Anda mungkin juga menyukai

- Manatee County, FL: Sold Summary InventoryDokumen3 halamanManatee County, FL: Sold Summary InventoryTHESERENAGROUPBelum ada peringkat

- Tailgating Ebook From The Serena Group &Dokumen28 halamanTailgating Ebook From The Serena Group &THESERENAGROUPBelum ada peringkat

- Heritage Harbour, Bradenton, Zip Code, 34212, Real Estate, Data, Statistics, Information, Market Report.Dokumen1 halamanHeritage Harbour, Bradenton, Zip Code, 34212, Real Estate, Data, Statistics, Information, Market Report.THESERENAGROUPBelum ada peringkat

- Bradenton, Sarasota, Manatee and Sarasota County, Real Estate, Market, Statistics, Report, DataDokumen4 halamanBradenton, Sarasota, Manatee and Sarasota County, Real Estate, Market, Statistics, Report, DataTHESERENAGROUPBelum ada peringkat

- Robert Serena, Certified, Distressed Property, Expert, Specialist, Short Sale, REO, Bank Owned, Foreclosure, Agent ResumeDokumen2 halamanRobert Serena, Certified, Distressed Property, Expert, Specialist, Short Sale, REO, Bank Owned, Foreclosure, Agent ResumeTHESERENAGROUPBelum ada peringkat

- Heritage Harbour, Bradenton, FL, Real Estate, Homes For Sale, Market, Report, Statistics, News, DataDokumen6 halamanHeritage Harbour, Bradenton, FL, Real Estate, Homes For Sale, Market, Report, Statistics, News, DataTHESERENAGROUPBelum ada peringkat

- Zillow Says 3yrs! Buying VS Renting A HomeDokumen1 halamanZillow Says 3yrs! Buying VS Renting A HomeTHESERENAGROUPBelum ada peringkat

- Bradenton, Sarasota, Florida, Home Buying, Guide, Book, Information, ReportDokumen27 halamanBradenton, Sarasota, Florida, Home Buying, Guide, Book, Information, ReportTHESERENAGROUPBelum ada peringkat

- Heritage Harbour, Bradenton, River Strand, Golf Membership, Information, 2011Dokumen1 halamanHeritage Harbour, Bradenton, River Strand, Golf Membership, Information, 2011THESERENAGROUPBelum ada peringkat

- River Sound Floorplans and FeaturesDokumen3 halamanRiver Sound Floorplans and FeaturesTHESERENAGROUPBelum ada peringkat

- Manatee County, Distressed Property, Foreclosure, Short Sale, Statistics, Report, Data - Aug 2010-Aug 2011Dokumen9 halamanManatee County, Distressed Property, Foreclosure, Short Sale, Statistics, Report, Data - Aug 2010-Aug 2011THESERENAGROUPBelum ada peringkat

- Heritage Harbour, Bradenton, FL, Real Estate, Statistics, Market Reports, - 2-2-11Dokumen2 halamanHeritage Harbour, Bradenton, FL, Real Estate, Statistics, Market Reports, - 2-2-11THESERENAGROUPBelum ada peringkat

- THE CAT AND THE OPEN HOUSE by Suni ByrnsDokumen1 halamanTHE CAT AND THE OPEN HOUSE by Suni ByrnsTHESERENAGROUPBelum ada peringkat

- Sarasota Florida Article - Authored by US Airways Http://usairwaysmag - Com/articles/welcome - To - SarasotaDokumen24 halamanSarasota Florida Article - Authored by US Airways Http://usairwaysmag - Com/articles/welcome - To - SarasotaTHESERENAGROUPBelum ada peringkat

- Bradenton, Real Estate, Homes For Sale, Home Values, Market Report, and Statistics - For Heritage Harbour, Bradenton, FLDokumen6 halamanBradenton, Real Estate, Homes For Sale, Home Values, Market Report, and Statistics - For Heritage Harbour, Bradenton, FLTHESERENAGROUPBelum ada peringkat

