Anda mungkin juga menyukai

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDari EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryPenilaian: 3.5 dari 5 bintang3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Dari EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Penilaian: 4.5 dari 5 bintang4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDari EverandGrit: The Power of Passion and PerseverancePenilaian: 4 dari 5 bintang4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDari EverandNever Split the Difference: Negotiating As If Your Life Depended On ItPenilaian: 4.5 dari 5 bintang4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDari EverandThe Little Book of Hygge: Danish Secrets to Happy LivingPenilaian: 3.5 dari 5 bintang3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDari EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaPenilaian: 4.5 dari 5 bintang4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDari EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifePenilaian: 4 dari 5 bintang4/5 (5795)

- Rise of ISIS: A Threat We Can't IgnoreDari EverandRise of ISIS: A Threat We Can't IgnorePenilaian: 3.5 dari 5 bintang3.5/5 (137)

- Her Body and Other Parties: StoriesDari EverandHer Body and Other Parties: StoriesPenilaian: 4 dari 5 bintang4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDari EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You ArePenilaian: 4 dari 5 bintang4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDari EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyPenilaian: 3.5 dari 5 bintang3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDari EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersPenilaian: 4.5 dari 5 bintang4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDari EverandShoe Dog: A Memoir by the Creator of NikePenilaian: 4.5 dari 5 bintang4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDari EverandThe Emperor of All Maladies: A Biography of CancerPenilaian: 4.5 dari 5 bintang4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDari EverandTeam of Rivals: The Political Genius of Abraham LincolnPenilaian: 4.5 dari 5 bintang4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDari EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RacePenilaian: 4 dari 5 bintang4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDari EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FuturePenilaian: 4.5 dari 5 bintang4.5/5 (474)

- Exhibit D Tenant Rental Ledger Tenant Rental Ledger CardDokumen1 halamanExhibit D Tenant Rental Ledger Tenant Rental Ledger CardStephanie KaitlynBelum ada peringkat

- On Fire: The (Burning) Case for a Green New DealDari EverandOn Fire: The (Burning) Case for a Green New DealPenilaian: 4 dari 5 bintang4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Dari EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Penilaian: 4 dari 5 bintang4/5 (98)

- The Unwinding: An Inner History of the New AmericaDari EverandThe Unwinding: An Inner History of the New AmericaPenilaian: 4 dari 5 bintang4/5 (45)

- Asian Countries Capitals and CurrenciesDokumen1 halamanAsian Countries Capitals and CurrenciesQuality Lover50% (2)

- MD Wasim Bhuyian: Statement of Account Savings Bank DepositsDokumen2 halamanMD Wasim Bhuyian: Statement of Account Savings Bank DepositsSalahuddin Nayan71% (7)

- Account Number: 552592902 PIN CODE: 213996: Tax InvoiceDokumen2 halamanAccount Number: 552592902 PIN CODE: 213996: Tax InvoiceFikile EemBelum ada peringkat

- Axis Bank Statement 916020016900949 PDFDokumen6 halamanAxis Bank Statement 916020016900949 PDFAnonymous iN6XHHABelum ada peringkat

- Cash and Cash Equivalents PDFDokumen4 halamanCash and Cash Equivalents PDFJade Gomez100% (1)

- Account Statement PDFDokumen12 halamanAccount Statement PDFShalini SinghBelum ada peringkat

- Client Information Sheet: Company'S Information::: Signatory'S InformationDokumen4 halamanClient Information Sheet: Company'S Information::: Signatory'S InformationGarbo BentleyBelum ada peringkat

- Stcpay WU 23031477 PDFDokumen1 halamanStcpay WU 23031477 PDFNeon True BeldiaBelum ada peringkat

- Table of ContentDokumen10 halamanTable of ContentHarsh MehtaBelum ada peringkat

