Anda mungkin juga menyukai

- Negotiable Instruments Act, 1881Dokumen33 halamanNegotiable Instruments Act, 1881Vinayak Khemani100% (1)

- Negotiable InstrumentsDokumen11 halamanNegotiable Instrumentsannmiraflor100% (1)

- Negotiable InstrumentsDokumen23 halamanNegotiable InstrumentssweetchotuBelum ada peringkat

- Chapter 05 Negotiable Instruments Act 1881 1229869805849562 1Dokumen11 halamanChapter 05 Negotiable Instruments Act 1881 1229869805849562 1अरुण शर्माBelum ada peringkat

- Negotiable Instruments Act ExplainedDokumen23 halamanNegotiable Instruments Act ExplainedAishwarya PriyadarshiniBelum ada peringkat

- Introduction to Negotiable Instruments: As per Indian LawsDari EverandIntroduction to Negotiable Instruments: As per Indian LawsPenilaian: 5 dari 5 bintang5/5 (1)

- Negotiable Instruments Act SummaryDokumen59 halamanNegotiable Instruments Act Summaryvivekananda Roy100% (7)

- Negotiable InstrumentsDokumen50 halamanNegotiable InstrumentsMj Panciles100% (3)

- Negotiable Instruments: Legal Aspects of BusinessDokumen25 halamanNegotiable Instruments: Legal Aspects of BusinessArun Sharma100% (2)

- Negotiable instruments law essentialsDokumen4 halamanNegotiable instruments law essentialsxsar_x100% (2)

- Negotiable Instruments - Notice of DishonorDokumen26 halamanNegotiable Instruments - Notice of DishonorRM MallorcaBelum ada peringkat

- Basics of Negotiable InstrumentsDokumen46 halamanBasics of Negotiable Instrumentsgox350% (2)

- The Negotiable Instruments Law Act of 1911Dokumen12 halamanThe Negotiable Instruments Law Act of 1911Marco ArponBelum ada peringkat

- Negotiable InstrumentsDokumen9 halamanNegotiable InstrumentsJANE MARIE DOROMALBelum ada peringkat

- Law of Negotiable Instruments ExplainedDokumen24 halamanLaw of Negotiable Instruments Explainedshiftn7100% (3)

- Negotiable Instruments Act, 1881Dokumen23 halamanNegotiable Instruments Act, 1881Kansal Abhishek100% (1)

- Negotiable InstrumentsDokumen20 halamanNegotiable InstrumentsFRANCIS JOSEPH100% (1)

- Bills of ExchangeDokumen5 halamanBills of Exchangesara24391100% (3)

- IndorsementDokumen1 halamanIndorsementJason HenryBelum ada peringkat

- Extinguishment of Obligations: Payment, Performance and Loss of the Thing DueDokumen39 halamanExtinguishment of Obligations: Payment, Performance and Loss of the Thing DueClaudine Marabut Tabora-RamonesBelum ada peringkat

- Ch 11 Consideration & Promissory EstoppelDokumen18 halamanCh 11 Consideration & Promissory EstoppelHenggao CaiBelum ada peringkat

- Negotiable Instruments ActDokumen34 halamanNegotiable Instruments Actx2Belum ada peringkat

- Bill of Exchange (Credit Instruments)Dokumen12 halamanBill of Exchange (Credit Instruments)Aziz ShaikhBelum ada peringkat

- Stamp Duties Act 15 of 1993Dokumen40 halamanStamp Duties Act 15 of 1993André Le Roux100% (4)

- Nil Holder in Due CourseDokumen13 halamanNil Holder in Due CourseLennart ReyesBelum ada peringkat

- The Power of Attorney Act 1882Dokumen2 halamanThe Power of Attorney Act 1882Naveen Kumar SharmaBelum ada peringkat

- Full Faith & Credit ActDokumen6 halamanFull Faith & Credit ActRoy Tanner100% (2)

- Accounting For Special Transactions: Unit - 1 Bills of Exhange and Promissory NotesDokumen31 halamanAccounting For Special Transactions: Unit - 1 Bills of Exhange and Promissory NotesNakul ChaudharyBelum ada peringkat

- Surety ShipDokumen2 halamanSurety ShipMakoy MolinaBelum ada peringkat

- The Negotiable Instruments LawDokumen16 halamanThe Negotiable Instruments LawMark Earl Santos100% (1)

