Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Helping Shape Your Future: Chartered Financial Analyst (CFA)Dokumen12 halamanHelping Shape Your Future: Chartered Financial Analyst (CFA)wakemeup143Belum ada peringkat

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Taxation of Employee Fringe BenefitsDokumen28 halamanThe Taxation of Employee Fringe Benefitswakemeup143Belum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5794)

- 2014, T302, Topic 3, Taxable Activity & Regn, 1 SlideDokumen18 halaman2014, T302, Topic 3, Taxable Activity & Regn, 1 Slidewakemeup143Belum ada peringkat

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- FBTDokumen4 halamanFBTwakemeup143Belum ada peringkat

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- VAT On Imports and ExportsDokumen18 halamanVAT On Imports and Exportswakemeup1430% (1)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Tiếp Cận Khối Vùng Chậu: Gv Hướng Dẫn: Ths. Bs. Lê Thị Hồng VânDokumen135 halamanTiếp Cận Khối Vùng Chậu: Gv Hướng Dẫn: Ths. Bs. Lê Thị Hồng Vânwakemeup143Belum ada peringkat

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Taxable Supplies - DR MartinDokumen22 halamanTaxable Supplies - DR Martinwakemeup143Belum ada peringkat

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Exam NotesDokumen21 halamanExam Notesrong004100% (1)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Supply VATDokumen25 halamanSupply VATwakemeup143Belum ada peringkat

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Case Study Cam LTDDokumen9 halamanCase Study Cam LTDwakemeup143Belum ada peringkat

- Job and Batch Costing II COMPLETEDokumen34 halamanJob and Batch Costing II COMPLETEwakemeup143Belum ada peringkat

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Tax TalkDokumen29 halamanTax Talkwakemeup143Belum ada peringkat

- VATon Financial Services PDFDokumen5 halamanVATon Financial Services PDFwakemeup143Belum ada peringkat

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Chapter 6 Property Plant and Equipment ModelsDokumen41 halamanChapter 6 Property Plant and Equipment ModelsHammad Ahmad77% (13)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (73)

- Kiwi Life Insurance DebriefDokumen7 halamanKiwi Life Insurance Debriefwakemeup143Belum ada peringkat

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- Business StructuresDokumen1 halamanBusiness Structureswakemeup143Belum ada peringkat

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- IAS 2 - InventoriesDokumen42 halamanIAS 2 - Inventorieswakemeup143100% (1)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- IAS 18 - Revenue RecognitionDokumen26 halamanIAS 18 - Revenue Recognitionwakemeup143Belum ada peringkat

- Principles of A Good Tax SystemDokumen1 halamanPrinciples of A Good Tax Systemwakemeup143Belum ada peringkat

- IAS 12 TaxationDokumen30 halamanIAS 12 Taxationwakemeup143Belum ada peringkat

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Chapter 17 Provisions and Post Balance Sheet EventsDokumen29 halamanChapter 17 Provisions and Post Balance Sheet EventsHammad Ahmad100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Indirect Tax 2013Dokumen120 halamanIndirect Tax 2013wakemeup143Belum ada peringkat

- Hatfield Ethics of Tax LawyeringDokumen63 halamanHatfield Ethics of Tax Lawyeringwakemeup143Belum ada peringkat

- IAS 40 - Investment PropertyDokumen16 halamanIAS 40 - Investment Propertywakemeup143Belum ada peringkat

- WestpacTrust Case WK 7Dokumen26 halamanWestpacTrust Case WK 7wakemeup143Belum ada peringkat

- FCOM111 2013 Trimester One Course OutlineDokumen31 halamanFCOM111 2013 Trimester One Course Outlinewakemeup143Belum ada peringkat

- Financial AccountingDokumen746 halamanFinancial Accountingwakemeup143100% (4)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Government Regulation and The Legal Environment of BusinessDokumen901 halamanGovernment Regulation and The Legal Environment of Businesswakemeup143100% (2)

- Ssac2006.Hf5691.Jm1.1 StudentDokumen18 halamanSsac2006.Hf5691.Jm1.1 Studentwakemeup143Belum ada peringkat

- MortgageDokumen88 halamanMortgagejhanu jhanuBelum ada peringkat

- Chapter Four: Taxation and Corporate Decision MakingDokumen18 halamanChapter Four: Taxation and Corporate Decision Makingembiale ayalu100% (1)

- Colgate Ratio Analysis WSM 2020 SolvedDokumen19 halamanColgate Ratio Analysis WSM 2020 Solvedwan nur anisahBelum ada peringkat

- Sbi Mutual Fund Introduction - Converted - by - AbcdpdfDokumen6 halamanSbi Mutual Fund Introduction - Converted - by - AbcdpdfAnkita RanaBelum ada peringkat