- Circular No. 45 / 2007-08 Credit Guarantee Scheme (CGS) - Modification in Guarantee Fee (GF) and Annual Service Fee (ASF) StructureDokumen1 halamanCircular No. 45 / 2007-08 Credit Guarantee Scheme (CGS) - Modification in Guarantee Fee (GF) and Annual Service Fee (ASF) StructureHarsh MehtaBelum ada peringkat

- Circular No. 43 / 2007-08: All Member Lending Institutions of CGTSIDokumen1 halamanCircular No. 43 / 2007-08: All Member Lending Institutions of CGTSIHarsh MehtaBelum ada peringkat

- Circ 36Dokumen8 halamanCirc 36Harsh MehtaBelum ada peringkat

- New RefDokumen3 halamanNew RefHarsh MehtaBelum ada peringkat

- Circular No. 44 / 2007-08: All Member Lending Institutions of CGTMSEDokumen1 halamanCircular No. 44 / 2007-08: All Member Lending Institutions of CGTMSEHarsh MehtaBelum ada peringkat

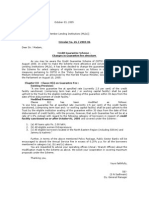

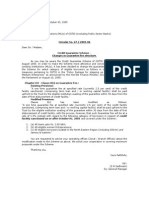

- Credit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government of India and SIDBI) SDokumen2 halamanCredit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government of India and SIDBI) SHarsh MehtaBelum ada peringkat

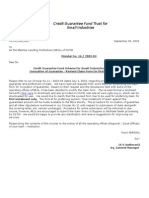

- Credit Guarantee Fund Trust For Small IndustriesDokumen3 halamanCredit Guarantee Fund Trust For Small IndustriesHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No. 34 / 2006-07Dokumen1 halamanCredit Guarantee Fund Trust For Small Industries: Circular No. 34 / 2006-07Harsh MehtaBelum ada peringkat

- Circ 36Dokumen8 halamanCirc 36Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: All Member Lending InstitutionsDokumen4 halamanCredit Guarantee Fund Trust For Small Industries: All Member Lending InstitutionsHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government of India and SIDBI) SDokumen2 halamanCredit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government of India and SIDBI) SHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government. of India and SIDBI)Dokumen2 halamanCredit Guarantee Fund Trust For Micro and Small Enterprises: (Set Up by Government. of India and SIDBI)Harsh MehtaBelum ada peringkat

- Circ 31Dokumen2 halamanCirc 31Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: All Member Lending Institutions of CGTSIDokumen2 halamanCredit Guarantee Fund Trust For Small Industries: All Member Lending Institutions of CGTSIHarsh MehtaBelum ada peringkat

- Circ 26Dokumen2 halamanCirc 26Harsh MehtaBelum ada peringkat

- Circ 28Dokumen1 halamanCirc 28Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: CGTSI/ (44) / 681 September 01, 2006Dokumen1 halamanCredit Guarantee Fund Trust For Small Industries: CGTSI/ (44) / 681 September 01, 2006Harsh MehtaBelum ada peringkat

- Circular No. 30 / 2005-06Dokumen1 halamanCircular No. 30 / 2005-06Harsh MehtaBelum ada peringkat

- Circ 25Dokumen1 halamanCirc 25Harsh MehtaBelum ada peringkat

- Circ 27Dokumen1 halamanCirc 27Harsh MehtaBelum ada peringkat

- Circ 29Dokumen3 halamanCirc 29Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No.14/2003-04Dokumen1 halamanCredit Guarantee Fund Trust For Small Industries: Circular No.14/2003-04Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No. 19/2003-04Dokumen2 halamanCredit Guarantee Fund Trust For Small Industries: Circular No. 19/2003-04Harsh MehtaBelum ada peringkat

