Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- ListDokumen6 halamanListalonsoBelum ada peringkat

- Free Study Material For Bankpo Clerk SBI IBPS Rbi Banking GlossaryDokumen136 halamanFree Study Material For Bankpo Clerk SBI IBPS Rbi Banking GlossaryniteshBelum ada peringkat

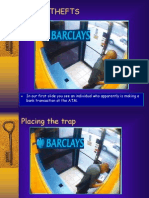

- Atm Thefts: in Our First Slide You See An Individual Who Apparently Is Making A Bank Transaction at The ATMDokumen17 halamanAtm Thefts: in Our First Slide You See An Individual Who Apparently Is Making A Bank Transaction at The ATMLeia Grace ElaineBelum ada peringkat

- List of Registered Independent Sales OrganizationsDokumen53 halamanList of Registered Independent Sales Organizationscdill70100% (1)

- Machine Operators Case StudyDokumen1 halamanMachine Operators Case StudyAkshata BhosaleBelum ada peringkat

- MX5600S - Operator Manual-V01.00.00Dokumen71 halamanMX5600S - Operator Manual-V01.00.00Suhrowardi RasyidBelum ada peringkat

- Scalable Deposit Module: ThebunchmaximumoffiftyitemscanbereducedviathecustomerapplicationDokumen116 halamanScalable Deposit Module: ThebunchmaximumoffiftyitemscanbereducedviathecustomerapplicationnunocoitoBelum ada peringkat

- Far East Bank Trust CompanyDokumen2 halamanFar East Bank Trust Companyazalea marie maquiranBelum ada peringkat

- HDFC Bank: Revision of Interest Rates On HDFC Bank Savings Bank DepositsDokumen8 halamanHDFC Bank: Revision of Interest Rates On HDFC Bank Savings Bank Depositsanirudh birlaBelum ada peringkat

- SBI Account Opening FormDokumen9 halamanSBI Account Opening FormkhatrinaveenBelum ada peringkat

- Under Supervision: Submitted byDokumen71 halamanUnder Supervision: Submitted byNeha PassiBelum ada peringkat

- ATM White Label ATM PDFDokumen2 halamanATM White Label ATM PDFSURENDRA SAHUBelum ada peringkat

- Aviation Insurance ProjectDokumen58 halamanAviation Insurance ProjectAkshata BhosaleBelum ada peringkat

- Swot of Maruti SuzukiDokumen1 halamanSwot of Maruti SuzukiAkshata BhosaleBelum ada peringkat

- Intro of Maruti SuzukiDokumen7 halamanIntro of Maruti SuzukiAkshata BhosaleBelum ada peringkat

- The Impact and Role of Information Technology in Banking Development in NigeriaDokumen18 halamanThe Impact and Role of Information Technology in Banking Development in Nigeriaisrael0% (1)

- Vietnam National University - Ho Chi Minh City International UniversityDokumen17 halamanVietnam National University - Ho Chi Minh City International UniversityThiên ÂnBelum ada peringkat

- GE Café™ "This Is Really Big" RebateDokumen2 halamanGE Café™ "This Is Really Big" RebateKitchens of ColoradoBelum ada peringkat

- Object Oriented Software Engineering: Practical FileDokumen33 halamanObject Oriented Software Engineering: Practical FileVidhi KishorBelum ada peringkat

- Approach Paper: It-Enabled Financial InclusionDokumen28 halamanApproach Paper: It-Enabled Financial InclusionAbdoul FerozeBelum ada peringkat

- EGov User ManualDokumen67 halamanEGov User Manualpedro jose33% (6)

- Ibea PDFDokumen37 halamanIbea PDFpratz1996Belum ada peringkat

- Account Statement 25-05-2023T02 58 36Dokumen1 halamanAccount Statement 25-05-2023T02 58 36SHEHERYAR QAZI 26488Belum ada peringkat

- Flexi Current Account: (Effective From Jul 01, 2019 Charges Are Exclusive of GST)Dokumen4 halamanFlexi Current Account: (Effective From Jul 01, 2019 Charges Are Exclusive of GST)Athish KumarBelum ada peringkat

- 2023 09 12 22 47 30aug 23 - 110042Dokumen9 halaman2023 09 12 22 47 30aug 23 - 110042pradeepBelum ada peringkat

- TRANSDATE205077767021213 1672554386037pdf 230101 122644Dokumen3 halamanTRANSDATE205077767021213 1672554386037pdf 230101 122644MD NAZMULBelum ada peringkat

- Impact of Digitalisation On Bank Performance: A Study of Indian BanksDokumen15 halamanImpact of Digitalisation On Bank Performance: A Study of Indian BanksHardik MistryBelum ada peringkat

- FAQ Unifi Air - For Consumer - Website Update - 23032020Dokumen6 halamanFAQ Unifi Air - For Consumer - Website Update - 23032020RAZALI BIN AHMAD MoeBelum ada peringkat

- Case StudyDokumen5 halamanCase StudyShubham BhatewaraBelum ada peringkat

- ATM Terminal Security Using Fingerprint Recognition: Vaibhav R. Pandit Kirti A. Joshi Narendra G. Bawane, PH.DDokumen5 halamanATM Terminal Security Using Fingerprint Recognition: Vaibhav R. Pandit Kirti A. Joshi Narendra G. Bawane, PH.Dseunnuga93Belum ada peringkat

- Kalpana Bisen Paper On Dress CodeDokumen19 halamanKalpana Bisen Paper On Dress CodeKalpana BisenBelum ada peringkat

- SBI Fee & ChargesDokumen16 halamanSBI Fee & ChargesAks SomvanshiBelum ada peringkat

- Go Green: Intelligent Energy Saving SystemDokumen9 halamanGo Green: Intelligent Energy Saving SystemM. Adil NasirBelum ada peringkat

- A Comparative Analysis On Green Banking PDFDokumen11 halamanA Comparative Analysis On Green Banking PDFmjoyroyBelum ada peringkat