- The Surety Is Discharged From His Liability On 6 CircumstancesDokumen5 halamanThe Surety Is Discharged From His Liability On 6 CircumstancesPriyankaJainBelum ada peringkat

- Negotiable InstrumentDokumen15 halamanNegotiable InstrumentAngelitOdicta100% (2)

- Commercial Paper DefinitionDokumen6 halamanCommercial Paper DefinitionDebasish DeyBelum ada peringkat

- Ogden - The Law of Negotiable InstrumentsDokumen888 halamanOgden - The Law of Negotiable InstrumentsEdward Jay Robin Belanger100% (5)

- Bills of Exchange & Consumer Credit LawDokumen41 halamanBills of Exchange & Consumer Credit LawDaniel100% (2)

- UNCITRAL Model for International Payments GuideDokumen8 halamanUNCITRAL Model for International Payments GuideroselinBelum ada peringkat

- Doctrine of SubrogationDokumen5 halamanDoctrine of SubrogationPRASANG NANDWANA100% (2)

- Acceptance Endorsement and Surrender Bill of LadingDokumen28 halamanAcceptance Endorsement and Surrender Bill of Ladingv100% (3)

- What Happens If The Presentment Is Done BEFORE The Instrument Is Due?Dokumen3 halamanWhat Happens If The Presentment Is Done BEFORE The Instrument Is Due?bmdadamsonBelum ada peringkat

- 2012 June 15.bills of ExchangeDokumen20 halaman2012 June 15.bills of ExchangeAy Ar Ey Valencia100% (1)

- Negotiable Instruments Act 1881Dokumen16 halamanNegotiable Instruments Act 1881Sunil Shaw100% (2)

- Promissory Note & Bill of ExchangeDokumen1 halamanPromissory Note & Bill of ExchangehemantnalekarBelum ada peringkat

- Bill of Exchange Act 34 of 1964Dokumen31 halamanBill of Exchange Act 34 of 1964lifeisgrand100% (7)

- The UNITED NATIONS Convention On International Bills of Exchange and International Promissory NotesDokumen8 halamanThe UNITED NATIONS Convention On International Bills of Exchange and International Promissory NotesDanton Lawson100% (1)

- Doctrine of SubrogationDokumen3 halamanDoctrine of SubrogationchitraBelum ada peringkat

- INDORSEMENT LIABILITYDokumen71 halamanINDORSEMENT LIABILITYFrancezedric CruzBelum ada peringkat

- Law On Negotiable InstrumentDokumen20 halamanLaw On Negotiable InstrumentLhyn Cantal Calica100% (1)

- Bill of ExchangeDokumen4 halamanBill of ExchangeChetan SapraBelum ada peringkat

- Accounting for Bills of Exchange (40 charactersDokumen10 halamanAccounting for Bills of Exchange (40 charactersMumtazAhmadBelum ada peringkat

- Surety's Right to Subrogation Against Third Party Bank AnalyzedDokumen6 halamanSurety's Right to Subrogation Against Third Party Bank AnalyzedFaith100% (4)

- Law of Suretyship - by StearnsDokumen760 halamanLaw of Suretyship - by Stearnsilovemondays1100% (10)

- Cheeseman Blaw9e Inppt 16Dokumen30 halamanCheeseman Blaw9e Inppt 16Suhel KararaBelum ada peringkat

- PS-bill of Exchange ActDokumen35 halamanPS-bill of Exchange ActPhani Kiran MangipudiBelum ada peringkat

- Equitable Remedies - NotesDokumen33 halamanEquitable Remedies - Notessabiti edwinBelum ada peringkat

- EndorsementsDokumen15 halamanEndorsementsSaadat Ullah Khan100% (1)

- Lawfully Yours: The Realm of Business, Government and LawDari EverandLawfully Yours: The Realm of Business, Government and LawBelum ada peringkat

- The Declaration of Independence: A Play for Many ReadersDari EverandThe Declaration of Independence: A Play for Many ReadersBelum ada peringkat

- Best Franchise FormDokumen5 halamanBest Franchise FormPitamber RohtanBelum ada peringkat

- WeatherDokumen5 halamanWeatherPà TépBelum ada peringkat

- 100 Steps To Developing Your FranchiseDokumen4 halaman100 Steps To Developing Your FranchisePitamber RohtanBelum ada peringkat