- CH4 InvDokumen16 halamanCH4 InvPhước VũBelum ada peringkat

- 5-10 Fa1Dokumen10 halaman5-10 Fa1Shahab ShafiBelum ada peringkat

- What Is FactoringDokumen22 halamanWhat Is Factoringshah faisal100% (1)

- More Credit With Fewer Crises 2011Dokumen84 halamanMore Credit With Fewer Crises 2011World Economic ForumBelum ada peringkat

- # 52 Zubik Vs BurwellDokumen8 halaman# 52 Zubik Vs Burwellrols villanezaBelum ada peringkat

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

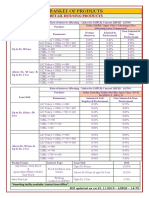

- BASKET OF PRODUCTS As On 21.11.19Dokumen3 halamanBASKET OF PRODUCTS As On 21.11.19Virendra K VermaBelum ada peringkat

- Employment Issues in Insolvency (2013)Dokumen9 halamanEmployment Issues in Insolvency (2013)Iqbal MohammedBelum ada peringkat

- E.bs 3rd-Unit 14 BankingDokumen52 halamanE.bs 3rd-Unit 14 BankingQuỳnh HunnieBelum ada peringkat

- Capital Growth, Financing Source and Profitability of Small Businesses: Evidence From Taiwan Small EnterprisesDokumen2 halamanCapital Growth, Financing Source and Profitability of Small Businesses: Evidence From Taiwan Small EnterprisesKukurubuuuBelum ada peringkat

- Acf 366-Financial Management (All)Dokumen274 halamanAcf 366-Financial Management (All)Paul AmihereBelum ada peringkat

- t1189 Nationwide BTL Product GuideDokumen20 halamant1189 Nationwide BTL Product GuideRavierBelum ada peringkat

- Latham Watkins Second Lien LoansDokumen56 halamanLatham Watkins Second Lien Loanspvalka1Belum ada peringkat

- Gregory Albo: Department of Political Science, York University CanadaDokumen19 halamanGregory Albo: Department of Political Science, York University CanadaMônica Di MasiBelum ada peringkat

- Credit+management Chapter 1 2Dokumen52 halamanCredit+management Chapter 1 2Omar FarukBelum ada peringkat

- Treasury Operations of Islamic Banks 2Dokumen11 halamanTreasury Operations of Islamic Banks 2idrisngrBelum ada peringkat

- PSE Overview PDFDokumen43 halamanPSE Overview PDFRonStephaneMaylonBelum ada peringkat

- Schedule Showing Changes in Working Capital For The Financial Year 2017-18 (Rs. in Million)Dokumen6 halamanSchedule Showing Changes in Working Capital For The Financial Year 2017-18 (Rs. in Million)Shobhit ShuklaBelum ada peringkat

- Ratio Analysis On Dabur India Ltd.Dokumen62 halamanRatio Analysis On Dabur India Ltd.dheeraj dawar50% (2)

- LAW ON BUSINESS TRANSACTIONS (Obligation To Sales)Dokumen31 halamanLAW ON BUSINESS TRANSACTIONS (Obligation To Sales)Joen SinamagBelum ada peringkat

- HO 2 Receivables PDFDokumen4 halamanHO 2 Receivables PDFIzzy BBelum ada peringkat

- Group4 - CF - Dividend PolicyDokumen10 halamanGroup4 - CF - Dividend PolicyAKSHAYKUMAR SHARMABelum ada peringkat

- ChargesDokumen16 halamanChargesSrija ChidaraBelum ada peringkat

- DBP v. Guarina Corp.Dokumen18 halamanDBP v. Guarina Corp.Juris FormaranBelum ada peringkat

- Chapter Elements of FSDokumen15 halamanChapter Elements of FSangellachavezlabalan.cpalawyerBelum ada peringkat

- Management of Financial InstitutionsDokumen165 halamanManagement of Financial Institutionskannnamreddyeswar80% (5)

- Enriquez Vs RanoloDokumen2 halamanEnriquez Vs RanoloLoveAnneBelum ada peringkat

- Ben & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooDari EverandBen & Jerry's Double-Dip Capitalism: Lead With Your Values and Make Money TooPenilaian: 5 dari 5 bintang5/5 (2)

- Introduction to Negotiable Instruments: As per Indian LawsDari EverandIntroduction to Negotiable Instruments: As per Indian LawsPenilaian: 5 dari 5 bintang5/5 (1)

- Wall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementDari EverandWall Street Money Machine: New and Incredible Strategies for Cash Flow and Wealth EnhancementPenilaian: 4.5 dari 5 bintang4.5/5 (20)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDari EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingPenilaian: 4.5 dari 5 bintang4.5/5 (97)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDari EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorPenilaian: 4.5 dari 5 bintang4.5/5 (132)

- Indian Polity with Indian Constitution & Parliamentary AffairsDari EverandIndian Polity with Indian Constitution & Parliamentary AffairsBelum ada peringkat