Anda mungkin juga menyukai

- Credit Trans Reviewer Nature of Guaranty and SuretyshipDokumen12 halamanCredit Trans Reviewer Nature of Guaranty and Suretyshipzal50% (2)

- Assignment On Effects of Ultra Vires TransactionsDokumen5 halamanAssignment On Effects of Ultra Vires Transactionssaksham ahuja100% (1)

- 36 People's Bank and Trust Co. v. OdomDokumen2 halaman36 People's Bank and Trust Co. v. OdomKarla Bee100% (1)

- Fish Pond LeaseDokumen4 halamanFish Pond LeaseScarlet Fernandez100% (1)

- Corporate PersonalityDokumen3 halamanCorporate PersonalitymanjushreeBelum ada peringkat

- Case Summaries - Contract Law Unit 1Dokumen10 halamanCase Summaries - Contract Law Unit 1Laura HawkinsBelum ada peringkat

- Lifting The Corporate Veil - P M BakshiDokumen19 halamanLifting The Corporate Veil - P M Bakshiv_singh28Belum ada peringkat

- Guarantee Case LawDokumen20 halamanGuarantee Case LawJagii Sandhu100% (4)

- Jeff Thigpen Victim ReportDokumen95 halamanJeff Thigpen Victim ReportForeclosure Fraud0% (1)

- Delegated LegislationDokumen17 halamanDelegated LegislationParunjeet Singh Chawla100% (7)

- Chanakya National Law University, Patna: Continuing Guarantee: Judicial InterpretationDokumen19 halamanChanakya National Law University, Patna: Continuing Guarantee: Judicial InterpretationAdi 10eoBelum ada peringkat

- International Law DigestDokumen148 halamanInternational Law DigestDinah Pearl Campos75% (4)

- Utilitarianism & Bentham: Nature Has Placed Mankind Under The Governance of Two Sovereign Masters, Pain and PleasureDokumen19 halamanUtilitarianism & Bentham: Nature Has Placed Mankind Under The Governance of Two Sovereign Masters, Pain and PleasureKarthik Ricky100% (1)

- 1.contract Ii (Contracts of Guarantee An Analysis)Dokumen11 halaman1.contract Ii (Contracts of Guarantee An Analysis)Palak ThakrarBelum ada peringkat

- Contract-II Case Review Of: Maharashtra National Law University, AurangabadDokumen9 halamanContract-II Case Review Of: Maharashtra National Law University, AurangabadSaurabh Krishna SinghBelum ada peringkat

- Comparative Analysis of Companies Act, 1956 and Companies Act 2013Dokumen8 halamanComparative Analysis of Companies Act, 1956 and Companies Act 2013Archisman GuptaBelum ada peringkat

- Possibility of Performance and Terms of ContractDokumen27 halamanPossibility of Performance and Terms of ContractSnr Berel ShepherdBelum ada peringkat

- Introduction of Epistolary JurisdictionDokumen25 halamanIntroduction of Epistolary JurisdictionZACHARIAH MANKIRBelum ada peringkat

- P Nedumaran Vs The State of Tamil Nadu 14082001 Mt010299COM294450 PDFDokumen3 halamanP Nedumaran Vs The State of Tamil Nadu 14082001 Mt010299COM294450 PDFAnushkaBelum ada peringkat

- Maharashtra National Law University Mumbai: Promoters-Duties, Liabilities and Rights'Dokumen11 halamanMaharashtra National Law University Mumbai: Promoters-Duties, Liabilities and Rights'Ayashkant ParidaBelum ada peringkat

- Hurt and Grievous HurtDokumen2 halamanHurt and Grievous HurtHarshit SharmaBelum ada peringkat

- Law Mantra: Consumer Protection Act and Air CarriageDokumen8 halamanLaw Mantra: Consumer Protection Act and Air CarriageLAW MANTRABelum ada peringkat

- Vanishing CompaniesDokumen7 halamanVanishing CompaniesVinay Artwani100% (1)

- Essay, 71Dokumen4 halamanEssay, 71Ritisha ChoudharyBelum ada peringkat

- General Principles of Insurance LawDokumen12 halamanGeneral Principles of Insurance LawCarina Amor ClaveriaBelum ada peringkat

- HC Order 9 Sept 2015Dokumen30 halamanHC Order 9 Sept 2015Moneylife Foundation100% (1)

- Moses v. MacferlanDokumen1 halamanMoses v. MacferlanBhumikaBelum ada peringkat

- Corporate Law Case StudiesDokumen2 halamanCorporate Law Case Studiesshaurya JainBelum ada peringkat

- Privity of ContractDokumen12 halamanPrivity of ContractR100% (1)