- Intimate The Trust Before Entering Into Any Compromise or ArrangementDokumen2 halamanIntimate The Trust Before Entering Into Any Compromise or ArrangementHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No. 18/2003-04Dokumen2 halamanCredit Guarantee Fund Trust For Small Industries: Circular No. 18/2003-04Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Scheme For Small Industries (CGFSI)Dokumen2 halamanCredit Guarantee Fund Scheme For Small Industries (CGFSI)Harsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Click HereDokumen1 halamanCredit Guarantee Fund Trust For Small Industries: Click HereHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No. 17/2003-04 Communication Is The KeyDokumen2 halamanCredit Guarantee Fund Trust For Small Industries: Circular No. 17/2003-04 Communication Is The KeyHarsh MehtaBelum ada peringkat

- Credit Guarantee Fund Trust For Small Industries: Circular No. 12/2003-04Dokumen1 halamanCredit Guarantee Fund Trust For Small Industries: Circular No. 12/2003-04Harsh MehtaBelum ada peringkat

- Discount, Denoted by D Which Is A Measure of Interest Where The Interest IsDokumen3 halamanDiscount, Denoted by D Which Is A Measure of Interest Where The Interest IsNguyễn Quang TrườngBelum ada peringkat

- HT - LTIP E-BillDokumen4 halamanHT - LTIP E-BillRatnakar GuravBelum ada peringkat

- Capital Adequacy Ratio - Wikipedia, The Free EncyclopediaDokumen4 halamanCapital Adequacy Ratio - Wikipedia, The Free EncyclopediaTrần Kim ChungBelum ada peringkat

- 307 NotesDokumen6 halaman307 NotesNeel ManushBelum ada peringkat

- ICICI Bank ACQUISITION WITH BANK OF RAJASTHANDokumen6 halamanICICI Bank ACQUISITION WITH BANK OF RAJASTHANPrayagraj PradhanBelum ada peringkat

- Case Study One CapitecDokumen10 halamanCase Study One Capitecstanely ndlovuBelum ada peringkat

- MagnetarDokumen11 halamanMagnetarYokohama3000Belum ada peringkat

- PPT Presentation RbiDokumen10 halamanPPT Presentation RbiAayushBelum ada peringkat

- NBP RateSheet 28 06 2019Dokumen1 halamanNBP RateSheet 28 06 2019Tahseen AhmedBelum ada peringkat

- 2010fin MS263Dokumen5 halaman2010fin MS263nmsusarla999Belum ada peringkat

- Banci Din RomaniaDokumen1 halamanBanci Din Romaniaflorin74Belum ada peringkat

- BOM and Yes Bank..Dokumen23 halamanBOM and Yes Bank..kunalclad41Belum ada peringkat

- 1298 IDokumen1 halaman1298 ICormac O'KeeffeBelum ada peringkat

- Radian Default Claims Servicing GuideDokumen42 halamanRadian Default Claims Servicing GuidelostvikingBelum ada peringkat

- DetailedStatement PDFDokumen2 halamanDetailedStatement PDFAditi MistryBelum ada peringkat

- Yes Bank-Case Study AnalysisDokumen9 halamanYes Bank-Case Study AnalysisANUSHKA SHARMA 20111307Belum ada peringkat

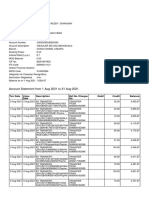

- Account Statement From 1 Aug 2021 To 31 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDokumen6 halamanAccount Statement From 1 Aug 2021 To 31 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChirasani Yogeshwar ReddyBelum ada peringkat

- Hayman July 07Dokumen5 halamanHayman July 07grumpyfeckerBelum ada peringkat

- BNI Mobile Banking: Histori TransaksiDokumen7 halamanBNI Mobile Banking: Histori TransaksiIrvan KurniawanBelum ada peringkat

- Multi Currency in PeoplesoftDokumen8 halamanMulti Currency in PeoplesoftdannydongappaBelum ada peringkat

- MHP TSYS Footer FAQs - 2023 - FINAL - UpdatedDokumen3 halamanMHP TSYS Footer FAQs - 2023 - FINAL - UpdatedAlex BurksBelum ada peringkat