- Sarasota, Bradenton, Real Estate Statistics, Reports, Statistical Data Charts, Real Estate Market Information, Home Value Information, - 1st Quarter Statistics Report for 2010 - by National Association of REALTORSDokumen7 halamanSarasota, Bradenton, Real Estate Statistics, Reports, Statistical Data Charts, Real Estate Market Information, Home Value Information, - 1st Quarter Statistics Report for 2010 - by National Association of REALTORSTHESERENAGROUPBelum ada peringkat

- Bradenton, Sarasota, Manatee County, East Manatee County, Sarasota County, Real Estate, Marketing PlanDokumen10 halamanBradenton, Sarasota, Manatee County, East Manatee County, Sarasota County, Real Estate, Marketing PlanTHESERENAGROUPBelum ada peringkat

- Short Sale and Bank Owned Real Estate Statistics, Report, For Bradenton, Manatee County, Florida, 2-22-10Dokumen2 halamanShort Sale and Bank Owned Real Estate Statistics, Report, For Bradenton, Manatee County, Florida, 2-22-10THESERENAGROUPBelum ada peringkat

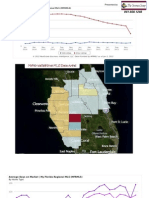

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Sales AbsorbtionDokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Sales AbsorbtionTHESERENAGROUPBelum ada peringkat

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Months Supply of Inventory Uder Contract Vs SoldDokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Months Supply of Inventory Uder Contract Vs SoldTHESERENAGROUPBelum ada peringkat

- Lakewood Ranch, Bradenton, Real Estate - Market Update, Statistics, MLS Report, InformationDokumen1 halamanLakewood Ranch, Bradenton, Real Estate - Market Update, Statistics, MLS Report, InformationTHESERENAGROUPBelum ada peringkat

- Bradenton Real Estate, Heritage Harbour, Home Values, Statistics, ReportsDokumen2 halamanBradenton Real Estate, Heritage Harbour, Home Values, Statistics, ReportsTHESERENAGROUPBelum ada peringkat

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Avg Price Per SQ - Ft.Dokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Avg Price Per SQ - Ft.THESERENAGROUPBelum ada peringkat

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Sold Price-List Price ComparisonDokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Sold Price-List Price ComparisonTHESERENAGROUPBelum ada peringkat

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Median PriceDokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Median PriceTHESERENAGROUPBelum ada peringkat

- BRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Supply and DemandDokumen2 halamanBRADENTON REAL ESTATE, HERITAGE HARBOUR, HOME VALUES, STATISTICS, REPORTS, Supply and DemandTHESERENAGROUPBelum ada peringkat

- Bradenton, Manatee County, Palmetto, Lakewood Ranch, Real Estate, Market Report, MLS Information, Listings, HomesDokumen20 halamanBradenton, Manatee County, Palmetto, Lakewood Ranch, Real Estate, Market Report, MLS Information, Listings, HomesTHESERENAGROUPBelum ada peringkat

- HERITAGE HARBOUR, BRADENTON, Tennis and Golf Course MembershipsDokumen2 halamanHERITAGE HARBOUR, BRADENTON, Tennis and Golf Course MembershipsTHESERENAGROUPBelum ada peringkat

- Bradenton, Manatee County, Parade of Homes, Tour MapDokumen1 halamanBradenton, Manatee County, Parade of Homes, Tour MapTHESERENAGROUPBelum ada peringkat

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (890)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (587)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (72)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2219)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (119)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Jonsay Vs Solid Bank Corp.Dokumen15 halamanJonsay Vs Solid Bank Corp.MarizPatanaoBelum ada peringkat

- Ust Civil Q and A 2013 To 2015Dokumen55 halamanUst Civil Q and A 2013 To 2015twenty19 lawBelum ada peringkat

- Mondragon V CaDokumen5 halamanMondragon V CaLiv PerezBelum ada peringkat

- Cases Rule 2 DigestDokumen7 halamanCases Rule 2 DigestJessa PuerinBelum ada peringkat

- Revised Guidelines Implementing The Pag-IBIG Fund HRRL ProgramDokumen11 halamanRevised Guidelines Implementing The Pag-IBIG Fund HRRL ProgramRaine Buenaventura-EleazarBelum ada peringkat

- Credit Trans ReviewerDokumen34 halamanCredit Trans ReviewerMhayBinuyaJuanzon100% (3)