- Golaknath CaseDokumen6 halamanGolaknath CaseRadhikaBelum ada peringkat

- Issue 1Dokumen8 halamanIssue 1Pranay BhardwajBelum ada peringkat

- 7 Differences Between Constitutional Administrative LawDokumen4 halaman7 Differences Between Constitutional Administrative LawVaalu MuthuBelum ada peringkat

- Matrimonial Property Law in India Need oDokumen24 halamanMatrimonial Property Law in India Need orishabhsingh261100% (1)

- CHAPTER-14: C I R P U I & B C, 2016: Orporate Nsolvency Esolution Rocess Nder Nsolvency Ankruptcy ODEDokumen27 halamanCHAPTER-14: C I R P U I & B C, 2016: Orporate Nsolvency Esolution Rocess Nder Nsolvency Ankruptcy ODESrishti NigamBelum ada peringkat

- Role of Minors in Limited Liability PartnershipDokumen5 halamanRole of Minors in Limited Liability PartnershipVanessa ThomasBelum ada peringkat

- A Report On Procedure of Winding Up Partnership FirmDokumen7 halamanA Report On Procedure of Winding Up Partnership FirmSatellite CafeBelum ada peringkat

- RE Mptive Ight: V.B.Rangaraj v. V.B.GopalakrishnanDokumen3 halamanRE Mptive Ight: V.B.Rangaraj v. V.B.GopalakrishnanVishnu SunBelum ada peringkat

- Corporate Law Project SubDokumen20 halamanCorporate Law Project SubDIWAKAR CHIRANIABelum ada peringkat

- Suggested Answers of Company Law June 2019 Old Syl-Executive-RevisionDokumen15 halamanSuggested Answers of Company Law June 2019 Old Syl-Executive-RevisionjesurajajosephBelum ada peringkat

- Law of AttemptDokumen5 halamanLaw of AttemptAkashBelum ada peringkat

- Morgan Stanley Mutual Fund Vskartick Das 1994 SCC (4) 225Dokumen20 halamanMorgan Stanley Mutual Fund Vskartick Das 1994 SCC (4) 225sai kiran gudisevaBelum ada peringkat

- THE Honourable Supreme Court OF India: BeforeDokumen15 halamanTHE Honourable Supreme Court OF India: BeforeSagar RajBelum ada peringkat

- Sem5 Jurisprudence PDFDokumen16 halamanSem5 Jurisprudence PDFMuskan KhatriBelum ada peringkat

- Ipo 1Dokumen7 halamanIpo 1Aditya SinghBelum ada peringkat

- Government SubsidiesDokumen6 halamanGovernment Subsidiessamy7541Belum ada peringkat

- Ankesh Sir CLM ProjectDokumen11 halamanAnkesh Sir CLM ProjectSaket RaoBelum ada peringkat

- Role of Adjudicating Authority in CIRP & Liquidation Under Insolvency and Bankruptcy LawDokumen11 halamanRole of Adjudicating Authority in CIRP & Liquidation Under Insolvency and Bankruptcy LawShachi SinghBelum ada peringkat

- Constitutional Law IRACDokumen7 halamanConstitutional Law IRACChinmay GuptaBelum ada peringkat

- T-17 - Respondents' Written SubmissionDokumen20 halamanT-17 - Respondents' Written SubmissionMayank TripathiBelum ada peringkat

- Case Comment Appelant Ram Avtar v. Respodent State of U.PDokumen3 halamanCase Comment Appelant Ram Avtar v. Respodent State of U.PVivek GutamBelum ada peringkat

- Awasthi's ProjectDokumen26 halamanAwasthi's ProjectJyoti SharmaBelum ada peringkat

- Alternative Dispute Resolution in Bangladesh: Barrister Tahmidur Rahman On 4th January 2023Dokumen10 halamanAlternative Dispute Resolution in Bangladesh: Barrister Tahmidur Rahman On 4th January 2023Md Abu Taher BhuiyanBelum ada peringkat

- Manager, ICICI Bank V Prakash Kaur and OrsDokumen10 halamanManager, ICICI Bank V Prakash Kaur and Orsarunav_guha_royroyBelum ada peringkat

- Assignment On Contract Law 1Dokumen17 halamanAssignment On Contract Law 1Aashi watsBelum ada peringkat

- Understanding of Compulsorily Convertible Debentures Vinod KothariDokumen7 halamanUnderstanding of Compulsorily Convertible Debentures Vinod KothariNazir kondkariBelum ada peringkat

- Unfair Labour PracticesDokumen16 halamanUnfair Labour PracticesMishika Pandita0% (1)