- General Questions and Possible AnswersDokumen29 halamanGeneral Questions and Possible AnswersPitamber RohtanBelum ada peringkat

- Labour LawsDokumen12 halamanLabour LawsPitamber RohtanBelum ada peringkat

- EndorseDokumen1 halamanEndorsePitamber RohtanBelum ada peringkat

- Student Notes ETHICSand SOCIALRDokumen8 halamanStudent Notes ETHICSand SOCIALRAziz JumanneBelum ada peringkat

- Partnership ActDokumen67 halamanPartnership ActPitamber RohtanBelum ada peringkat

- Bills of Exchange Payable at SightDokumen3 halamanBills of Exchange Payable at SightPitamber RohtanBelum ada peringkat

- How To Give Self Introduction in IterviewDokumen8 halamanHow To Give Self Introduction in IterviewJostin PunnasseryBelum ada peringkat

- Payment of Gratuity ActDokumen20 halamanPayment of Gratuity ActPitamber RohtanBelum ada peringkat

- How To Become Super StudentDokumen7 halamanHow To Become Super StudentPitamber RohtanBelum ada peringkat

- Sale of Goods ActDokumen6 halamanSale of Goods Actshipra.sangal4717Belum ada peringkat

- 10 Best Non Government OrganisationsDokumen3 halaman10 Best Non Government OrganisationsPitamber RohtanBelum ada peringkat

- ITSM Syllabus for Information Technology & Strategic ManagementDokumen3 halamanITSM Syllabus for Information Technology & Strategic ManagementPitamber RohtanBelum ada peringkat

- CommunicationDokumen12 halamanCommunicationFanueal Samson0% (1)

- Russell's Spoken English Private Limited.: Franchise Support and ROI DocumentDokumen3 halamanRussell's Spoken English Private Limited.: Franchise Support and ROI DocumentSanjay SuryadevraBelum ada peringkat

- Corruption in India: Causes and MeasuresDokumen2 halamanCorruption in India: Causes and MeasuresPitamber RohtanBelum ada peringkat

- Careers in Company SecretaryDokumen2 halamanCareers in Company SecretaryPitamber RohtanBelum ada peringkat

- Ublic Ector Nterprises: Module - 2 Business OrganisationsDokumen20 halamanUblic Ector Nterprises: Module - 2 Business Organisationsd-fbuser-65596417Belum ada peringkat

- Difference Between Hindu Undivided Family (HUF) and A Firm: InterestDokumen2 halamanDifference Between Hindu Undivided Family (HUF) and A Firm: InterestPitamber Rohtan100% (1)

- Difference Between A Press Release and A Press ReportDokumen1 halamanDifference Between A Press Release and A Press ReportPitamber Rohtan67% (3)

- Session 5: Business Organization: OBJECTIVE: When You Have Decided Which BusinessDokumen8 halamanSession 5: Business Organization: OBJECTIVE: When You Have Decided Which BusinessPitamber RohtanBelum ada peringkat

- Element of Relating To PartnershipDokumen15 halamanElement of Relating To PartnershipPitamber RohtanBelum ada peringkat

- How To Give Self Introduction in IterviewDokumen8 halamanHow To Give Self Introduction in IterviewJostin PunnasseryBelum ada peringkat

- Female Foeticide in IndiaDokumen2 halamanFemale Foeticide in IndiaPitamber RohtanBelum ada peringkat

- Internal and External Business EnvironmentDokumen7 halamanInternal and External Business EnvironmentMohammad RIzwan88% (34)

- Franchisee Application FormDokumen5 halamanFranchisee Application FormPitamber RohtanBelum ada peringkat

- NIL - Go-Bangayan Vs Ho - DigestDokumen3 halamanNIL - Go-Bangayan Vs Ho - DigestRegine GumbocBelum ada peringkat

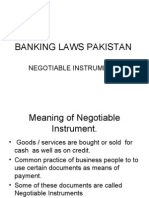

- Banking Laws Pakistan Negotiable InstrumentsDokumen57 halamanBanking Laws Pakistan Negotiable Instrumentsmzqace100% (8)

- Banking Practice & Proc. Course OutlineDokumen5 halamanBanking Practice & Proc. Course OutlineSuresh Vadde50% (2)

- Mercantile Law Bar Examination Q&ADokumen198 halamanMercantile Law Bar Examination Q&AJowelYabotBelum ada peringkat

