Anda mungkin juga menyukai

- An Overview of Organizational Commitment Among The IT Employees in Chennai CityDokumen3 halamanAn Overview of Organizational Commitment Among The IT Employees in Chennai CityBONFRINGBelum ada peringkat

- Block Chain Technology For Privacy Protection For Cloudlet-Based Medical Data SharingDokumen4 halamanBlock Chain Technology For Privacy Protection For Cloudlet-Based Medical Data SharingBONFRINGBelum ada peringkat

- Review On MRI Brain Tumor Segmentation ApproachesDokumen5 halamanReview On MRI Brain Tumor Segmentation ApproachesBONFRINGBelum ada peringkat

- Smart Home Implementing IOT Technology With Multilingual Speech Recognition SystemDokumen6 halamanSmart Home Implementing IOT Technology With Multilingual Speech Recognition SystemBONFRINGBelum ada peringkat

- A Study On Time ManagementDokumen5 halamanA Study On Time ManagementBONFRINGBelum ada peringkat

- Review of Data Mining Classification TechniquesDokumen4 halamanReview of Data Mining Classification TechniquesBONFRINGBelum ada peringkat

- Detection of Polycystic Ovary Syndrome From Ultrasound Images Using SIFT DescriptorsDokumen5 halamanDetection of Polycystic Ovary Syndrome From Ultrasound Images Using SIFT DescriptorsBONFRINGBelum ada peringkat

- Effective Online Discussion Data For Teachers Reflective Thinking Using Feature Base ModelDokumen5 halamanEffective Online Discussion Data For Teachers Reflective Thinking Using Feature Base ModelBONFRINGBelum ada peringkat

- Android Application Development For Textile IndustryDokumen4 halamanAndroid Application Development For Textile IndustryBONFRINGBelum ada peringkat

- Different Traffic Profiles For Wireless NetworkDokumen3 halamanDifferent Traffic Profiles For Wireless NetworkBONFRING100% (1)

- Investigation of CO2 Capturing Capacity of Solid Adsorbents (PEIs) Polyethylenimines From Automotive Vehicle Exhausts System For 4-Stroke SI EngineDokumen5 halamanInvestigation of CO2 Capturing Capacity of Solid Adsorbents (PEIs) Polyethylenimines From Automotive Vehicle Exhausts System For 4-Stroke SI EngineBONFRINGBelum ada peringkat

- Preventing The Breach of Sniffers in TCP/IP Layer Using Nagles AlgorithmDokumen5 halamanPreventing The Breach of Sniffers in TCP/IP Layer Using Nagles AlgorithmBONFRINGBelum ada peringkat

- Security Enhancement and Time Delay Consumption For Cloud Computing Using AES and RC6 AlgorithmDokumen6 halamanSecurity Enhancement and Time Delay Consumption For Cloud Computing Using AES and RC6 AlgorithmBONFRINGBelum ada peringkat

- Automated Switching Solar Power Grid Tie Inverter Using Embedded SystemDokumen5 halamanAutomated Switching Solar Power Grid Tie Inverter Using Embedded SystemBONFRINGBelum ada peringkat

- Awareness Among The Consumers About Instant Food ProductsDokumen3 halamanAwareness Among The Consumers About Instant Food ProductsBONFRINGBelum ada peringkat

- Power Quality Improvement Using Dynamic Voltage RestorerDokumen4 halamanPower Quality Improvement Using Dynamic Voltage RestorerBONFRINGBelum ada peringkat

- Topic Categorization Based On User Behaviour in Random Social Networks Using Firefly AlgorithmDokumen5 halamanTopic Categorization Based On User Behaviour in Random Social Networks Using Firefly AlgorithmBONFRINGBelum ada peringkat

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- Banking AwarenessDokumen412 halamanBanking AwarenessSai PraveenBelum ada peringkat

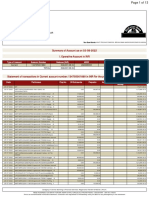

- Summary of Account As On 03-08-2022 I. Operative Account in INRDokumen13 halamanSummary of Account As On 03-08-2022 I. Operative Account in INRMonu DewanganBelum ada peringkat