- Pritam Singh v. State, AIR 1950 SC 169: 1950 SCR 453 Article 141 of The Indian Constitution Manikchand v. Elias, AIR 1969 SC 751Dokumen4 halamanPritam Singh v. State, AIR 1950 SC 169: 1950 SCR 453 Article 141 of The Indian Constitution Manikchand v. Elias, AIR 1969 SC 751kakuBelum ada peringkat

- Gherulal Parakh v. Mahadeodas Maiya and Ors. 1959 AIR 781Dokumen2 halamanGherulal Parakh v. Mahadeodas Maiya and Ors. 1959 AIR 781SHRIKANT VERMABelum ada peringkat

- Assignment 2ndDokumen14 halamanAssignment 2ndSwarup Das DiptoBelum ada peringkat

- Nature and Scope of Law of Torts - Author - Lakshmi SomanathanDokumen5 halamanNature and Scope of Law of Torts - Author - Lakshmi SomanathanJasmine Singh100% (1)

- Law of Torts - KLE Law Academy NotesDokumen133 halamanLaw of Torts - KLE Law Academy NotesSupriya UpadhyayulaBelum ada peringkat

- Aligarh Muslim University Malappuram Centre, Kerala: PROJECT Report On Topic LIFE INSURANCE Law of InsuranceDokumen12 halamanAligarh Muslim University Malappuram Centre, Kerala: PROJECT Report On Topic LIFE INSURANCE Law of InsuranceSadhvi SinghBelum ada peringkat

- Torts Project-Sem 1 - ScribdDokumen16 halamanTorts Project-Sem 1 - ScribdSaksham MarwahBelum ada peringkat

- M. S. Anirudhan Vs The Thomco's Bank LTDDokumen6 halamanM. S. Anirudhan Vs The Thomco's Bank LTDAnkit JindalBelum ada peringkat

- Expanding Horizon of Freedom of Speech ADokumen31 halamanExpanding Horizon of Freedom of Speech AAwan Ajmal AziziBelum ada peringkat

- Constitutional Set Up of East India CompanyDokumen20 halamanConstitutional Set Up of East India CompanyRahulAbHishekBelum ada peringkat

- Continuing Guarantee AnsDokumen5 halamanContinuing Guarantee AnsSwarna LathaBelum ada peringkat

- Notes Ica and SogaDokumen38 halamanNotes Ica and SogahaloXDBelum ada peringkat

- Table of ContentsDokumen29 halamanTable of ContentsKarthik RickyBelum ada peringkat

- Bentham's UtilitarianismDokumen6 halamanBentham's UtilitarianismKarthik RickyBelum ada peringkat

- Income Exempt From TaxDokumen1 halamanIncome Exempt From TaxKarthik RickyBelum ada peringkat

- Damodaram Sanjivayya National Law UniversityDokumen6 halamanDamodaram Sanjivayya National Law UniversityKarthik RickyBelum ada peringkat

- SomethingDokumen10 halamanSomethingKarthik RickyBelum ada peringkat

- Abstract EnviormentDokumen1 halamanAbstract EnviormentKarthik RickyBelum ada peringkat

- StiglitzDokumen2 halamanStiglitzKarthik RickyBelum ada peringkat

- Vested InterestDokumen17 halamanVested InterestKarthik RickyBelum ada peringkat

- Class Test 2 2Dokumen19 halamanClass Test 2 2Karthik RickyBelum ada peringkat

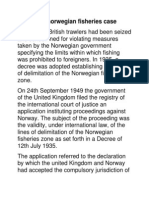

- The Anglo Norwegian Fisheries CaseDokumen37 halamanThe Anglo Norwegian Fisheries CaseKarthik RickyBelum ada peringkat

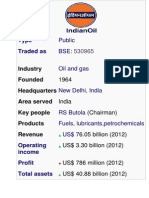

- Type Traded As: Public BSE NSE Oil and GasDokumen2 halamanType Traded As: Public BSE NSE Oil and GasKarthik RickyBelum ada peringkat

- History and Origin of CopyrightDokumen1 halamanHistory and Origin of CopyrightKarthik RickyBelum ada peringkat

- AcknowledgementDokumen14 halamanAcknowledgementKarthik RickyBelum ada peringkat

- The Anglo Norwegian Fisheries CaseDokumen37 halamanThe Anglo Norwegian Fisheries CaseKarthik RickyBelum ada peringkat

- Intl-Law 4-9Dokumen9 halamanIntl-Law 4-9Karthik RickyBelum ada peringkat

- JurisprudenceDokumen24 halamanJurisprudenceKarthik RickyBelum ada peringkat

- Role of Dharma in Ancient Indian JurisprudenceDokumen9 halamanRole of Dharma in Ancient Indian JurisprudenceKarthik RickyBelum ada peringkat