- Court Rules Against Bank for Irregular Deposit of Crossed CheckDokumen7 halamanCourt Rules Against Bank for Irregular Deposit of Crossed ChecklouryBelum ada peringkat

- NIL - HolderDokumen2 halamanNIL - HolderMiu KawashimaBelum ada peringkat

- Promissory Note and Its ImportanceDokumen16 halamanPromissory Note and Its Importancepraboooo67% (3)

- 01 Chan Wan vs. Tan Kim, Et AlDokumen3 halaman01 Chan Wan vs. Tan Kim, Et AlNicaRejusoBelum ada peringkat

- 06 Puget Sound State Bank v. Washington Paving Co.Dokumen8 halaman06 Puget Sound State Bank v. Washington Paving Co.KathBelum ada peringkat

- Haresh Advani of Mumbai Vs Suraj Jagtiani On 24 AprilDokumen9 halamanHaresh Advani of Mumbai Vs Suraj Jagtiani On 24 AprilDeepak SharmaBelum ada peringkat

- Secrecy of Bank Deposits and Unclaimed Balances LawDokumen22 halamanSecrecy of Bank Deposits and Unclaimed Balances LawLailani Kato100% (4)

- 1991-1996 BAR Mercantile QuestionsDokumen63 halaman1991-1996 BAR Mercantile QuestionsasdgafsdgadfgBelum ada peringkat

- Caltex (Philippines) Inc. vs. CA GR 97753, 10 August 1992 - NegotiabilityDokumen5 halamanCaltex (Philippines) Inc. vs. CA GR 97753, 10 August 1992 - Negotiabilitykitakattt100% (1)

- Essential Guide to Letters of CreditDokumen11 halamanEssential Guide to Letters of CreditOna DlanorBelum ada peringkat

- Complete Internship - Report HIRADokumen52 halamanComplete Internship - Report HIRAHafsa AminBelum ada peringkat

- Rights of Drawers Banks and Holders in Bank Checks and Other CADokumen57 halamanRights of Drawers Banks and Holders in Bank Checks and Other CASiddharth Singh TomarBelum ada peringkat

- Mock Bar - Commercial Law PDFDokumen8 halamanMock Bar - Commercial Law PDFPatricia Anne GarciaBelum ada peringkat

- The Negotiable Instruments Law in a NutshellDokumen78 halamanThe Negotiable Instruments Law in a NutshelljaneBelum ada peringkat

- Philippines Supreme Court ruling on accommodation makers' liabilityDokumen6 halamanPhilippines Supreme Court ruling on accommodation makers' liabilityCJ MillenaBelum ada peringkat

- 2018 Bar Exam Syllabus in Mercantile Law PDFDokumen16 halaman2018 Bar Exam Syllabus in Mercantile Law PDFRalph Christian Lusanta FuentesBelum ada peringkat

- Section 11-16Dokumen6 halamanSection 11-16Jane GonzalesBelum ada peringkat

- General Awareness 2015 For All Upcoming ExamsDokumen59 halamanGeneral Awareness 2015 For All Upcoming ExamsJagannath JagguBelum ada peringkat

- Vs. The Court of Appeals and Philippine Commercial and Industrial Bank, RespondentsDokumen2 halamanVs. The Court of Appeals and Philippine Commercial and Industrial Bank, RespondentsRobee Marie IlaganBelum ada peringkat

- Abhishek Kumar Department of Management Studies Kumaun University, NainitalDokumen69 halamanAbhishek Kumar Department of Management Studies Kumaun University, NainitalAarav AroraBelum ada peringkat

- Expert Witness Affidavit by Attorney SampleDokumen24 halamanExpert Witness Affidavit by Attorney SampleCFLA, Inc100% (1)

- Uniform Commercial Code UCC Article 3Dokumen48 halamanUniform Commercial Code UCC Article 3val_guralnikBelum ada peringkat

- Philacor Credit Corp Vs CIRDokumen23 halamanPhilacor Credit Corp Vs CIRJeanne CalalinBelum ada peringkat

- Nil Notes PDFDokumen93 halamanNil Notes PDFvilma marceloBelum ada peringkat

- Metrobank and Solid Bank liable for crossed checksDokumen2 halamanMetrobank and Solid Bank liable for crossed checksRaiden DalusagBelum ada peringkat

- Stamp Duty BookDokumen18 halamanStamp Duty BookGeetika Anand100% (2)