3 - Cash Flow Analysis - SVNguyen LienBelum ada peringkat

- INDIAN RAILWAYS - Source of Finance BudgetaryDokumen12 halamanINDIAN RAILWAYS - Source of Finance Budgetaryjeya chandranBelum ada peringkat

- Practice Questions For AMFI TestDokumen41 halamanPractice Questions For AMFI TestanupBelum ada peringkat

- Mahindra & Mahindra VS Tata MotorsDokumen20 halamanMahindra & Mahindra VS Tata MotorsPratik Kalekar100% (1)

- RE1 Trading CaseDokumen3 halamanRE1 Trading CaseDerrick LowBelum ada peringkat

- Tutorial 1 AnswersDokumen3 halamanTutorial 1 AnswersAmeer FulatBelum ada peringkat

- AUC Settlement in Asset Accounting - Your Finance BookDokumen3 halamanAUC Settlement in Asset Accounting - Your Finance BookTamal BiswasBelum ada peringkat

- De Vera V CADokumen5 halamanDe Vera V CAcmv mendozaBelum ada peringkat

- This Study Resource WasDokumen5 halamanThis Study Resource WasDevia SuswodijoyoBelum ada peringkat

- Deloitte - IFRS in Real EstateDokumen13 halamanDeloitte - IFRS in Real EstateRD100% (1)

- The Time To Green FinanceDokumen46 halamanThe Time To Green FinanceComunicarSe-ArchivoBelum ada peringkat

- (PART 2) 8990 - 2021 Definitive Information Statement (Consolidated AFS)Dokumen124 halaman(PART 2) 8990 - 2021 Definitive Information Statement (Consolidated AFS)PaulBelum ada peringkat