- A Review of SylabusDokumen154 halamanA Review of SylabusKarthik RickyBelum ada peringkat

- History MarketingDokumen2 halamanHistory MarketingKarthik RickyBelum ada peringkat

- The Anglo-Norwegian Fisheries CaseDokumen3 halamanThe Anglo-Norwegian Fisheries CaseKarthik RickyBelum ada peringkat

- Child Labour (Learning Form Developing Countries)Dokumen2 halamanChild Labour (Learning Form Developing Countries)Karthik RickyBelum ada peringkat

- Dowry DeathDokumen15 halamanDowry DeathKarthik RickyBelum ada peringkat

- Rent Agreement-2Dokumen1 halamanRent Agreement-2raghu rajBelum ada peringkat

- 2 Introduction To ContractDokumen5 halaman2 Introduction To ContractMax TanBelum ada peringkat

- Law On Credit Transactions 4 Year Review Class St. Thomas More School of LawDokumen181 halamanLaw On Credit Transactions 4 Year Review Class St. Thomas More School of LawAlexis EnriquezBelum ada peringkat

- Chapter 12 Quiz - Business LawDokumen2 halamanChapter 12 Quiz - Business LawRayonneBelum ada peringkat

- RealDokumen5 halamanRealanvit seemanshBelum ada peringkat

- Canadian Law - Inside The ContractDokumen2 halamanCanadian Law - Inside The ContractNic PaolellaBelum ada peringkat

- Contracts: 1. DEFINITION. The NCC Defines A Contract As "A Meeting of Minds Between Two Persons Whereby (Art. 1305, NCC)Dokumen9 halamanContracts: 1. DEFINITION. The NCC Defines A Contract As "A Meeting of Minds Between Two Persons Whereby (Art. 1305, NCC)VIRILITER AGITEBelum ada peringkat

- 5 Hire PurchaseDokumen71 halaman5 Hire PurchaseAmirHakimRusliBelum ada peringkat

- Case Laws ContractDokumen24 halamanCase Laws ContractVaibhav KaulBelum ada peringkat

- Allied Banking Corp. vs. YujuicoDokumen10 halamanAllied Banking Corp. vs. YujuicospBelum ada peringkat

- Seminar 7 WorksheetDokumen3 halamanSeminar 7 WorksheetRishabhBelum ada peringkat

- BFDA Volume 35 Issue 1 Pages 125-199Dokumen74 halamanBFDA Volume 35 Issue 1 Pages 125-199inesse.berkaneBelum ada peringkat

- Commercial Tenancy Act BC PDFDokumen2 halamanCommercial Tenancy Act BC PDFKellyBelum ada peringkat

- ASSIGNMENT AND ASSUMPTION of CONTRACT AGREEMENTDokumen3 halamanASSIGNMENT AND ASSUMPTION of CONTRACT AGREEMENTCizca Tubice ObreBelum ada peringkat

- Notes On IndemnityDokumen6 halamanNotes On Indemnitymonish bBelum ada peringkat

- LAW 299: Business Law (Offer) : Main Source of ReferenceDokumen30 halamanLAW 299: Business Law (Offer) : Main Source of ReferenceNaqi LemanBelum ada peringkat

- Chapter 3 - Form of Contracts: Reviewer in Obligations and ContractsDokumen1 halamanChapter 3 - Form of Contracts: Reviewer in Obligations and ContractsJozelle Grace PadelBelum ada peringkat

- Pledge (Articles 2085-2123)Dokumen14 halamanPledge (Articles 2085-2123)Aessie Anne Morilla Cagurangan100% (1)

- CONTRACT LEASE - PhilGEPS PostingDokumen7 halamanCONTRACT LEASE - PhilGEPS PostingNicole Solano AnditBelum ada peringkat

- Assigment Business Law Group 3 - 230707 - 205012Dokumen26 halamanAssigment Business Law Group 3 - 230707 - 205012nurinBelum ada peringkat

- VIKRANTDokumen246 halamanVIKRANTVIKRANTBelum ada peringkat

- Classification of Contract Project WorkDokumen10 halamanClassification of Contract Project Workhithan mBelum ada peringkat

- Lease Agreement Hourly 1 Day RentalDokumen1 halamanLease Agreement Hourly 1 Day RentaltharleylawBelum ada peringkat

- Contingent ContractsDokumen2 halamanContingent ContractsMOHAMMED ALI CHOWDHURY100% (1)

- TC 174353 3Dokumen1 halamanTC 174353 3Anwarul HoqueBelum ada peringkat