- Statement of Affairs of The State Bank of Pakistan Banking Department As On The 27 April, 2018Dokumen1 halamanStatement of Affairs of The State Bank of Pakistan Banking Department As On The 27 April, 2018muhammad nazirBelum ada peringkat

- Mastercard Switch RulesDokumen80 halamanMastercard Switch RulesBaluBelum ada peringkat

- Latihan Soal Rekonsiliasi BankDokumen1 halamanLatihan Soal Rekonsiliasi BankIchsan WibowoBelum ada peringkat

- Study Plan JAIIBDokumen17 halamanStudy Plan JAIIBbagavan10Belum ada peringkat

- Functions - Duties of The RBI GovernorDokumen4 halamanFunctions - Duties of The RBI GovernorDeepanwita SarBelum ada peringkat

- Afghanistan Banking LawDokumen104 halamanAfghanistan Banking Lawyargulkhan54Belum ada peringkat

- PayGate PayWebv2 v1.15Dokumen23 halamanPayGate PayWebv2 v1.15gmk0% (1)

- CIMA Chartered Management Accounting Qualification 2010Dokumen7 halamanCIMA Chartered Management Accounting Qualification 2010lunoguBelum ada peringkat

- Maths ProjectDokumen15 halamanMaths Projecttmbcreditdummy50% (2)

- Taxation of Financial Services Sybbi FinalDokumen24 halamanTaxation of Financial Services Sybbi Finalsheenu152005Belum ada peringkat

- Akash RukhaiyarDokumen2 halamanAkash Rukhaiyaradvindulali100% (2)

- Deloitte Treasury BusinessDokumen4 halamanDeloitte Treasury BusinessyalkalBelum ada peringkat

- Project Report of Hotel Gawaran For Bank LoanDokumen11 halamanProject Report of Hotel Gawaran For Bank Loansachin919575% (4)

- PDFDokumen374 halamanPDFSimbuBelum ada peringkat

- Earnings Insight FactSet 01-2019Dokumen29 halamanEarnings Insight FactSet 01-2019krg09Belum ada peringkat

- 06 Puget Sound State Bank v. Washington Paving Co.Dokumen8 halaman06 Puget Sound State Bank v. Washington Paving Co.KathBelum ada peringkat

- Organisational Behavior On SBM BANKDokumen101 halamanOrganisational Behavior On SBM BANKkeshav_26Belum ada peringkat

- Mode of OperationsDokumen5 halamanMode of OperationsArchana SinhaBelum ada peringkat

- Swarna Vriksha One PagerDokumen5 halamanSwarna Vriksha One PagerArun Singh0% (1)

- Uniform Loan Delivery Data - Set FaqsDokumen4 halamanUniform Loan Delivery Data - Set FaqsraghuBelum ada peringkat

- Banking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduDokumen27 halamanBanking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduilusonaBelum ada peringkat

- Pag Ibig Foreclosed Properties Pubbid 2017 05 25 NCR No Discount PDFDokumen25 halamanPag Ibig Foreclosed Properties Pubbid 2017 05 25 NCR No Discount PDFrochie cerveraBelum ada peringkat

- Statement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Dokumen3 halamanStatement On Impact of Audit Qualifications For The Period Ended March 31, 2016 (Company Update)Shyam SunderBelum ada peringkat

- Accpac - Guide - Checklist For Bank Setup PDFDokumen4 halamanAccpac - Guide - Checklist For Bank Setup PDFcaplusincBelum ada peringkat

- Vendor Registration Form - VRF 3 0Dokumen1 halamanVendor Registration Form - VRF 3 0Suraj Sankar Mukherjee100% (1)

- Cash For SeatworkDokumen3 halamanCash For SeatworkMika MolinaBelum ada peringkat

- 01 - DBS Annual Report 2016-FullDokumen208 halaman01 - DBS Annual Report 2016-Fullvolcan9000Belum ada peringkat

- Corporate Governance-Cadbury ReportDokumen13 halamanCorporate Governance-Cadbury ReportParamjit Sharma100% (7)