Anda mungkin juga menyukai

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Cheminot Had Lost by Striking in The Month of December. We Had Just Finished Our Shift and Were Locking UpDokumen4 halamanCheminot Had Lost by Striking in The Month of December. We Had Just Finished Our Shift and Were Locking Upmaviss828Belum ada peringkat

- ADVICE COLUMN Danny HaywardDokumen22 halamanADVICE COLUMN Danny Haywardmaviss828Belum ada peringkat

- Erotoplasty Issue 4 PDFDokumen118 halamanErotoplasty Issue 4 PDFmaviss828Belum ada peringkat

- Slightly Broken For EPDokumen6 halamanSlightly Broken For EPmaviss828Belum ada peringkat

- Romania RedivisusDokumen37 halamanRomania Redivisusmaviss828Belum ada peringkat

- Hix Eros 7 (August 2016) PDFDokumen47 halamanHix Eros 7 (August 2016) PDFmaviss828Belum ada peringkat

- Why We Lost The WarDokumen282 halamanWhy We Lost The Warmaviss828100% (1)

- Speaking About GodardDokumen175 halamanSpeaking About Godardmaviss828Belum ada peringkat

- Hix Eros 6Dokumen66 halamanHix Eros 6maviss828Belum ada peringkat

- Marker Chris The Forthright SpiritDokumen95 halamanMarker Chris The Forthright Spiritmarco_alcalá_1Belum ada peringkat

- Class Struggle and This Thing Named „The Middle East‟ by Melancholic Troglodytes نوشتۀ غارنشینان مالیخولیاییDokumen298 halamanClass Struggle and This Thing Named „The Middle East‟ by Melancholic Troglodytes نوشتۀ غارنشینان مالیخولیاییTae AtehBelum ada peringkat

- Hume, MemorandaDokumen28 halamanHume, Memorandamaviss828Belum ada peringkat

- Manfred Kuehn, Scottish Common Sense in GermanyDokumen300 halamanManfred Kuehn, Scottish Common Sense in Germanymaviss828Belum ada peringkat

- The New Dialectic and Marxs CapitalDokumen272 halamanThe New Dialectic and Marxs Capitalmaviss828100% (1)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Midsemester Practice QuestionsDokumen6 halamanMidsemester Practice Questionsoshane126Belum ada peringkat

- Chapter 02Dokumen15 halamanChapter 02sanket_yavalkarBelum ada peringkat

- 50 Best Startup Cities - ValuerDokumen56 halaman50 Best Startup Cities - ValuerAlejandro AriasBelum ada peringkat

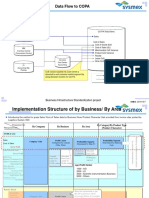

- Data Flow To COPA: Business Infrastructure Standardization ProjectDokumen3 halamanData Flow To COPA: Business Infrastructure Standardization ProjectT SAIKIRANBelum ada peringkat

- AJC Case Analysis.Dokumen4 halamanAJC Case Analysis.sunny rahulBelum ada peringkat

- Chapter 06 - Risk & ReturnDokumen42 halamanChapter 06 - Risk & Returnmnr81Belum ada peringkat

- Course Syllabus 01 Technical Analysis Training Course PDFDokumen4 halamanCourse Syllabus 01 Technical Analysis Training Course PDFDHANESH UDDHAV PATIL0% (1)

- Relationship of Nifty-50 With Reliance Infrastructure LTDDokumen3 halamanRelationship of Nifty-50 With Reliance Infrastructure LTDPrabhaBelum ada peringkat

- Ch4ProbsetTVM13ed - MasterDokumen4 halamanCh4ProbsetTVM13ed - MasterRisaline CuaresmaBelum ada peringkat

- A Mutual Fund is a Common Pool of Money in to Which Investors With Common Investment Objective Place Their Contributions That Are to Be Invested in Accordance With the Stated Investment Objective of the SchemeDokumen6 halamanA Mutual Fund is a Common Pool of Money in to Which Investors With Common Investment Objective Place Their Contributions That Are to Be Invested in Accordance With the Stated Investment Objective of the SchemeKumaran MohanBelum ada peringkat

- 4AC0 01 AccountingDokumen20 halaman4AC0 01 AccountingShakib Bin Mahmud WcmBelum ada peringkat

- Bajaj Allianz General Insurance Company LimitedDokumen108 halamanBajaj Allianz General Insurance Company LimitedhemangchauhanBelum ada peringkat

- Project Blue PWC 2012Dokumen250 halamanProject Blue PWC 2012carlonewmannBelum ada peringkat

- Mth302 Assignmnet SolutionDokumen6 halamanMth302 Assignmnet Solutioncs619finalproject.comBelum ada peringkat

- Previous Year Question Papers (Theory) PDFDokumen4 halamanPrevious Year Question Papers (Theory) PDFSiva KumarBelum ada peringkat

- Aether Analytics October ConspectusDokumen73 halamanAether Analytics October ConspectusAlex Bernal, CMTBelum ada peringkat

- SC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsDokumen5 halamanSC's NRA Judgement On Sec.68: Threadbare Analysis of Subsequent DecisionsArchit ShethBelum ada peringkat

- Basic Cash Formulas Manual April 2009 - 2.8Dokumen123 halamanBasic Cash Formulas Manual April 2009 - 2.8horns2034Belum ada peringkat

- BOP India BullsDokumen19 halamanBOP India Bullsthexplorer008Belum ada peringkat

- Are Profit Maximizers Wealth CreatorsDokumen36 halamanAre Profit Maximizers Wealth Creatorskanika5985Belum ada peringkat

- Class 1 Investments BKM Chapter9Dokumen19 halamanClass 1 Investments BKM Chapter9Daniel PortellaBelum ada peringkat

- OYO ROOMS Economics AssignmentDokumen22 halamanOYO ROOMS Economics AssignmentNikhil TanwarBelum ada peringkat

- Convergence of Indian Accounting Standards With Ifrs Prospects and ChallengesDokumen11 halamanConvergence of Indian Accounting Standards With Ifrs Prospects and Challengesksmuthupandian2098Belum ada peringkat

- CA IPC Capital Budgeting Most Important Questions 1TR8KKBFDokumen12 halamanCA IPC Capital Budgeting Most Important Questions 1TR8KKBFChandreshBelum ada peringkat

- Ib On GranitesDokumen23 halamanIb On Granitesaks14uBelum ada peringkat

- Democratic Republic Congo Mining Guide PDFDokumen40 halamanDemocratic Republic Congo Mining Guide PDFtatekBelum ada peringkat

- A Study OF Bank Profitability Between Commercial and Islamic Bank Between 1997 To 2011: Maybank Berhad and Bank Islam Malaysia BerhadDokumen47 halamanA Study OF Bank Profitability Between Commercial and Islamic Bank Between 1997 To 2011: Maybank Berhad and Bank Islam Malaysia BerhadAhmad FikriBelum ada peringkat

- Apl Apollo - Business Analysis Report: by Subroto BaulDokumen8 halamanApl Apollo - Business Analysis Report: by Subroto BaulSubroto BaulBelum ada peringkat

- Aza Smart Pen Pro-Forma Income Statement: Less: Cost of Sales (Notes 1 & 2) Gross ProfitDokumen1 halamanAza Smart Pen Pro-Forma Income Statement: Less: Cost of Sales (Notes 1 & 2) Gross ProfitAzran AfandiBelum ada peringkat