- Avila - GG Sportwear Vs Bdo - 1Dokumen3 halamanAvila - GG Sportwear Vs Bdo - 1Sum Aaron AvilaBelum ada peringkat

- GR 177050Dokumen4 halamanGR 177050Abegail Protacio Guardian100% (1)

- SC upholds CA decision nullifying writ of preliminary injunction in foreclosure caseDokumen3 halamanSC upholds CA decision nullifying writ of preliminary injunction in foreclosure caseJesa BayonetaBelum ada peringkat

- Court of Appeals Decision Reversed on Obligations Secured by Real Estate MortgageDokumen11 halamanCourt of Appeals Decision Reversed on Obligations Secured by Real Estate MortgageStrugglingStudentBelum ada peringkat

- G.R. No. L-2412 April 11, 1906 Pedro Roman vs. Andres GrimaltDokumen5 halamanG.R. No. L-2412 April 11, 1906 Pedro Roman vs. Andres GrimaltDiane UyBelum ada peringkat

- Special Commercial Law MidtermsDokumen3 halamanSpecial Commercial Law MidtermsCoreine Valledor-SarragaBelum ada peringkat

- Action of Breach and Extinguishment of SaleDokumen30 halamanAction of Breach and Extinguishment of SaleJanetGraceDalisayFabrero100% (3)

- Connie Campbell Against Steven Baum, MERSCORP, Inc, Et Al., Case #10CV3800Dokumen53 halamanConnie Campbell Against Steven Baum, MERSCORP, Inc, Et Al., Case #10CV3800Foreclosure FraudBelum ada peringkat

- Order Granting Motion To Proceed On Appeal in Forma Pauperis 09A11175-3Dokumen2 halamanOrder Granting Motion To Proceed On Appeal in Forma Pauperis 09A11175-3Janet and James100% (1)

- IDFCDokumen2 halamanIDFCRohit Sisodiya100% (1)

- Orola vs. Rural Bank of PontevedraDokumen13 halamanOrola vs. Rural Bank of PontevedraoscarletharaBelum ada peringkat

- DBP v. NLRC, 186 SCRA 841 (1990)Dokumen5 halamanDBP v. NLRC, 186 SCRA 841 (1990)carlota ann lafuenteBelum ada peringkat

- 1-13-3555 Foreclosure Service of Process UpheldDokumen7 halaman1-13-3555 Foreclosure Service of Process Upheldsbhasin1100% (1)

- Actions in PersonamDokumen9 halamanActions in PersonamJohn Ludwig Bardoquillo PormentoBelum ada peringkat

- 2019 Rem Law Bar ExamDokumen10 halaman2019 Rem Law Bar ExamSalvador II100% (1)

- BP 22 Law GuideDokumen42 halamanBP 22 Law GuidefocusedkheyBelum ada peringkat

- Credit Trans Mutuum To Warehouse Receipts CasesDokumen17 halamanCredit Trans Mutuum To Warehouse Receipts CasesDarlene GanubBelum ada peringkat

- SMART V Dava0, CIR vs. CA, CIR v. UCBPDokumen6 halamanSMART V Dava0, CIR vs. CA, CIR v. UCBPKath LeenBelum ada peringkat

- School of Law Property and Land Title Compilation of Questions and AnswersDokumen114 halamanSchool of Law Property and Land Title Compilation of Questions and AnswersTabs Net100% (3)

- Case Digests of Rule 59 Receivership (2018) CasesDokumen9 halamanCase Digests of Rule 59 Receivership (2018) CaseschaynagirlBelum ada peringkat

- Yam V CADokumen9 halamanYam V CAslashBelum ada peringkat

- Court Voids Mortgage of Estate Property Without Proper ApprovalDokumen26 halamanCourt Voids Mortgage of Estate Property Without Proper ApprovalAttyGalva22Belum ada peringkat

- The Invisible Crisis: Water Unaffordability in The United StatesDokumen64 halamanThe Invisible Crisis: Water Unaffordability in The United StatesRich SamartinoBelum ada peringkat

- Leung Yee V. F.L Strong Machinery Co. and WilliamsonDokumen19 halamanLeung Yee V. F.L Strong Machinery Co. and WilliamsonYasser MambuayBelum ada peringkat